이상탐지 실습

캐글의 신용카드 거래 데이터를 가지고 실습을 진행해 보자

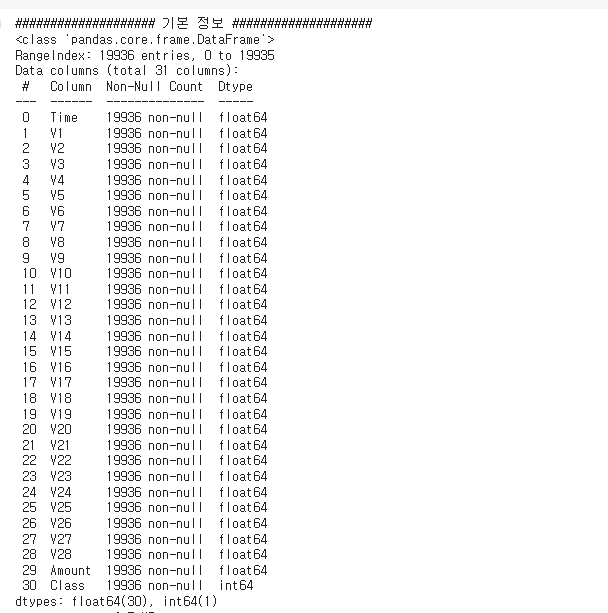

데이터 셋 설명

Credit Card Fraud Detection 데이터

- 신용카드 거래에서의 사기 탐지를 위해 설계된 데이터셋

• 2013년 유럽 카드 소지자들의 거래 데이터를 포함

• 총 284,807건의 거래 데이터가 있고

• 그 중 492건(0.172%)의 사기 거래 데이터가 있음그런데!! 데이터가 너무 커서 샘플링을 함. - 전체 19,936건, 사기 34건 (0.171%) 데이터를 포함 - 변수로는 Time, Amount, V1~V28, Class

• Time : 첫 거래 후 각 거래 사이 경과 시간 (초)

• Amount : 거래 금액

• V1~V28 : PCA로 얻은 수치형 입력 변수

• Class : 정상 거래 (0)와 비정상 거래 (1)

문제정의

풀어야 하는 문제

• 주어진 거래 관련 데이터를 바탕으로 이상 거래 데이터를 탐지

- 머신 러닝 모델의 입, 출력 정의

- 입력 : 거래 관련 데이터

- Time

- Amount

- V1 ~ V28

- 출력 : 각 데이터 포인트 마다 할당된 이상치 점수 (종속 변수)

- 후처리 필요

- 입력 : 거래 관련 데이터

1. EDA

- 데이터는 독립변수 Time,V1~V28, Amount와 종속변수 Class가 있다.

- 총 31개의 데이터로 결측치는 없는 모습!

- 기초 통계량은 패스!

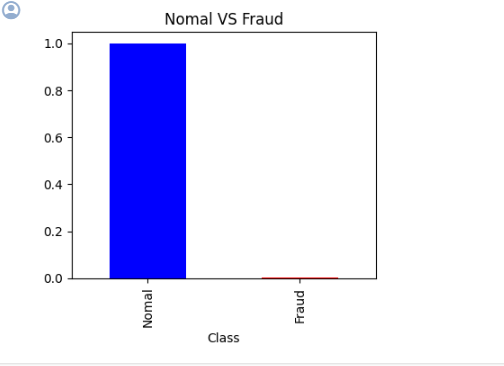

범주형 데이터 (Class 컬럼) 분석

# 이상치 여부 시각화 (Class : 종속변수)

y_columns = ['Class']

y = credit[y_columns]

import matplotlib.pyplot as plt

plt.figure(figsize=(4, 4))

y.value_counts(normalize=True).plot(kind='bar', color=['b', 'r'])

plt.xticks(range(2), ['Nomal', 'Fraud'])

plt.title('Nomal VS Fraud')

plt.tight_layout()

plt.show()

값이 Fraud가 너무 적다! 실제 갯수를 확인해 보자.

# 갯수 확인

num_Normal = (y==0).sum().values[0]

num_Fraud = (y==1).sum().values[0]

print(f'Number of Normal data : {num_Normal}')

print(f'Number of Fraud data : {num_Fraud}')출력값:

Number of Normal data : 19902

Number of Fraud data : 34

확실히 작다. 이는 이상치로 분류할 수 있을 듯.

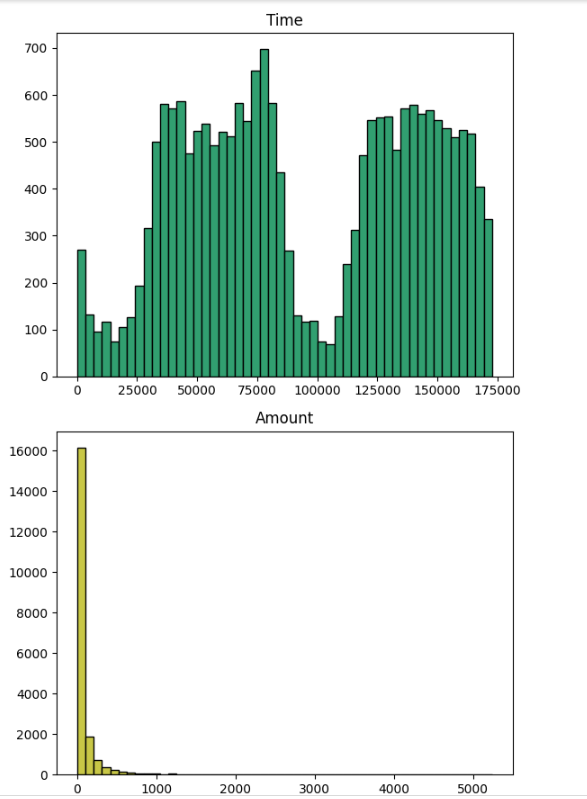

수치형 데이터 (시간, 거래 금액) 분석

# Time과 Amount 데이터

time_amount_columns = ['Time', 'Amount']

time_amount = credit[time_amount_columns]

# 분포 시각화

plt.figure(figsize=(6, 9))

np.random.seed(seed)

for idx, numeric in enumerate(time_amount_columns) :

col = (np.random.random(), np.random.random(), np.random.random())

plt.subplot(2, 1, idx+1)

plt.hist(time_amount[numeric], bins=50, color=col, edgecolor='black')

plt.title(numeric)

plt.tight_layout()

plt.tight_layout()

plt.show()

TIME!

Time의 경우 거래 시작 이후의 경과 시간을 나타내므로

기준 시간 정보가 있다면 주기성을 갖고 있을 수 있음

- 낮에 한 거래와 밤에 한 거래와 같이

- 그렇다면 주기 함수를 적용하는 것도 좋은 방법!

하지만 시간 그래프를 보면 175,000초(대략 2일) 정도까지 가지고 있다.

시작 지점이 정해져있지 않기 때문에 함수를 사용하는 것은 어렵다.

큰 outlier가 없어 보이므로 Min-Max Scaling 을 사용해서 시간대를 줄요보자.

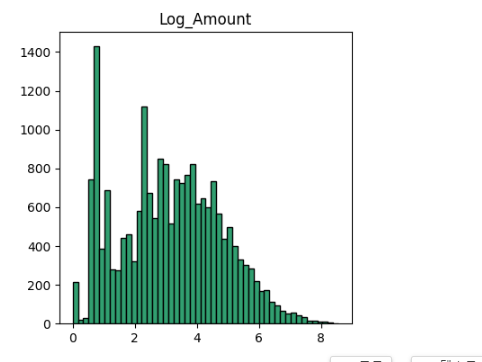

AMOUNT!

Amount는 치우침이 있지만,

신용 카드 거래 금액으로 의미가 없는 데이터는 아님

근데 큰 값은 너무 작아서 그래프에서 보이지 않는다.

이처럼 극단적으로 치우쳐진 값을 처리하기 위해 Log 스케일링을 진행!

credit['Log_Amount'] = np.log(credit['Amount']+1)

이를 시각화 하면!

그럼 이렇게 예쁜 그래프가 나온다!

Log(0) 의 값을 피하기 위해 +1 값을 추가 해준다.

• Amount의 경우 1 정도의 크기가 큰 문제가 되지 않음

• 이 값이 영향을 미치는 데이터인지 확인 필요

2. 데이터 전처리 진행

- Time : Min-Max Scailing

- Amount : Log Amount 사용

- V1 ~ V28 : 그대로 사용

Time 데이터 MinMaxScaler 처리

# Time 변수를 Min Max Scaling

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler()

credit_time = scaler.fit_transform(credit[['Time']])

credit_time = pd.DataFrame(credit_time)

credit_time.columns = ['Time']

credit_time

Amount 변수를 Log scale로 진행

# Amount 변수를 Log scale로

credit_log_amount= credit[log_amount_columns]

credit_log_amount

이를 데이터 프레임으로 합친다!

credit_combined = pd.concat([credit_time,

credit_log_amount,

Vs_data],

axis=1)

credit_combined3. 모델 구축!

학습진행

n_estimators = 100

max_samples = 'auto'

# contamination = 'auto'

contamination = num_Fraud/(num_Normal+num_Fraud)

# Isolation Forest 생성 및 학습

from sklearn.ensemble import IsolationForest

IForest = IsolationForest(n_estimators=n_estimators,

max_samples=max_samples,

contamination=contamination,

random_state=seed)

IForest.fit(credit_combined)contamination = num_Fraud/(num_Normal+num_Fraud) : 우리는 사기 갯수를 알기 때문에 임계치 비율을 완벽하게 기입함.

평가 진행

y_true = credit['Class']

y_pred = IForest.predict(credit_combined)

y_pred = np.where(y_pred == 1, 0, 1)# 성능 평가

from sklearn.metrics import accuracy_score, precision_score, recall_score, f1_score

accuracy = accuracy_score(y_true, y_pred)

precision = precision_score(y_true, y_pred)

recall = recall_score(y_true, y_pred)

f1 = f1_score(y_true, y_pred)

print(f'정확도 Accuracy : {accuracy*100:.2f} %')

print(f'정밀도 Precision : {precision*100:.2f} %')

print(f'재현율 Recall : {recall*100:.2f} %')

print(f'F1 : {f1*100:.2f} %')출력값:

정확도 Accuracy : 99.77 %

정밀도 Precision : 32.35 %

재현율 Recall : 32.35 %

F1 : 32.35 %

정확도 말고는 다 낮게 나왔다!!! 왜지!!

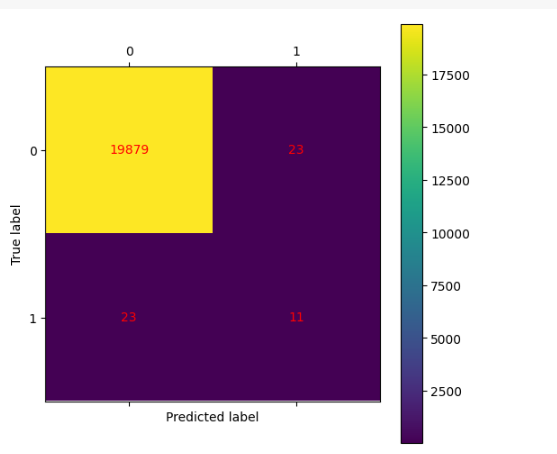

이를 confusion_matrix를 그려보면 알 수 있다.

from sklearn.metrics import confusion_matrix

result_cm = confusion_matrix(y_true, y_pred)

plt.figure(figsize=(6, 6))

plt.matshow(result_cm, fignum=1)

plt.xticks(range(2), [0, 1])

plt.yticks(range(2), [0, 1])

plt.ylabel('True label')

plt.xlabel('Predicted label')

plt.colorbar()

for (i, j), val in np.ndenumerate(result_cm):

plt.text(j, i, f'{val}', ha='center', va='center', color='red')

plt.show()

0,0의 부분은 정상 데이터를 예측한 갯 수,

1,1,은 이상치 데이터를 예측한 갯 수 이다.

이때 이상치 데이터의 수가 너무 낮아서 이런 결과가 나온것이다.

이럴때는 전문가의 도움을 받는다!