참고)https://efinancemanagement.com/financial-accounting/fundamental-accounting-equation

예시 : Dixon

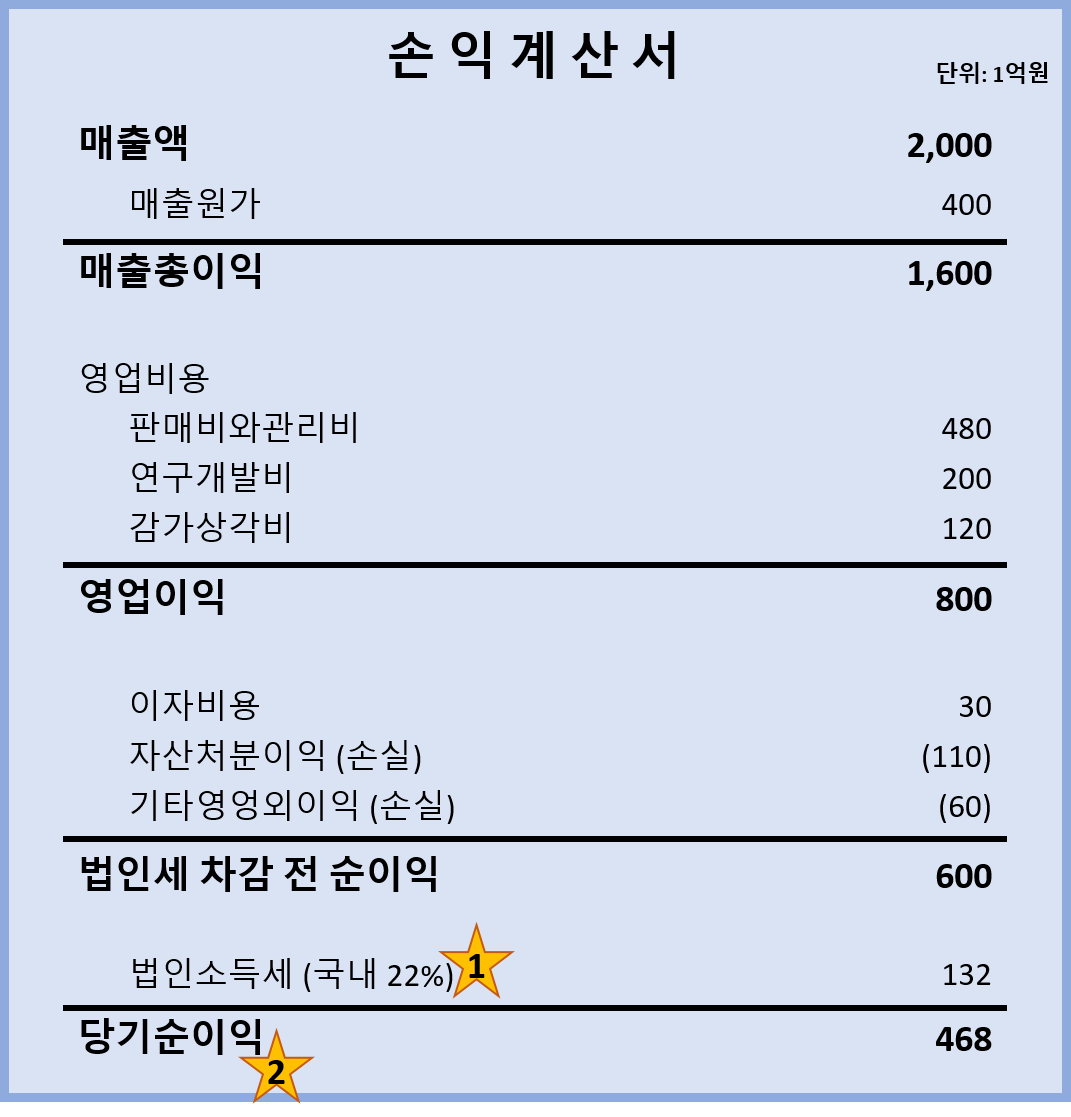

Mr Dixon runs a shop selling ironmongery in rented premises. He has some accounting experience and has extracted the following trial balance from his nominal ledger as at 31 December 2022.

The following is Trial balance as at 31 December 2022

The following information is also relevant:

(a) Depreciation has not yet been charged. The following rates are to be used:

Shop fittings: 5% on cost

Leasehold: straight line over estimated useful life of 20 years, with no residual value.

(b) A debt of ₩500 is irrecoverable and is to be written off; the doubtful debts provision is to be increased to 2% of recoverable debtors

(c) The proprietor has withdrawn goods costing ₩1,000 for his personal use, which have not been recorded as drawings.

(d) The inventory at 31 December 2022 is to be valued at its cost of ₩30,000.

밑의 주석은 BS, IS를 실제로 적으면서 적용해보도록 하겠다.

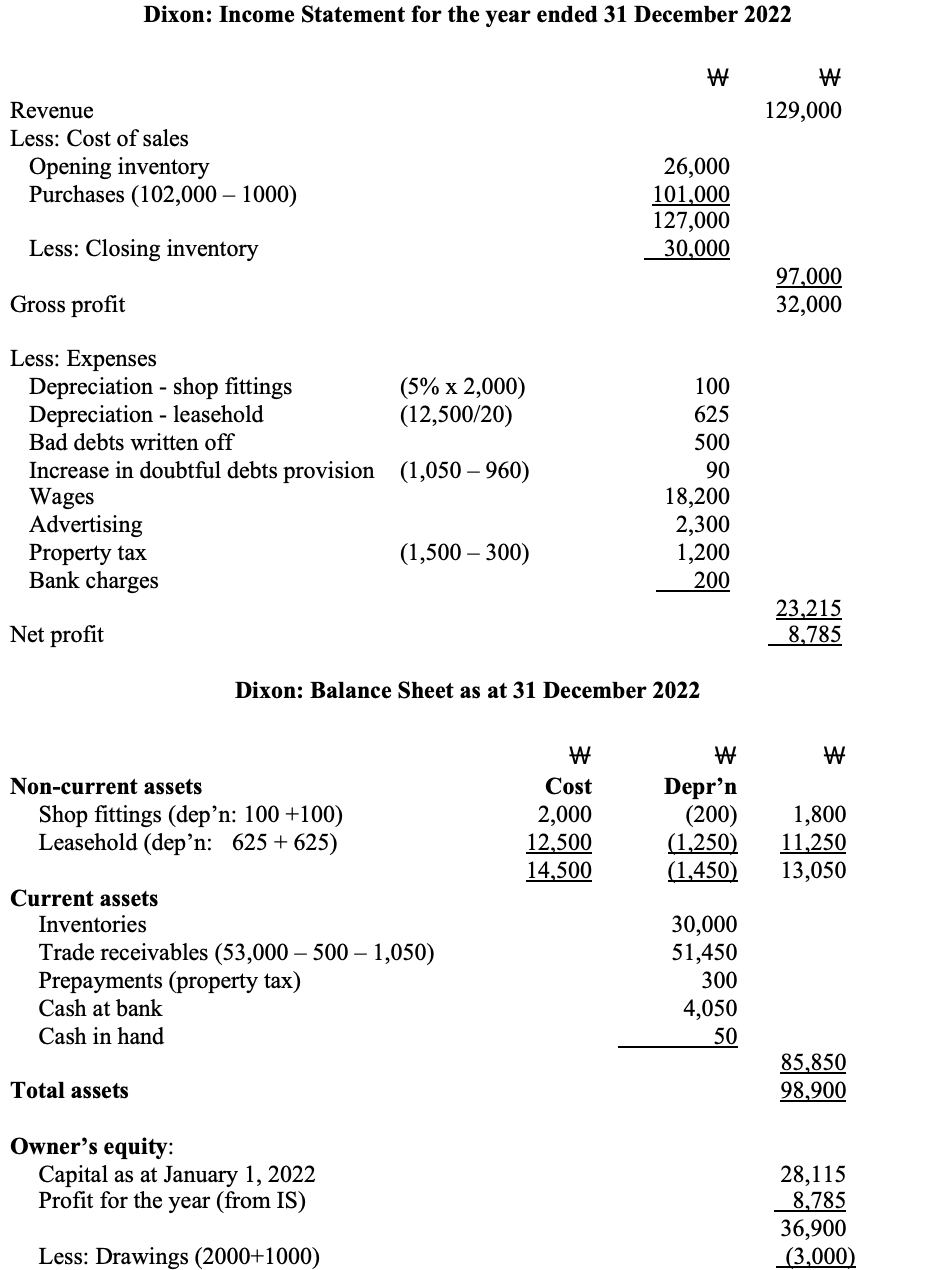

Income Statement

그 전에 Income Statement는 무엇을 표현하는지, Balance Sheet과는 어떤 차이점이 있는지 알아보겠다.

Balance Sheet는 어떤 특정 기간에 회사가 가지고 있는 Asset을 중심으로 Liability, Equity를 분석한 재무재표 이다.

반면 Income Statement 는 회사의 경영활동으로 발생하는 손해와 이익을 중심으로 회사를 분석한 재무재표이다.

Asset은 기업이 사용할 수 있는 자원으로 볼 수 있다. 빛이든, 회사가 가진 현금이든 사용할 수 있는 것을 중심으로 분석한다. 손익은 Asset과는 어떤 차이가 있는지는, 밑의 Income Statement의 더 자세한 정의를 보면서 알아보자.

포괄손익계산서는 그 회계기간에 속하는 모든 수익(Revenue)과 이에 대응하는 모든 비용(Expense)을 적정하게 표시하여 손익(Profit, Loss)을 나타내는 회계문서를 말한다.

Revenue

Revenue is the total amount of income generated by the sale of goods or services related to the company's primary operations.

다른 말로 the top line 이라고도 한다. 왜냐하면, Income Statement에 제일 위에 위치하기 때문이다.

Expense

An expense is the reduction in value of an asset as it is used to generate revenue.

간단한 형식으로는 Revenue - Expense = Profit(Loss)가 될 것이다.

Expense는 여러 부분으로 나눌 수 있다.

Expense중에서 Cost of sales(매출원가),

The cost of goods sold is usually the largest expense that a business incurs. This line item is the aggregate amount of expenses incurred to create products or services that have been sold.

는 대게 Expense에서 매우 큰 비용을 차지하기 때문에, 따로 표시한다. 또한, Revenue - Cost of sales 를 미리 해서 Gross Profit(매출 총이익) 라는 개념을 만들기도 한다.

How much a firm earned by buying (or making) and selling merchandise

Expense 중에서 Operating Expense(영업비용)이라는 부분도 있다.

Costs involved in operating a business, such as rent, utilities, and salaries

세부 분류를 해보자면 이렇다.

- Selling expenses

- marketing, distribution

- advertising

- salespeople’s salaries - General expenses

- administrative expenses

- office salaries

- depreciation

- insurance

- rent

이렇게 모든 Expense를 빼고 남은 Profit이 진짜 Profit, 즉 Net Profit(당기 순이익)이다.

IS 예시 적용

이 표를 참고해서 한번 가보자구

Revenue

당연히 Sales $12900이 바로 Revenue가 될 것이다.

표로 점검해보면, 오른쪽에 Credit으로, Increase of an revenue/income이므로 타당한 표이다.

Expense

Cost of sales

매출원가에 해당하는 부분들은 Purchases(새로 산 원재료)그리고 Stock/inventory in trade(이미 존재하는 원재료)이다.

표의 점검을 해보자면, 매출원가는 Expense이므로 Debit에 들어가는 것이 맞다.

관련된 주석을 살펴보자. C와 D 이다.

(c) The proprietor has withdrawn goods costing ₩1,000 for his personal use, which have not been recorded as drawings.

Drawings:Goods taken by the owner of a business for his own use

Goods의 1000원만큼의 Cost라고 했을 때에, 이는 정가인가 원가인가? 저번에도 보았듯이 정가로 판매될 수 있는 가능성은 따지는 것이 아니기 때문에 원가이다. 그러므로, 매출원가에서 1000원을 더해주거나 빼주는 접근이 옳다.

Expense의 정의를 다시 보자.

An expense is the reduction in value of an asset as it is used to generate revenue.

주인이 자신을 위해서 쓰는 것은, 수익을 위해서 쓰는 것 이라고 할 수 없다. 그러므로, 매출원가에서 1000원을 없애주는 것이 옳다.

새로 산 원재료 말고, 이미 있는 inventory의 변동은 opening, closing inventory로 정의된다.

Opening inventory:the total monetary value of items that are in stock and ready to use or sell at the start of an accounting period.

Closing inventory:the amount of stock that an organisation has at the end of an accounting period.

Tip을 주자면, opening은 항상 Trial balance, closing은 주석에 달아놓는다고 한다.

Trial balance에 있는 inventory는 날짜가 1 jan 2022이다. Opening inventory이다.

(d) The inventory at 31 December 2022 is to be valued at its cost of ₩30,000.

반면, 주석에 있는 inventory는 31 december 2022이다. Closing inventory이다.

그래서 결국 매출원가는 얼마인가?

Purchases + Opening inventory - drawings - Closing inventory

를 적용하면(Closing Inventory는 매출원가 입장에서 -) $97000 이다.

Gross Profit

그러면 Gross Profit 도 구할 수가 있다.

Revenue - Cost of sales = Gross Profit

이므로 129000 - 97000 = 32000 이다.

Operating Expenses

Depreciation

부동산으로 발생하는 Decipration이든, shop fitting으로 만든 인테리어든 Decipriation이든 모두 business를 경영하는데 드는 Expense 이다.

그러므로 Debit이 되는 것이 맞다.

구체적인 수치는 주석에 정보가 나와있다.

(a) Depreciation has not yet been charged. The following rates are to be used:

Shop fittings: 5% on cost

Leasehold: straight line over estimated useful life of 20 years, with no residual value.

Trial balance 에 나와있는 수치는 현재까지의 Decipriation 이다. 우리는 December 31에 맞게 주석을 참고해서 Decipriation을 구해줘야 한다.

Shop fitting은 쉽다. 1000의 5%이므로, 전과 똑같은 100.

Leasehold와 관련해서 straight line 이 무엇인지 질문할 수 있다.

이는 Decipriation 의 기법인 Straight line, 그리고 Reducing Balance 중 하나이다.

Straight line:Equal amount each year over life of asset

그러므로, 전년도와 같은 $625이 이번년도 decipriation이 될 것이다.

이번 년도의 decipriation은 Expense로 기록이 된다.

725원으로 말이다.

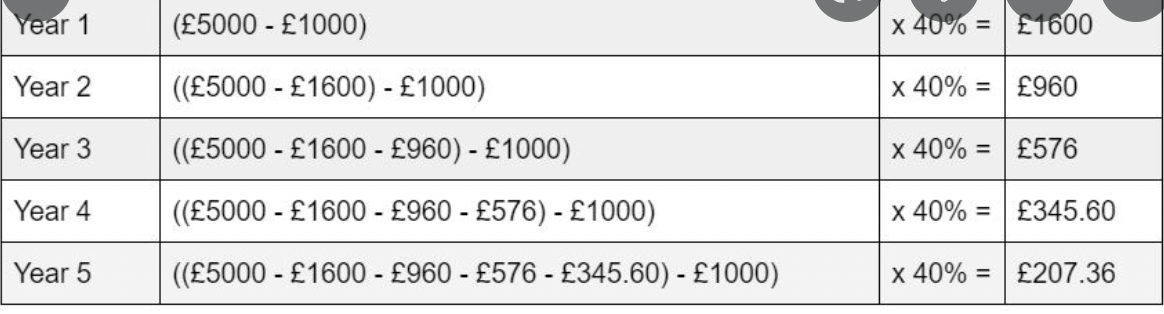

궁금하지 않겠지만 다른 기법인 Reducing Balance에 대해서도 알아보자.

Reducing balance: A % of net book value (NBV) at end of each year (NBV = cost less depreciation charged so far)

예시를 들어보자면 다음과 같을 것이다.

이는, 자산의 가치가 초반에 기하급수적으로 낮아지고, 시간이 조금 지나면 낮은 변화율로 감소하는 실제 특성을 반영하는 depreciation방식 이라고 한다.

Property Tax

시간에 역시 주목해야 한다.

보기에서는

Property tax for 15 months to 31 Mar 2023

이라고 쓰여 있는데, 현재 우리는 2022 12 31까지만 고려하면 된다.

나머지는 Accrual에 의해, 아직 발생하지 않은 부분이기 때문에 Expense로 고려되지 않는다. 이미 발생한 $1200만 Expense 로 포함된다.

Bad Debt

회사 경영과정에서 발생한 Expense로 역시 볼 수 있다.

주석 (b)에 따르면 $500 이라고 한다.

(b)의 나머지 부분을 살펴보면

the doubtful debts provision is to be increased to 2% of recoverable debtors

이런 말이 있다. 무슨 말일까?

Bad Debt는 실제로 먹튀한 거다. 반면 doubtful debt provision은 먹튀할 것이라고 예상되는 부분이다.

현재 이미 Provision for doubtful debt가 존재한다. 1 Jan 2022로 말이다!! $960

현재 기준은 31 December로, 주석에서는 2%로 증가한다고 한다.

현재 기준에서는 53000 * 2%, 즉 1050로 Provision이 증가했다.

결론적으로 $90의 Expense가 증가하였다.

Wages

당연히 영업비용으로, Expense이므로 Debit에 있는 것이 옳다.

$18200

Advertising

역시 영업비용, Debit에 있다.

$2300

Bank charges

또한 영업비용.

$200

Bank Charges(은행 수수료)

응 영업비용.

$200

다 더하면?

$23215 나옴.

Net Profit

Gross profit - Net Profit = 8785

나이쓰!!

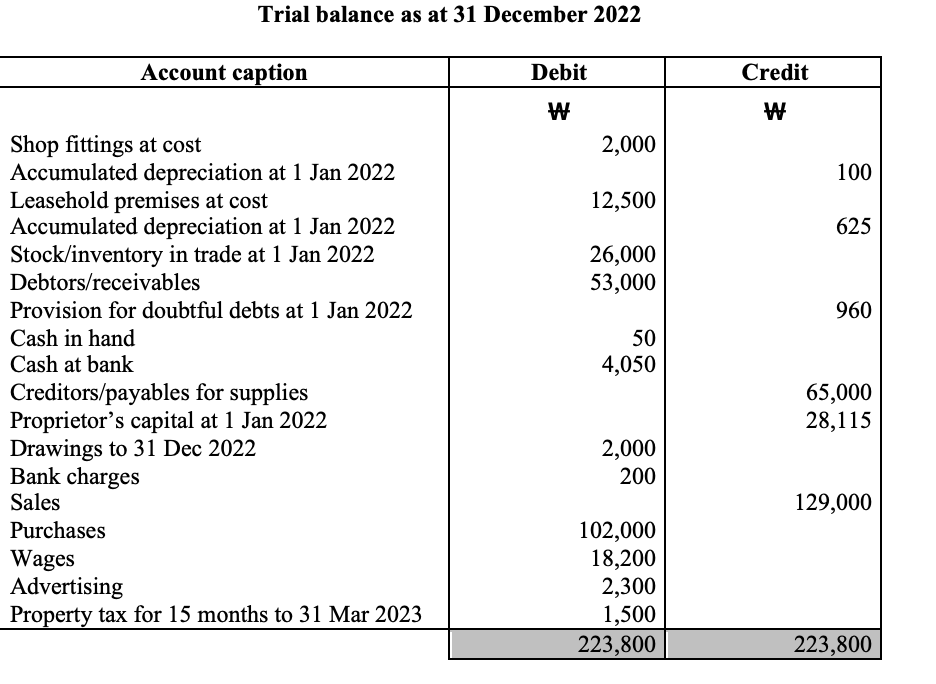

Balance Sheet

회계학은 분류, 또 분류다!!

분류기준을 다시 떠올려 보자면,

Assets

- Non current Asset

- Current Asset

- Inventories- Trade receivables

- Prepayments

- Cash at bank

- Cash in hand

Liability

-

Non current Liability

-

Current Liability

- Trade payables

Equity

가 있다.

Equity

저번의 Simon의 예시에선, Asset과 Liability를 구하고 그 공식의 결과로서 Equity를 구했다. 이번에는 Income Statement를 작성했으므로 그 결과인 Net Profit이 우리에게 있다.

한번 우리가 Equity를 만들어보자.

Equity = Opening equity capital + changes in equity capital + profit (revenue – expenses)

예시를 보니 Capital은 그냥 써 있다.

Proprietor's capital at 1 Jan 2022 : $28115

그리고, Drawing (주석과 Trial balance 에 있는 $3000) 은 (-)Equity 이다.

Equity is the net amount of funds invested in a business by its owners, plus any retained earnings.

Equity는 소유주가 직접 회사에 투자한 돈을 의미하므로, 직접 회사의 돈을 빼갔으면 Equity의 반대가 될 것이다.

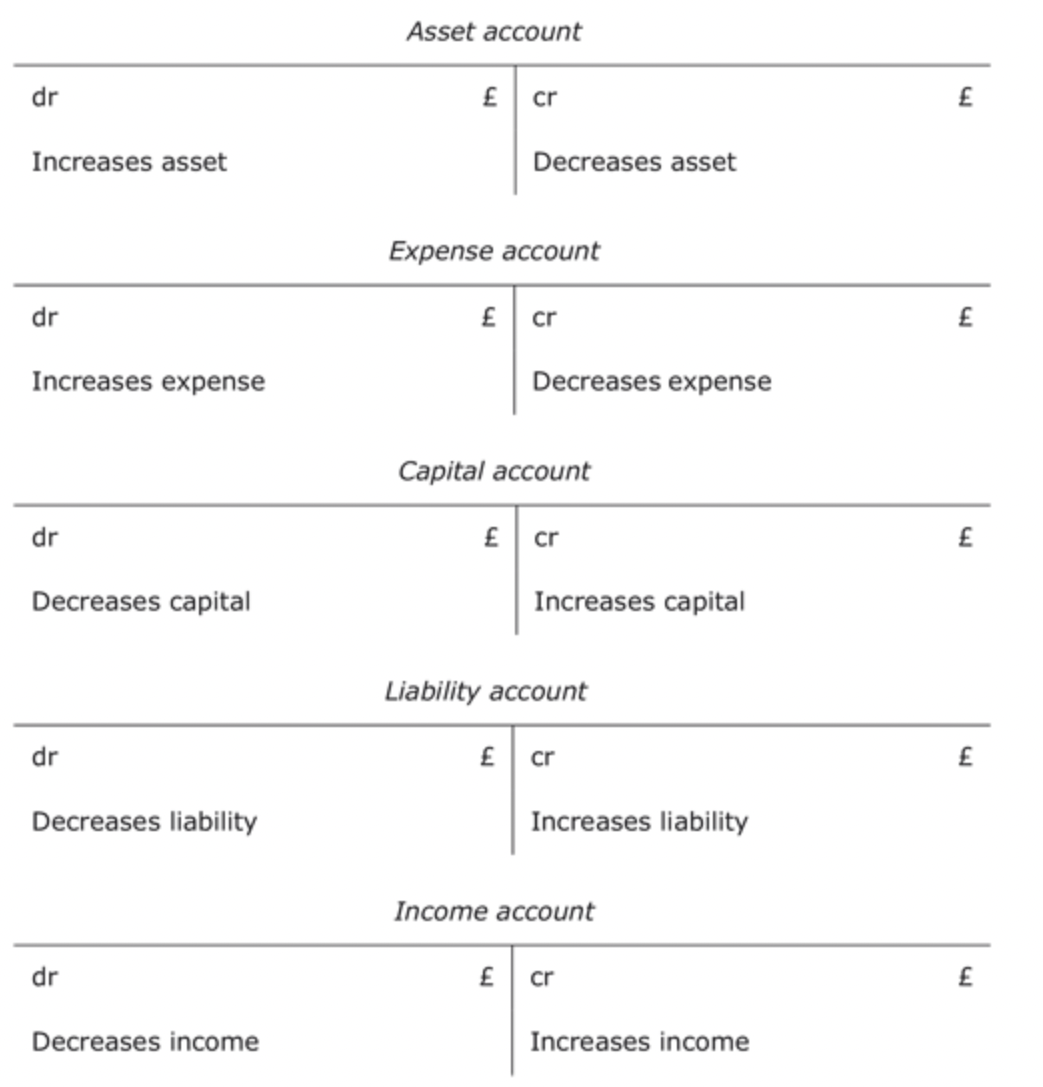

그런데 위의 double entry 표를 보면 어디에도 Capital은 없다. 공식을 변형해보면 그 의문에 답을 할 수 있다.

변형 공식

A – L= C+ (I – E)

A+ E =C+ L+ I

(Assets, Expenses, Capital, Liability, Income)

새로운 공식에 따라 Double Entry표를 변형해 보면,

이 표를 보면 Double Entry의 핵심 개념인,

Every transaction has a twofold effect / double entry

가 더 와닿을지도 모르겠다.

밑에서부터는 저번에 했던 내용과 크게 다르지 않은듯 하다.

Non current Assets

Shop fittings

Expense를 살펴보았던 income statment과는 다르게, 여기선 Asset의 가치를 다룬다.

Value - decipriated value 로 말이다. Trial balance 에 적혀있는 것은, 처음의 가치이다.

아까 계산한 저번년도, 그리고 이번년도 decipriation을 빼주어야 한다.

그래서 $2000 - 100 - 100 => $1800

Leasehold

위와 별 다를 것이 없다.

$12500 - $625 - $625 = 11250

Current Assets

Inventories

(d)주석에 매우 친절하게 30000원이라고 쓰여있다.

Trade receivables

53000원을 그대로 넣으면 좋겠지만, Bad debt와 Provision을 빼주어야 한다.(Increased provision, (b)를 참고해서 말이다.)

$53000 - 500 - 1050 => 51450

Prepayments

아까 1500원의 tax를 미리 냈던 것을 기억하는가? 남은 300원의 가치는 아직 사용하지 않은, Prepayment로 취급된다.

Simon이 가지 않은, 21 번의 대회 중 10번의 대회가 Asset으로 가치를 가지는 것처럼 말이다.

Cash

cash at bank <= $4050

cash at hand <= $ 50

Current Liabilities

Trade payables

$ 65000

끝!

휴 힘들었다 !

٩(◕ᗜ◕)و