Online Shoppers Purchasing Intention Dataset Data Set

데이터는 총 18개의 칼럼과 12330개의 rows로 구성

| Header | Description |

|---|---|

| Administrative | This is the number of pages of this type (administrative) that the user visited. |

| Administrative_Duration | This is the amount of time spent in this category of pages. |

| Informational | This is the number of pages of this type (informational) that the user visited. |

| Informational_Duration | This is the amount of time spent in this category of pages. |

| ProductRelated | This is the number of pages of this type (product related) that the user visited. |

| ProductRelated_Duration | This is the amount of time spent in this category of pages. |

| BounceRates | The percentage of visitors who enter the website through that page and exit without triggering any additional tasks. |

| ExitRates | The percentage of pageviews on the website that end at that specific page. |

| PageValues | The average value of the page averaged over the value of the target page and/or the completion of an eCommerce |

| SpecialDay | This value represents the closeness of the browsing date to special days or holidays (eg Mother's Day or Valentine's day) in |

| Month | Contains the month the pageview occurred, in string form. |

| OperatingSystems | An integer value representing the operating system that the user was on when viewing the page. |

| Browser | An integer value representing the browser that the user was using to view the page. |

| Region | An integer value representing which region the user is located in. |

| TrafficType | An integer value representing what type of traffic the user is categorized into. |

| VisitorType | A string representing whether a visitor is New Visitor, Returning Visitor, or Other. |

| Weekend | A boolean representing whether the session is on a weekend. |

| Revenue | A boolean representing whether or not the user completed the purchase. |

EDA

- 데이터를 불러오고 기본적인 정보를 보자.

library(knitr)

library(rmarkdown)

getwd()

## [1] "/Users/leehyebin/Desktop"

setwd("/Users/leehyebin/Rdata")

df <- read.csv('online_shoppers_intention.csv', stringsAsFactors = TRUE)

head(df)

## Administrative Administrative_Duration Informational Informational_Duration

## 1 0 0 0 0

## 2 0 0 0 0

## 3 0 0 0 0

## 4 0 0 0 0

## 5 0 0 0 0

## 6 0 0 0 0

## ProductRelated ProductRelated_Duration BounceRates ExitRates PageValues

## 1 1 0.000000 0.20000000 0.2000000 0

## 2 2 64.000000 0.00000000 0.1000000 0

## 3 1 0.000000 0.20000000 0.2000000 0

## 4 2 2.666667 0.05000000 0.1400000 0

## 5 10 627.500000 0.02000000 0.0500000 0

## 6 19 154.216667 0.01578947 0.0245614 0

## SpecialDay Month OperatingSystems Browser Region TrafficType

## 1 0 Feb 1 1 1 1

## 2 0 Feb 2 2 1 2

## 3 0 Feb 4 1 9 3

## 4 0 Feb 3 2 2 4

## 5 0 Feb 3 3 1 4

## 6 0 Feb 2 2 1 3

## VisitorType Weekend Revenue

## 1 Returning_Visitor FALSE FALSE

## 2 Returning_Visitor FALSE FALSE

## 3 Returning_Visitor FALSE FALSE

## 4 Returning_Visitor FALSE FALSE

## 5 Returning_Visitor TRUE FALSE

## 6 Returning_Visitor FALSE FALSE

str(df)

## 'data.frame': 12330 obs. of 18 variables:

## $ Administrative : int 0 0 0 0 0 0 0 1 0 0 ...

## $ Administrative_Duration: num 0 0 0 0 0 0 0 0 0 0 ...

## $ Informational : int 0 0 0 0 0 0 0 0 0 0 ...

## $ Informational_Duration : num 0 0 0 0 0 0 0 0 0 0 ...

## $ ProductRelated : int 1 2 1 2 10 19 1 0 2 3 ...

## $ ProductRelated_Duration: num 0 64 0 2.67 627.5 ...

## $ BounceRates : num 0.2 0 0.2 0.05 0.02 ...

## $ ExitRates : num 0.2 0.1 0.2 0.14 0.05 ...

## $ PageValues : num 0 0 0 0 0 0 0 0 0 0 ...

## $ SpecialDay : num 0 0 0 0 0 0 0.4 0 0.8 0.4 ...

## $ Month : Factor w/ 10 levels "Aug","Dec","Feb",..: 3 3 3 3 3 3 3 3 3 3 ...

## $ OperatingSystems : int 1 2 4 3 3 2 2 1 2 2 ...

## $ Browser : int 1 2 1 2 3 2 4 2 2 4 ...

## $ Region : int 1 1 9 2 1 1 3 1 2 1 ...

## $ TrafficType : int 1 2 3 4 4 3 3 5 3 2 ...

## $ VisitorType : Factor w/ 3 levels "New_Visitor",..: 3 3 3 3 3 3 3 3 3 3 ...

## $ Weekend : logi FALSE FALSE FALSE FALSE TRUE FALSE ...

## $ Revenue : logi FALSE FALSE FALSE FALSE FALSE FALSE ...

df$Region <- as.factor(df$Region)

df$TrafficType <- as.factor(df$TrafficType)

df$Weekend <- as.factor(df$Weekend)

df$Revenue <- as.factor(df$Revenue)

df$OperatingSystems <- as.factor(df$OperatingSystems)

summary(df)

## Administrative Administrative_Duration Informational

## Min. : 0.000 Min. : 0.00 Min. : 0.0000

## 1st Qu.: 0.000 1st Qu.: 0.00 1st Qu.: 0.0000

## Median : 1.000 Median : 7.50 Median : 0.0000

## Mean : 2.315 Mean : 80.82 Mean : 0.5036

## 3rd Qu.: 4.000 3rd Qu.: 93.26 3rd Qu.: 0.0000

## Max. :27.000 Max. :3398.75 Max. :24.0000

##

## Informational_Duration ProductRelated ProductRelated_Duration

## Min. : 0.00 Min. : 0.00 Min. : 0.0

## 1st Qu.: 0.00 1st Qu.: 7.00 1st Qu.: 184.1

## Median : 0.00 Median : 18.00 Median : 598.9

## Mean : 34.47 Mean : 31.73 Mean : 1194.8

## 3rd Qu.: 0.00 3rd Qu.: 38.00 3rd Qu.: 1464.2

## Max. :2549.38 Max. :705.00 Max. :63973.5

##

## BounceRates ExitRates PageValues SpecialDay

## Min. :0.000000 Min. :0.00000 Min. : 0.000 Min. :0.00000

## 1st Qu.:0.000000 1st Qu.:0.01429 1st Qu.: 0.000 1st Qu.:0.00000

## Median :0.003112 Median :0.02516 Median : 0.000 Median :0.00000

## Mean :0.022191 Mean :0.04307 Mean : 5.889 Mean :0.06143

## 3rd Qu.:0.016813 3rd Qu.:0.05000 3rd Qu.: 0.000 3rd Qu.:0.00000

## Max. :0.200000 Max. :0.20000 Max. :361.764 Max. :1.00000

##

## Month OperatingSystems Browser Region TrafficType

## May :3364 2 :6601 Min. : 1.000 1 :4780 2 :3913

## Nov :2998 1 :2585 1st Qu.: 2.000 3 :2403 1 :2451

## Mar :1907 3 :2555 Median : 2.000 4 :1182 3 :2052

## Dec :1727 4 : 478 Mean : 2.357 2 :1136 4 :1069

## Oct : 549 8 : 79 3rd Qu.: 2.000 6 : 805 13 : 738

## Sep : 448 6 : 19 Max. :13.000 7 : 761 10 : 450

## (Other):1337 (Other): 13 (Other):1263 (Other):1657

## VisitorType Weekend Revenue

## New_Visitor : 1694 FALSE:9462 FALSE:10422

## Other : 85 TRUE :2868 TRUE : 1908

## Returning_Visitor:10551

##

##

##

##

dim(df)

## [1] 12330 18

sum(is.na(df))

## [1] 0NA값은 없으며 결과변수 ’Revenue’가 FALSE는 10422건, TRUE가 1908건으로 불균형 데이터이다.

- Month변수의 factor순서를 보기 편하게 재배열하자.

levels(df$Month)

## [1] "Aug" "Dec" "Feb" "Jul" "June" "Mar" "May" "Nov" "Oct" "Sep"

df$Month <- factor(df$Month, levels=levels(df$Month)[c(3, 6, 7, 5, 4, 1, 10, 9, 8, 2)])

levels(df$Month)

## [1] "Feb" "Mar" "May" "June" "Jul" "Aug" "Sep" "Oct" "Nov" "Dec"- EDA에 필요한 패키지들을 불러오자.

library(DMwR2)

## Registered S3 method overwritten by 'quantmod':

## method from

## as.zoo.data.frame zoo

library(pastecs)

library(psych)

library(caret)

## Loading required package: ggplot2

##

## Attaching package: 'ggplot2'

## The following objects are masked from 'package:psych':

##

## %+%, alpha

## Loading required package: lattice

library(ggplot2)

library(GGally)

## Registered S3 method overwritten by 'GGally':

## method from

## +.gg ggplot2

library(smotefamily)

library(naniar)

library(reshape2)

library(gridExtra)

library(gapminder)

library(dplyr)

##

## Attaching package: 'dplyr'

## The following object is masked from 'package:gridExtra':

##

## combine

## The following objects are masked from 'package:pastecs':

##

## first, last

## The following objects are masked from 'package:stats':

##

## filter, lag

## The following objects are masked from 'package:base':

##

## intersect, setdiff, setequal, union

library(PerformanceAnalytics)

## Loading required package: xts

## Loading required package: zoo

##

## Attaching package: 'zoo'

## The following objects are masked from 'package:base':

##

## as.Date, as.Date.numeric

##

## Attaching package: 'xts'

## The following objects are masked from 'package:dplyr':

##

## first, last

## The following objects are masked from 'package:pastecs':

##

## first, last

##

## Attaching package: 'PerformanceAnalytics'

## The following object is masked from 'package:graphics':

##

## legend

library(FSelector)

library(Boruta)

library(ROSE)

## Loaded ROSE 0.0-4- 탐색적 분석으로 첨도 및 왜도를 알아보자.

describeBy(df[, -c(11, 12, 14, 15, 16, 17)], df$Revenue, mat = FALSE)

##

## Descriptive statistics by group

## group: FALSE

## vars n mean sd median trimmed mad min

## Administrative 1 10422 2.12 3.20 0.00 1.43 0.00 0

## Administrative_Duration 2 10422 73.74 171.02 0.00 36.51 0.00 0

## Informational 3 10422 0.45 1.21 0.00 0.14 0.00 0

## Informational_Duration 4 10422 30.24 133.91 0.00 2.39 0.00 0

## ProductRelated 5 10422 28.71 40.74 16.00 20.62 17.79 0

## ProductRelated_Duration 6 10422 1069.99 1803.80 510.19 726.48 650.90 0

## BounceRates 7 10422 0.03 0.05 0.00 0.01 0.01 0

## ExitRates 8 10422 0.05 0.05 0.03 0.04 0.02 0

## PageValues 9 10422 1.98 9.07 0.00 0.03 0.00 0

## SpecialDay 10 10422 0.07 0.21 0.00 0.00 0.00 0

## Browser 11 10422 2.34 1.68 2.00 1.99 0.00 1

## Revenue* 12 10422 1.00 0.00 1.00 1.00 0.00 1

## max range skew kurtosis se

## Administrative 27.00 27.00 2.09 5.48 0.03

## Administrative_Duration 3398.75 3398.75 6.10 60.03 1.68

## Informational 24.00 24.00 4.45 33.92 0.01

## Informational_Duration 2549.38 2549.38 8.43 94.32 1.31

## ProductRelated 705.00 705.00 4.69 38.81 0.40

## ProductRelated_Duration 63973.52 63973.52 8.83 196.97 17.67

## BounceRates 0.20 0.20 2.66 5.97 0.00

## ExitRates 0.20 0.20 1.94 2.97 0.00

## PageValues 246.76 246.76 9.56 147.98 0.09

## SpecialDay 1.00 1.00 3.08 8.41 0.00

## Browser 13.00 12.00 3.24 12.82 0.02

## Revenue* 1.00 0.00 NaN NaN 0.00

## ------------------------------------------------------------

## group: TRUE

## vars n mean sd median trimmed mad min

## Administrative 1 1908 3.39 3.73 2.00 2.78 2.97 0

## Administrative_Duration 2 1908 119.48 201.11 52.37 76.18 77.64 0

## Informational 3 1908 0.79 1.52 0.00 0.42 0.00 0

## Informational_Duration 4 1908 57.61 171.62 0.00 14.44 0.00 0

## ProductRelated 5 1908 48.21 58.27 29.00 36.26 25.20 0

## ProductRelated_Duration 6 1908 1876.21 2312.21 1109.91 1410.82 1040.40 0

## BounceRates 7 1908 0.01 0.01 0.00 0.00 0.00 0

## ExitRates 8 1908 0.02 0.02 0.02 0.02 0.01 0

## PageValues 9 1908 27.26 35.19 16.76 20.87 23.93 0

## SpecialDay 10 1908 0.02 0.12 0.00 0.00 0.00 0

## Browser 11 1908 2.45 1.90 2.00 2.05 0.00 1

## Revenue* 12 1908 2.00 0.00 2.00 2.00 0.00 2

## max range skew kurtosis se

## Administrative 26.00 26.00 1.45 2.40 0.09

## Administrative_Duration 2086.75 2086.75 3.98 23.06 4.60

## Informational 12.00 12.00 2.69 9.25 0.03

## Informational_Duration 1767.67 1767.67 4.97 31.07 3.93

## ProductRelated 534.00 534.00 3.25 15.00 1.33

## ProductRelated_Duration 27009.86 27009.86 3.33 17.65 52.93

## BounceRates 0.20 0.20 8.26 109.82 0.00

## ExitRates 0.20 0.20 3.47 25.84 0.00

## PageValues 361.76 361.76 3.25 17.85 0.81

## SpecialDay 1.00 1.00 5.78 34.37 0.00

## Browser 13.00 12.00 3.18 11.72 0.04

## Revenue* 2.00 0.00 NaN NaN 0.00FALSE그룹의 Administrative_Duration, Informational, Informational_Duration, ProductRelated, ProductRelated_Duration, PageValues변수의 첨도가 모두 30이상으로 굉장히 뾰족한 분포를 보일 것으로 예상된다. 또한 모든 수치형 변수의 왜도가 0보다 큰 양수로 왼쪽으로 치우친 분포를 보일 것으로 예상된다.

TRUE그룹을 보면 Informational_Duration, BounceRates, SpecialDay변수만 30이 넘는 첨도를 보여 FALSE그룹과 차이나는 분포를 보이고 있음을 알 수 있다. TRUE그룹의 왜도 또한 모두 0보다 큰 양수로 왼쪽으로 치우친 분포를 보인다.

- 그래프로 변수별 분포를 확인해보자.

– 수치형 변수와 팩터형 변수를 따로 확인해보자.

– 우선 수치형 변수의 분포를 2번에 걸쳐서 확인해보자.

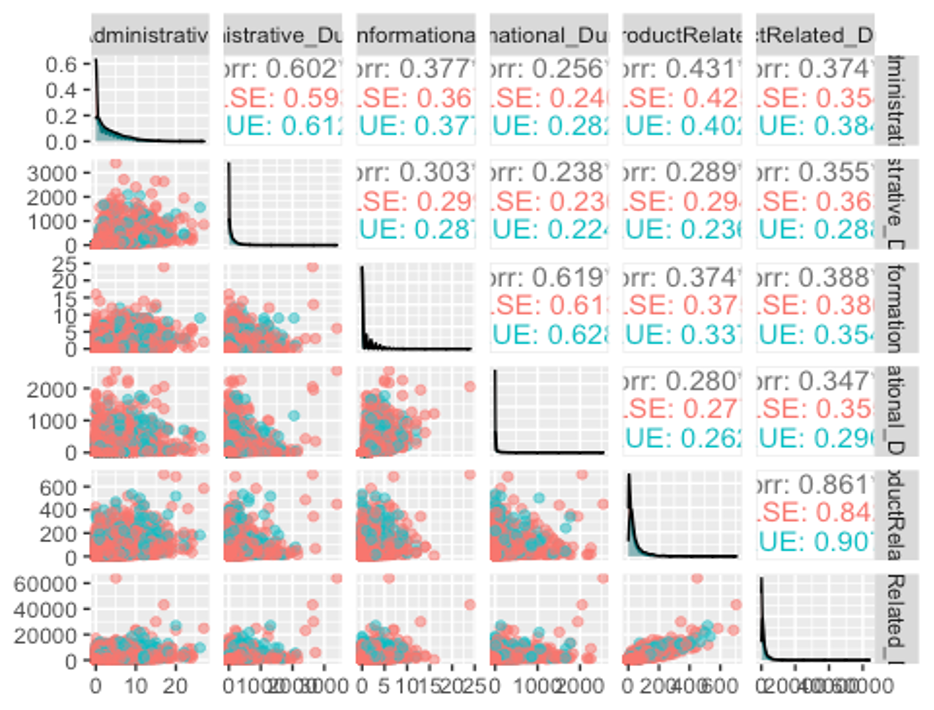

ggpairs(df, columns = c(1, 2, 3, 4, 5, 6), aes(colour = Revenue, alpha = 0.4))

위에서 보았듯이 모든 변수가 왼쪽으로 치우친 분포를 보이고 있고, Administrative_Duration, Informational, ProductRelated, ProductRelated_Duration변수는 FALSE그룹이 TRUE그룹보다 훨씬 뾰족한 분포를 보이고 있다.

- 나머지 수치형 변수들의 분포를 그려보자.

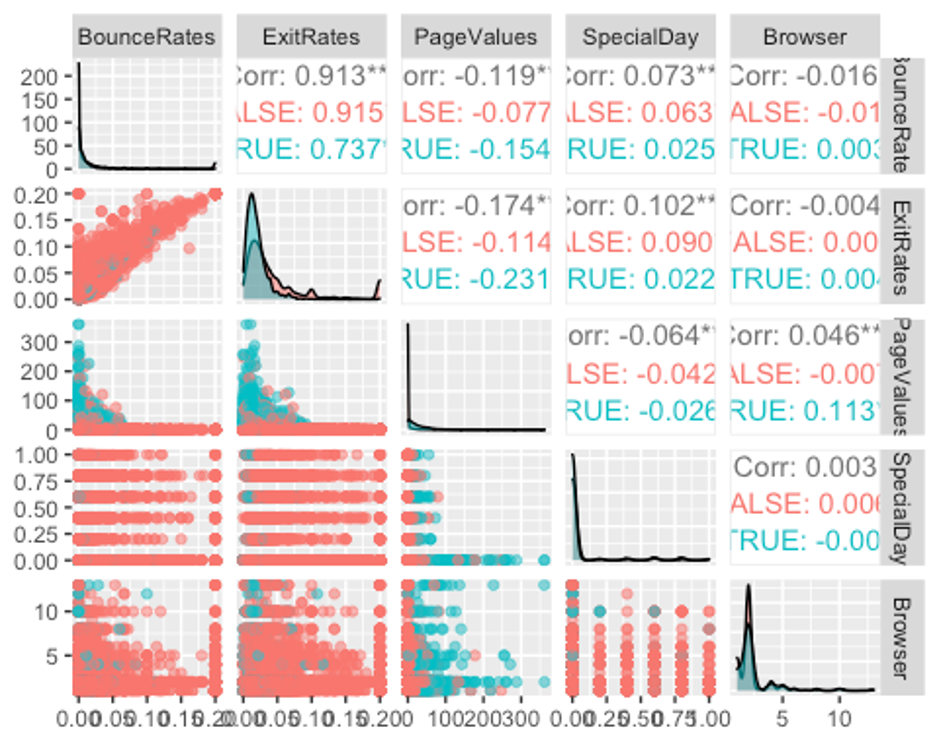

ggpairs(df, columns = c(7, 8, 9, 10, 13), aes(colour = Revenue, alpha = 0.4))

역시 모든 변수가 왼쪽으로 치우친 분포를 보이고 있으며, BounceRates, ExitRates, SpecialDay변수는 FALSE그룹보다 TRUE그룹이 뾰족한 분포를 보이고 있다.

- 다음으로 factor형 변수가 어떤 분포를 보이고 있는지 보자.

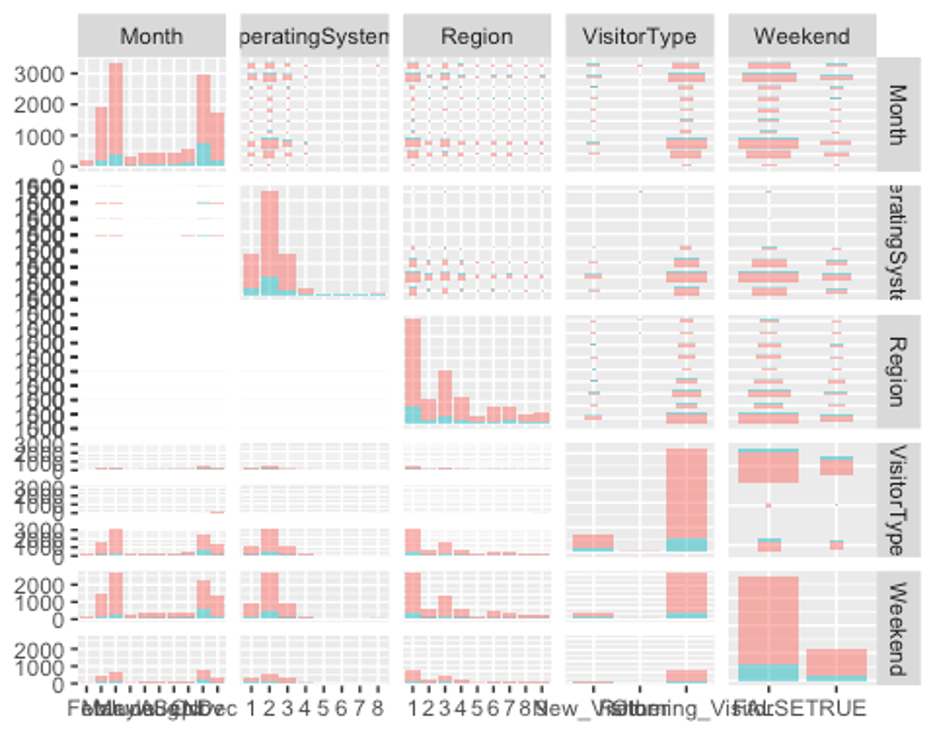

ggpairs(df, columns = c(11, 12, 14, 16, 17), aes(colour = Revenue, alpha = 0.4))

Month변수의 분포를 보면 구매 사실(Revenue변수에서 TRUE그룹)이 11월에 가장 높고, 2월에 가장 낮은 것으로 보인다. 단순한 홈페이지 방문자 수는 5월에 가장 높았다. 이는 월별 이벤트(5월의 Mother’s Day, 11월의 추수감사절, 12월의 크리스마스 등)가 홈페이지 방문자 수와 구매 여부에 상관관계가 있음을 암시한다.

Region변수의 분포를 보면 1지역에서 홈페이지 방문자수도 가장 많고, 구매도 가장 많다. VisitorType변수의 분포는 신규 고객보다 재방문 고객이 5배 이상 많았다. 또한 주말보다 평일에 홈페이지를 더 많이 방문하고 구매하는 것으로 보인다.

- 이제 수치형 변수에 이상치가 있는지 확인해보자.

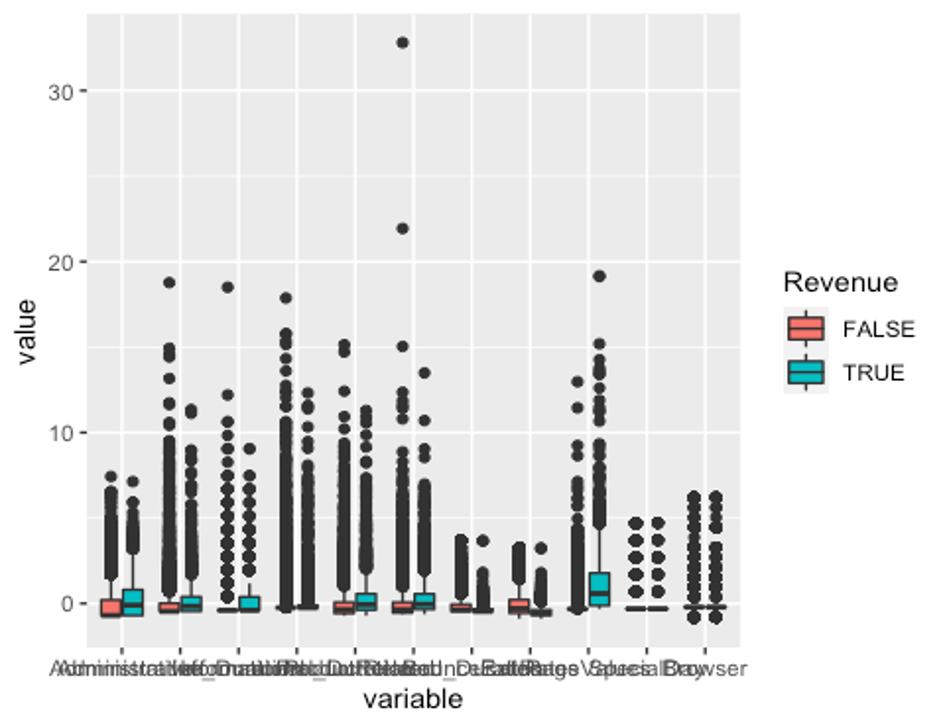

– 데이터의 범위가 변수별로 차이 나므로 평균이 0, 분산이 1이 되도록 스케일링 하고 데이터를 wide형식에서 long형식으로 바꿔주자.

df_numeric <- df[, c(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 13, 18)]

model_scale <- preProcess(df_numeric, method = c('center', 'scale'))

scaled_df <- predict(model_scale, df_numeric)

melt_df <- melt(scaled_df, id.vars = 'Revenue')

head(melt_df)

## Revenue variable value

## 1 FALSE Administrative -0.6969647

## 2 FALSE Administrative -0.6969647

## 3 FALSE Administrative -0.6969647

## 4 FALSE Administrative -0.6969647

## 5 FALSE Administrative -0.6969647

## 6 FALSE Administrative -0.6969647

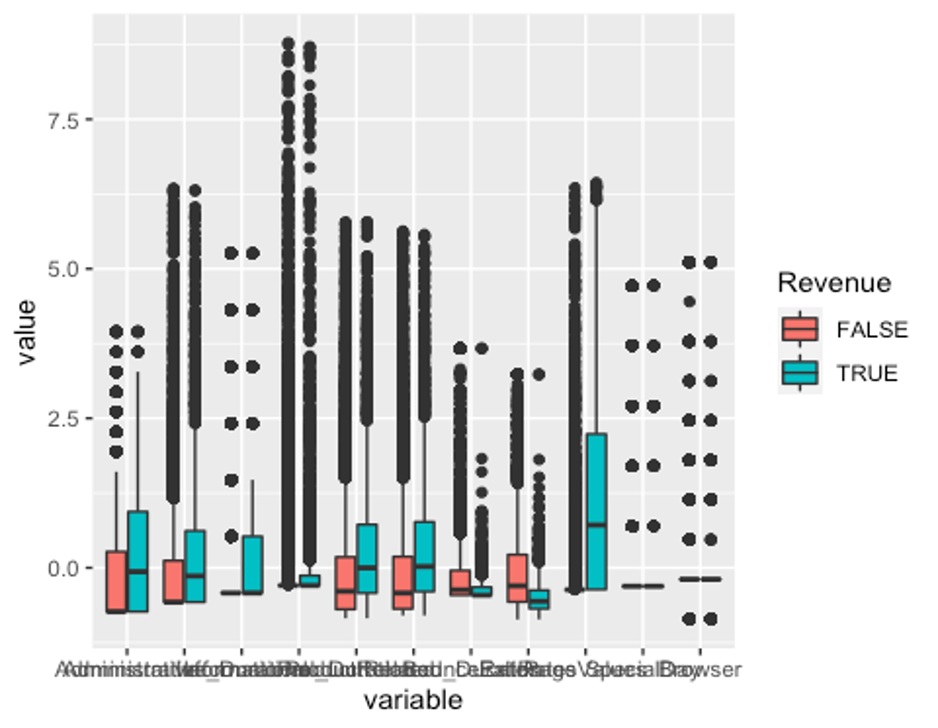

p1 <- ggplot(melt_df, aes(x = variable, y = value, fill = Revenue)) + geom_boxplot()

p1

모든 수치형 변수에 이상치가 있다.

- 사분위수 99% 범위 밖의 이상치는 75% 사분위수로 바꿔주고, 1%내의 이상치는 25% 사분위수로 바꿔준다.

outHigh <- function(x){

x[x > quantile(x, 0.99)] <- quantile(x, 0.75)

x

}

outLow <- function(x){

x[x < quantile(x, 0.01)] <- quantile(x, 0.25)

x

}

df_2 <- data.frame(lapply(df[, -c(11, 12, 14, 15, 16, 17, 18)], outHigh))

df_2 <- data.frame(lapply(df_2, outLow))

df_2$Month <- df$Month

df_2$OperatingSystems <- df$OperatingSystems

df_2$Region <- df$Region

df_2$TrafficType <- df$TrafficType

df_2$VisitorType <- df$VisitorType

df_2$Weekend <- df$Weekend

df_2$Revenue <- df$Revenue- 이상치 변경 후의 boxplot을 다시 그려보자.

df_numeric2 <- df_2[, -c(12:17)]

model_scale2 <- preProcess(df_numeric2, method = c('center', 'scale'))

scaled_df2 <- predict(model_scale2, df_numeric2)

melt_df2 <- melt(scaled_df2, id.vars = 'Revenue')

head(melt_df2)

## Revenue variable value

## 1 FALSE Administrative -0.7336044

## 2 FALSE Administrative -0.7336044

## 3 FALSE Administrative -0.7336044

## 4 FALSE Administrative -0.7336044

## 5 FALSE Administrative -0.7336044

## 6 FALSE Administrative -0.7336044

p2 <- ggplot(melt_df2, aes(x = variable, y = value, fill = Revenue)) + geom_boxplot()

p2

잘 변경된 것으로 보인다.

- 변수들의 상관관계를 확인하자.

str(df_numeric2)

## 'data.frame': 12330 obs. of 12 variables:

## $ Administrative : num 0 0 0 0 0 0 0 1 0 0 ...

## $ Administrative_Duration: num 0 0 0 0 0 0 0 0 0 0 ...

## $ Informational : num 0 0 0 0 0 0 0 0 0 0 ...

## $ Informational_Duration : num 0 0 0 0 0 0 0 0 0 0 ...

## $ ProductRelated : num 1 2 1 2 10 19 1 7 2 3 ...

## $ ProductRelated_Duration: num 0 64 0 2.67 627.5 ...

## $ BounceRates : num 0.2 0 0.2 0.05 0.02 ...

## $ ExitRates : num 0.2 0.1 0.2 0.14 0.05 ...

## $ PageValues : num 0 0 0 0 0 0 0 0 0 0 ...

## $ SpecialDay : num 0 0 0 0 0 0 0.4 0 0.8 0.4 ...

## $ Browser : num 1 2 1 2 3 2 4 2 2 4 ...

## $ Revenue : Factor w/ 2 levels "FALSE","TRUE": 1 1 1 1 1 1 1 1 1 1 ...

df_numeric2 <- df_numeric2[, -12]

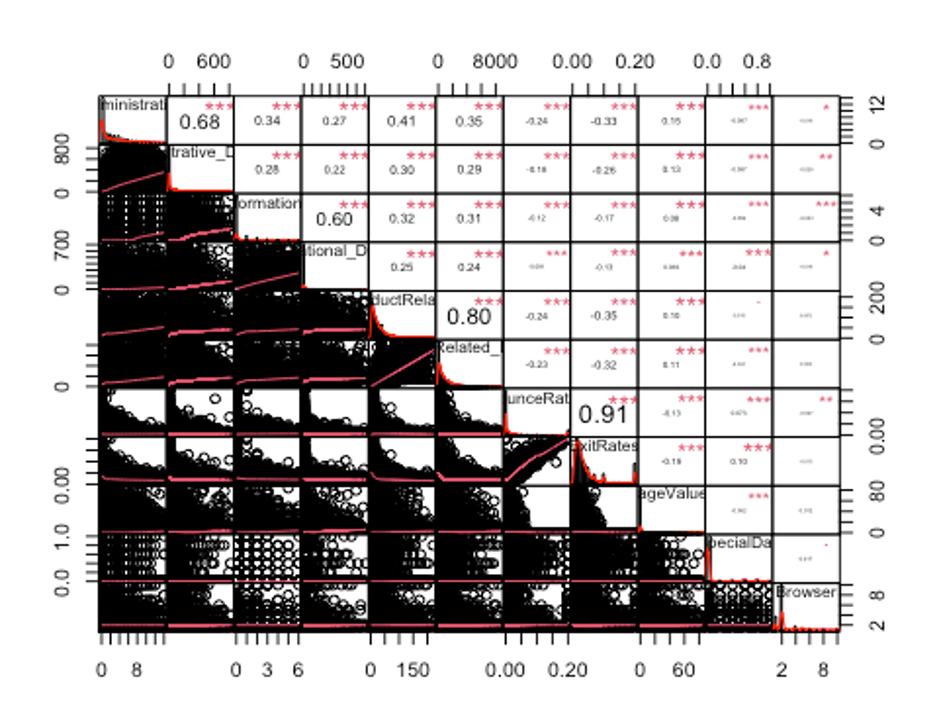

cor_df <- cor(df_numeric2)

chart.Correlation(df_numeric2, histogram = TRUE, pch = 19, method = 'pearson')

보통 상관계수의 절댓값이 0.7보다 크면 강한 상관관계가 있다고 보고, 0.3보다 크면 약한 상관관계가 있다고 본다. 상관계수가 0.3보다 작으면 일반적으로 상관관계가 없다고 해석한다. 독립변수 간에 선형 상관관계가 존재하는 경우 다중공선성이 있다고 얘기하는데, 다중공선성이 있으면 독립변수 간에 선형상관관계가 있어서 회귀계수의 분산이 커진다. 그 결과 분석 결과가 불안정하게 되어 분석의 효과성이 감소하는 문제가 발생한다.

- 상관관계의 절댓값이 0.7이상인 변수를 제거하자.

findCorrelation(cor_df, cutoff = 0.7)

## [1] 5 8- df_numeric2에서 5번째 변수와 8번째 변수는 각각 ProductRelated변수와 ExitRates변수이므로 이 둘을 df_2에서 제거하자.

df_new <- df_2[, -c(5, 8)]

str(df_new)

## 'data.frame': 12330 obs. of 16 variables:

## $ Administrative : num 0 0 0 0 0 0 0 1 0 0 ...

## $ Administrative_Duration: num 0 0 0 0 0 0 0 0 0 0 ...

## $ Informational : num 0 0 0 0 0 0 0 0 0 0 ...

## $ Informational_Duration : num 0 0 0 0 0 0 0 0 0 0 ...

## $ ProductRelated_Duration: num 0 64 0 2.67 627.5 ...

## $ BounceRates : num 0.2 0 0.2 0.05 0.02 ...

## $ PageValues : num 0 0 0 0 0 0 0 0 0 0 ...

## $ SpecialDay : num 0 0 0 0 0 0 0.4 0 0.8 0.4 ...

## $ Browser : num 1 2 1 2 3 2 4 2 2 4 ...

## $ Month : Factor w/ 10 levels "Feb","Mar","May",..: 1 1 1 1 1 1 1 1 1 1 ...

## $ OperatingSystems : Factor w/ 8 levels "1","2","3","4",..: 1 2 4 3 3 2 2 1 2 2 ...

## $ Region : Factor w/ 9 levels "1","2","3","4",..: 1 1 9 2 1 1 3 1 2 1 ...

## $ TrafficType : Factor w/ 20 levels "1","2","3","4",..: 1 2 3 4 4 3 3 5 3 2 ...

## $ VisitorType : Factor w/ 3 levels "New_Visitor",..: 3 3 3 3 3 3 3 3 3 3 ...

## $ Weekend : Factor w/ 2 levels "FALSE","TRUE": 1 1 1 1 2 1 1 2 1 1 ...

## $ Revenue : Factor w/ 2 levels "FALSE","TRUE": 1 1 1 1 1 1 1 1 1 1 ...- 다음으로 분산이 0에 가까운 변수를 제거하자.

nearZeroVar(df_new, saveMetrics = TRUE)

## freqRatio percentUnique zeroVar nzv

## Administrative 4.259970 0.1216545 FALSE FALSE

## Administrative_Duration 47.604839 26.0583942 FALSE FALSE

## Informational 9.396734 0.0567721 FALSE FALSE

## Informational_Duration 304.515152 9.2133009 FALSE TRUE

## ProductRelated_Duration 6.088710 76.4639092 FALSE FALSE

## BounceRates 7.882857 15.1824818 FALSE FALSE

## PageValues 1620.666667 20.9326845 FALSE FALSE

## SpecialDay 31.564103 0.0486618 FALSE TRUE

## Browser 3.264825 0.0811030 FALSE FALSE

## Month 1.122081 0.0811030 FALSE FALSE

## OperatingSystems 2.553578 0.0648824 FALSE FALSE

## Region 1.989180 0.0729927 FALSE FALSE

## TrafficType 1.596491 0.1622060 FALSE FALSE

## VisitorType 6.228453 0.0243309 FALSE FALSE

## Weekend 3.299163 0.0162206 FALSE FALSE

## Revenue 5.462264 0.0162206 FALSE FALSE

df_new2 <- df_new[, -nearZeroVar(df_new)]

str(df_new2)

## 'data.frame': 12330 obs. of 14 variables:

## $ Administrative : num 0 0 0 0 0 0 0 1 0 0 ...

## $ Administrative_Duration: num 0 0 0 0 0 0 0 0 0 0 ...

## $ Informational : num 0 0 0 0 0 0 0 0 0 0 ...

## $ ProductRelated_Duration: num 0 64 0 2.67 627.5 ...

## $ BounceRates : num 0.2 0 0.2 0.05 0.02 ...

## $ PageValues : num 0 0 0 0 0 0 0 0 0 0 ...

## $ Browser : num 1 2 1 2 3 2 4 2 2 4 ...

## $ Month : Factor w/ 10 levels "Feb","Mar","May",..: 1 1 1 1 1 1 1 1 1 1 ...

## $ OperatingSystems : Factor w/ 8 levels "1","2","3","4",..: 1 2 4 3 3 2 2 1 2 2 ...

## $ Region : Factor w/ 9 levels "1","2","3","4",..: 1 1 9 2 1 1 3 1 2 1 ...

## $ TrafficType : Factor w/ 20 levels "1","2","3","4",..: 1 2 3 4 4 3 3 5 3 2 ...

## $ VisitorType : Factor w/ 3 levels "New_Visitor",..: 3 3 3 3 3 3 3 3 3 3 ...

## $ Weekend : Factor w/ 2 levels "FALSE","TRUE": 1 1 1 1 2 1 1 2 1 1 ...

## $ Revenue : Factor w/ 2 levels "FALSE","TRUE": 1 1 1 1 1 1 1 1 1 1 ...Informational_Duration, SpecialDay변수의 분산이 0에 가까운 것으로 나타나 데이터프레임에서 제거하였다.

- 데이터를 train데이터와 test데이터로 분리한다.

idx <- createDataPartition(df_new2$Revenue, p = 0.7)

train <- df[idx$Resample1, ]

test <- df[-idx$Resample1, ]

table(train$Revenue)

##

## FALSE TRUE

## 7296 1336결과변수 Revenue의 범주가 약 5.5배 차이로 불균형 데이터이다.

- ROSE(random over sampling examples) 기법을 이용해 불균형 문제를 해결해보자

train_ROSE <- ROSE(Revenue ~., data = train, seed = 123)$data

table(train$Revenue)

##

## FALSE TRUE

## 7296 1336

table(train_ROSE$Revenue)

##

## FALSE TRUE

## 4366 4266- 데이터 스케일링을 진행해보자.

model_train <- preProcess(train_ROSE, method = 'range')

model_test <- preProcess(test, method = 'range')

scaled_train_ROSE <- predict(model_train, train_ROSE)

scaled_test <- predict(model_test, test)- factor형 변수들을 더미 변수로 만들어주자.

dummies <- dummyVars(Revenue ~., data = train_ROSE)

train_ROSE_dummy <- as.data.frame(predict(dummies, newdata = train_ROSE))

train_ROSE_dummy$Revenue <- train_ROSE$Revenue

dummies2 <- dummyVars(Revenue ~., data = scaled_train_ROSE)

scaled_train_ROSE_dummy <- as.data.frame(predict(dummies2, newdata = scaled_train_ROSE))

scaled_train_ROSE_dummy$Revenue <- scaled_train_ROSE$Revenue

dummies3 <- dummyVars(Revenue ~., data = test)

test_dummy <- as.data.frame(predict(dummies3, newdata = test))

test_dummy$Revenue <- test$Revenue

dummies4 <- dummyVars(Revenue ~., data = scaled_test)

scaled_test_dummy <- as.data.frame(predict(dummies4, newdata = scaled_test))

scaled_test_dummy$Revenue <- scaled_test$Revenue세트1 - train_ROSE, test : 데이터스케일X, 더미변수화X

세트2 - scaled_train_ROSE, scaled_test : 데이터스케일O, 더미변수화X

세트3 - train_ROSE_dummy, test_dummy : 데이터스케일X, 더미변수화O

세트4 - scaled_train_ROSE_dummy, scaled_test_dummy : 데이터 스케일O, 더미변수화O

총 4개의 조합이 만들어졌다. 모델 훈련법에 따라 세트를 선택해 사용하자. 다만 모형 훈련에 더미 변수가 들어가면 다른 변수에 비해 과하게 반영될 여지가 있기 때문에 굳이 더미 변수를 사용해야 할 이유가 없다면 사용하지 않는 것이 좋다.

다변량 적응 회귀 스플라인(MARS)

- train_ROSE, test데이터 세트를 사용한다.

- 먼저 필요한 패키지들을 불러오자.

library(MASS)

##

## Attaching package: 'MASS'

## The following object is masked from 'package:dplyr':

##

## select

library(bestglm)

## Loading required package: leaps

library(earth)

## Loading required package: Formula

## Loading required package: plotmo

## Loading required package: plotrix

##

## Attaching package: 'plotrix'

## The following object is masked from 'package:psych':

##

## rescale

## Loading required package: TeachingDemos

library(ROCR)

library(car)

## Loading required package: carData

##

## Attaching package: 'car'

## The following object is masked from 'package:dplyr':

##

## recode

## The following object is masked from 'package:psych':

##

## logit- 모형을 만들어 보자.

set.seed(321)

earth.fit <- earth(Revenue ~., data = train_ROSE,

pmethod = 'cv', nfold = 10,

ncross = 3, degree = 1,

minspan = -1,

glm = list(family = binomial))

summary(earth.fit)

## Call: earth(formula=Revenue~., data=train_ROSE, pmethod="cv",

## glm=list(family=binomial), degree=1, nfold=10, ncross=3,

## minspan=-1)

##

## GLM coefficients

## TRUE

## (Intercept) -0.217794

## MonthMar -0.716594

## MonthNov 0.548364

## MonthDec -0.649609

## OperatingSystems2 0.007544

## TrafficType3 -0.470470

## TrafficType13 -0.615791

## VisitorTypeOther -1.528098

## VisitorTypeReturning_Visitor -0.288701

## h(1.82014-Administrative) 0.025182

## h(Administrative-1.82014) 0.026639

## h(53.774-Administrative_Duration) 0.002749

## h(Administrative_Duration-53.774) 0.000967

## h(0.299924-Informational) 0.310813

## h(Informational-0.299924) 0.120581

## h(16.8912-Informational_Duration) 0.005569

## h(Informational_Duration-16.8912) 0.000703

## h(26.4066-ProductRelated) 0.010541

## h(ProductRelated-26.4066) 0.005902

## h(0.00535212-BounceRates) -95.365506

## h(BounceRates-0.00535212) -56.603481

## h(0.0220586-ExitRates) -35.887553

## h(ExitRates-0.0220586) -34.425075

## h(3.94875-PageValues) 0.097953

## h(PageValues-3.94875) 0.098646

## h(0.00811794-SpecialDay) -4.593668

## h(SpecialDay-0.00811794) -1.307738

## h(2.02052-Browser) 0.347494

## h(Browser-2.02052) 0.157571

##

## GLM (family binomial, link logit):

## nulldev df dev df devratio AIC iters converged

## 11965.3 8631 5827.97 8603 0.513 5886 7 1

##

## Earth selected 29 of 29 terms, and 18 of 57 predictors (pmethod="cv")

## Termination condition: RSq changed by less than 0.001 at 29 terms

## Importance: PageValues, ExitRates, BounceRates, MonthNov, ...

## Number of terms at each degree of interaction: 1 28 (additive model)

## Earth GRSq 0.3992937 RSq 0.4070635 mean.oof.RSq 0.4035203 (sd 0.017)

##

## pmethod="backward" would have selected:

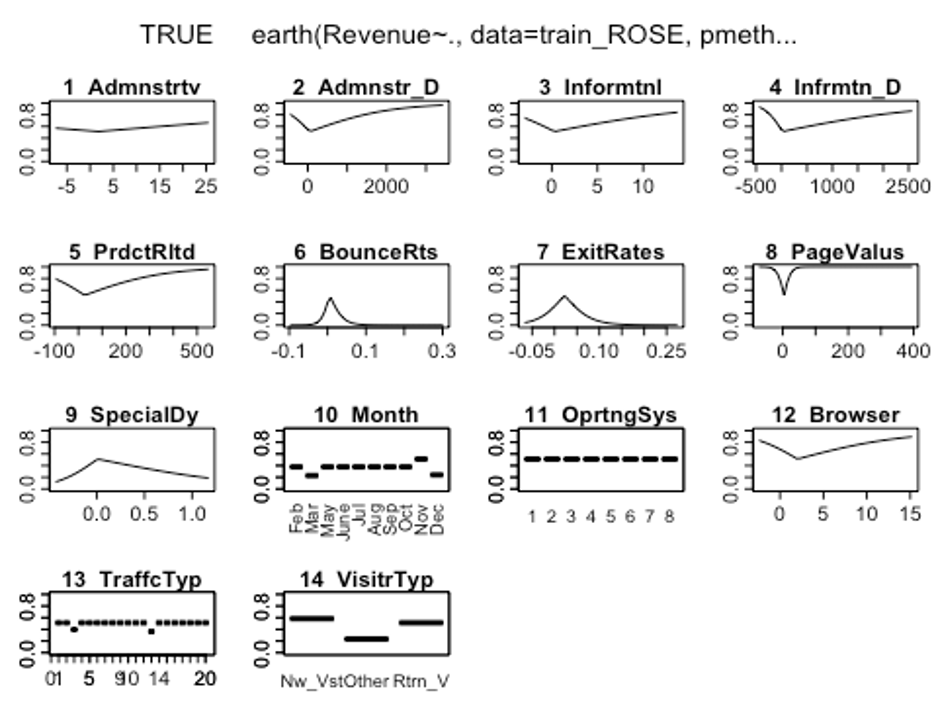

## 28 terms 18 preds, GRSq 0.3995216 RSq 0.4070119 mean.oof.RSq 0.4015694- plotmo()함수를 이용해 해당 예측 변수를 변화시키고 다른 변수들은 상수로 유지했을 때, 모형의 반응 변수가 변하는 양상을 보자.

plotmo(earth.fit)

## plotmo grid: Administrative Administrative_Duration Informational

## 1.82001 53.75336 0.2998683

## Informational_Duration ProductRelated ProductRelated_Duration BounceRates

## 16.88521 26.40348 1018.886 0.005349781

## ExitRates PageValues SpecialDay Month OperatingSystems Browser Region

## 0.02205257 3.945293 0.00810046 Nov 2 2.020514 1

## TrafficType VisitorType Weekend

## 2 Returning_Visitor FALSE

그래프를 보았을 때 OperatingSystems변수의 라벨에 따라서 반응변수가 크게 달라지지 않는 것으로 보인다.

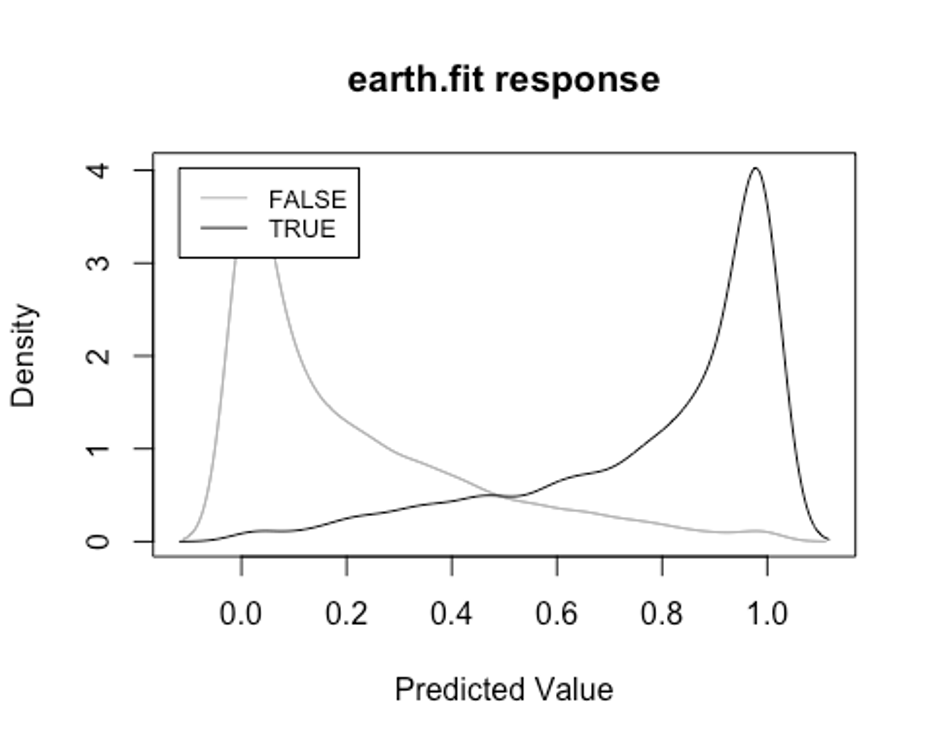

- plotd()함수를 이용해 결과변수 라벨(TRUE/FALSE)에 따른 예측 확률의 밀도 함수 도표를 보자.

plotd(earth.fit)

- evimp()함수로 상대적인 변수의 중요도를 살펴보자.

- nsubsets라는 변수명을 볼 수 있는데, 이는 가지치기 패스를 한 후에 남는 변수를 담고 있는 모형의 서브 세트 개수이다.

- gcv와 rss칼럼은 각 예측변수가 기여하는 각 감소값을 나타낸다.

evimp(earth.fit)

## nsubsets gcv rss

## PageValues 28 100.0 100.0

## ExitRates 27 76.3 76.8

## BounceRates 26 61.8 62.6

## MonthNov 23 47.0 48.1

## Informational_Duration 22 38.6 40.1

## ProductRelated 21 37.1 38.6

## SpecialDay 17 29.3 30.9

## Informational 16 27.5 29.1

## MonthMar 15 26.2 27.8

## MonthDec 15 26.2 27.8

## TrafficType3 15 26.2 27.8

## TrafficType13 15 26.2 27.8

## Browser 11 19.6 21.1

## VisitorTypeOther 9 17.3 18.8

## VisitorTypeReturning_Visitor 8 15.8 17.3

## Administrative_Duration 7 14.1 15.5

## Administrative 5 10.6 11.9

## OperatingSystems2 2 4.5 5.8PageValues, BounceRates, ExitRates순으로 중요한 변수인 것으로 나타났다.

- test데이터에 모형이 얼마나 잘 작동하는지 보자.

test.earth.fit <- predict(earth.fit, newdata = test, type = 'class')

test.earth.fit <- as.factor(test.earth.fit)

earth.confusion <- confusionMatrix(test.earth.fit, test$Revenue, positive = 'TRUE')

earth.confusion

## Confusion Matrix and Statistics

##

## Reference

## Prediction FALSE TRUE

## FALSE 2425 134

## TRUE 701 438

##

## Accuracy : 0.7742

## 95% CI : (0.7604, 0.7876)

## No Information Rate : 0.8453

## P-Value [Acc > NIR] : 1

##

## Kappa : 0.3854

##

## Mcnemar's Test P-Value : <2e-16

##

## Sensitivity : 0.7657

## Specificity : 0.7758

## Pos Pred Value : 0.3845

## Neg Pred Value : 0.9476

## Prevalence : 0.1547

## Detection Rate : 0.1184

## Detection Prevalence : 0.3080

## Balanced Accuracy : 0.7707

##

## 'Positive' Class : TRUE

##

earth.confusion$byClass

## Sensitivity Specificity Pos Pred Value

## 0.7657343 0.7757518 0.3845478

## Neg Pred Value Precision Recall

## 0.9476358 0.3845478 0.7657343

## F1 Prevalence Detection Rate

## 0.5119813 0.1546782 0.1184424

## Detection Prevalence Balanced Accuracy

## 0.3080043 0.7707430MARS모형의 Accuracy는 0.713, Kappa는 0.318, F1-score는 0.468인 것으로 나타났다.

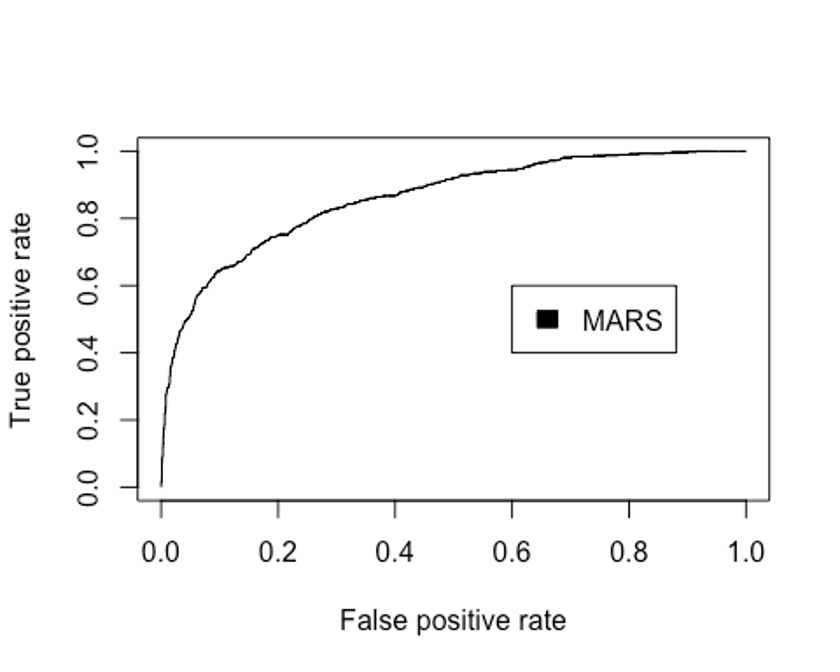

- ROC커브를 그려보자.

test.earth.pred <- predict(earth.fit, newdata = test, type = 'response')

pred.earth <- prediction(test.earth.pred, test$Revenue)

perf.earth <- performance(pred.earth, 'tpr', 'fpr')

plot(perf.earth, col = 1)

legend(0.6, 0.6, c('MARS'), 1)

- AUC를 확인해보자.

performance(pred.earth, 'auc')@y.values

## [[1]]

## [1] 0.8597294MARS모형의 Accuracy는 0.713, Kappa는 0.318, F1-score는 0.468, AUC는 0.860인 것으로 나타났다.

KNN

- K-최근접 이웃법을 이용해 모형을 만들어 보자.

– scaled_train_ROSE_dummy, scaled_test_dummy데이터를 사용한다.

– 먼저 필요한 패키지를 불러오자.

library(class)

library(kknn)

##

## Attaching package: 'kknn'

## The following object is masked from 'package:caret':

##

## contr.dummy

library(e1071)

##

## Attaching package: 'e1071'

## The following objects are masked from 'package:PerformanceAnalytics':

##

## kurtosis, skewness

library(kernlab)

##

## Attaching package: 'kernlab'

## The following object is masked from 'package:ggplot2':

##

## alpha

## The following object is masked from 'package:psych':

##

## alpha- KNN을 사용할 때는 적절한 k를 선택하는 것이 중요하다.

– expand.grid()와 seq()함수를 사용해 k를 선택해보자.

grid1 <- expand.grid(.k = seq(2, 30, by = 1))

control <- trainControl(method = 'cv')

set.seed(321)

knn.train <- train(Revenue ~., data = scaled_train_ROSE_dummy,

method = 'knn',

trControl = control,

tuneGrid = grid1)

knn.train

## k-Nearest Neighbors

##

## 8632 samples

## 63 predictor

## 2 classes: 'FALSE', 'TRUE'

##

## No pre-processing

## Resampling: Cross-Validated (10 fold)

## Summary of sample sizes: 7768, 7769, 7769, 7769, 7768, 7769, ...

## Resampling results across tuning parameters:

##

## k Accuracy Kappa

## 2 0.8111697 0.6227830

## 3 0.8138318 0.6282663

## 4 0.7924007 0.5854331

## 5 0.7857992 0.5723240

## 6 0.7670321 0.5347231

## 7 0.7635546 0.5278156

## 8 0.7526647 0.5060082

## 9 0.7511569 0.5030159

## 10 0.7473340 0.4953649

## 11 0.7453659 0.4914052

## 12 0.7376063 0.4759192

## 13 0.7379528 0.4765999

## 14 0.7322743 0.4652464

## 15 0.7328553 0.4663932

## 16 0.7284531 0.4575663

## 17 0.7276427 0.4558905

## 18 0.7226623 0.4459133

## 19 0.7262530 0.4531177

## 20 0.7254414 0.4514614

## 21 0.7219671 0.4444813

## 22 0.7197677 0.4401064

## 23 0.7190711 0.4386658

## 24 0.7165242 0.4335750

## 25 0.7157120 0.4319530

## 26 0.7157129 0.4319595

## 27 0.7127024 0.4259238

## 28 0.7094565 0.4194906

## 29 0.7106164 0.4217374

## 30 0.7107318 0.4219711

##

## Accuracy was used to select the optimal model using the largest value.

## The final value used for the model was k = 2.k매개변수 값으로 2가 나왔다.

- knn()함수를 이용해 모형을 만들어 보자.

knn.model <- knn(scaled_train_ROSE_dummy[, -64], scaled_test_dummy[, -64], scaled_train_ROSE_dummy[, 64], k = 2)

summary(knn.model)

## FALSE TRUE

## 2539 1159- scaled_test_dummy를 이용해 모형이 잘 작동하는지 보자.

knn.confusion <- confusionMatrix(knn.model, scaled_test_dummy$Revenue, positive = 'TRUE')

knn.confusion

## Confusion Matrix and Statistics

##

## Reference

## Prediction FALSE TRUE

## FALSE 2230 309

## TRUE 896 263

##

## Accuracy : 0.6741

## 95% CI : (0.6588, 0.6892)

## No Information Rate : 0.8453

## P-Value [Acc > NIR] : 1

##

## Kappa : 0.122

##

## Mcnemar's Test P-Value : <2e-16

##

## Sensitivity : 0.45979

## Specificity : 0.71337

## Pos Pred Value : 0.22692

## Neg Pred Value : 0.87830

## Prevalence : 0.15468

## Detection Rate : 0.07112

## Detection Prevalence : 0.31341

## Balanced Accuracy : 0.58658

##

## 'Positive' Class : TRUE

##

knn.confusion$byClass

## Sensitivity Specificity Pos Pred Value

## 0.45979021 0.71337172 0.22691976

## Neg Pred Value Precision Recall

## 0.87829854 0.22691976 0.45979021

## F1 Prevalence Detection Rate

## 0.30387060 0.15467820 0.07111952

## Detection Prevalence Balanced Accuracy

## 0.31341266 0.58658097Accuracy : 0.678, Kappa : 0.113, F1-score : 0.294의 성능이 나왔다.

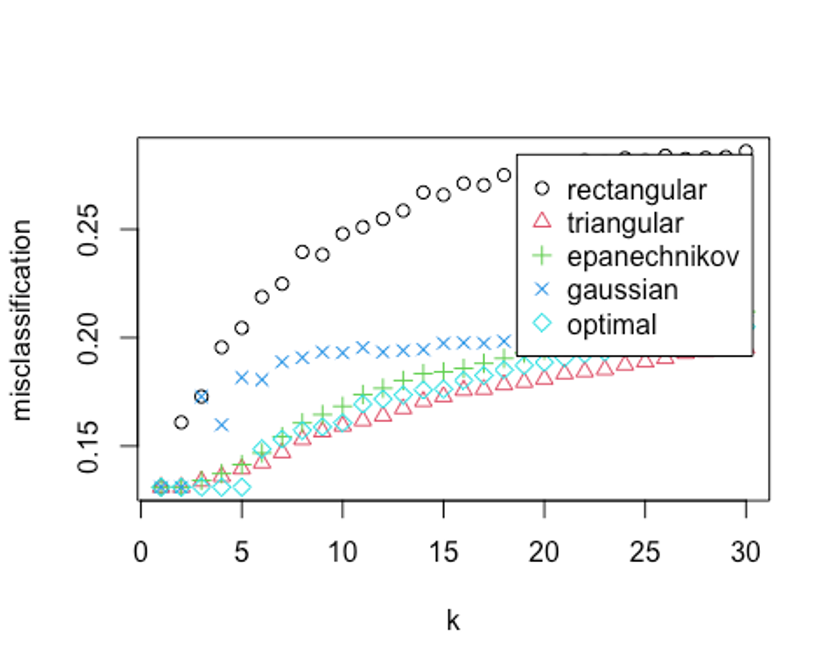

- 성능을 올리기 위해 커널을 입력하자.

– distance = 2를 이용해 절댓값합 거리를 사용하자.

kknn.train <- train.kknn(Revenue ~., data = scaled_train_ROSE_dummy, kmax = 30, distance = 2,

kernel = c('rectangular', 'triangular', 'epanechnikov', 'cosine', 'gaussian', 'optimal'))

plot(kknn.train)

- 자세한 값을 살펴보자.

kknn.train

##

## Call:

## train.kknn(formula = Revenue ~ ., data = scaled_train_ROSE_dummy, kmax = 30, distance = 2, kernel = c("rectangular", "triangular", "epanechnikov", "cosine", "gaussian", "optimal"))

##

## Type of response variable: nominal

## Minimal misclassification: 0.1310241

## Best kernel: rectangular

## Best k: 1k = 1, rectangular커널을 사용했을 때 약 13%의 오류가 나온 것으로 나타났다.

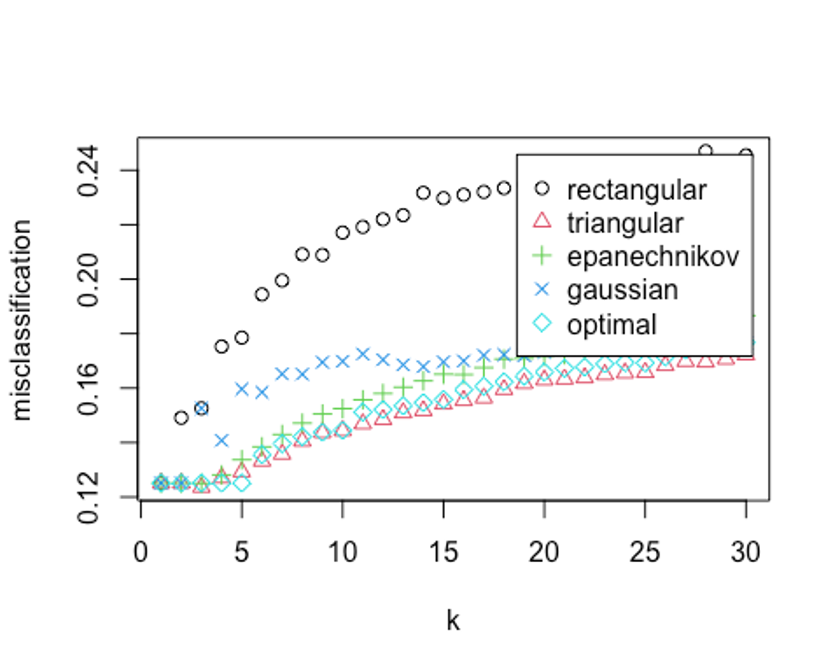

- distance = 1을 사용해 유클리드 거리로 다시 측정해보자.

kknn.train2 <- train.kknn(Revenue ~., data = scaled_train_ROSE_dummy, kmax = 30, distance = 1,

kernel = c('rectangular', 'triangular', 'epanechnikov', 'cosine', 'gaussian', 'optimal'))

plot(kknn.train2)

kknn.train2

##

## Call:

## train.kknn(formula = Revenue ~ ., data = scaled_train_ROSE_dummy, kmax = 30, distance = 1, kernel = c("rectangular", "triangular", "epanechnikov", "cosine", "gaussian", "optimal"))

##

## Type of response variable: nominal

## Minimal misclassification: 0.1236098

## Best kernel: triangular

## Best k: 3오류율이 더 떨어졌다. 최종 knn 하이퍼 파라미터로 유클리드 거리를 사용하고, k가 3, triangular커널을 사용하자.

- 예측 성능을 보자.

kknn.fit <- predict(kknn.train2, newdata = scaled_test_dummy)

kknn.fit <- as.factor(kknn.fit)

kknn.confusion <- confusionMatrix(kknn.fit, scaled_test_dummy$Revenue, positive = 'TRUE')

kknn.confusion

## Confusion Matrix and Statistics

##

## Reference

## Prediction FALSE TRUE

## FALSE 2315 314

## TRUE 811 258

##

## Accuracy : 0.6958

## 95% CI : (0.6807, 0.7106)

## No Information Rate : 0.8453

## P-Value [Acc > NIR] : 1

##

## Kappa : 0.1414

##

## Mcnemar's Test P-Value : <2e-16

##

## Sensitivity : 0.45105

## Specificity : 0.74056

## Pos Pred Value : 0.24135

## Neg Pred Value : 0.88056

## Prevalence : 0.15468

## Detection Rate : 0.06977

## Detection Prevalence : 0.28908

## Balanced Accuracy : 0.59581

##

## 'Positive' Class : TRUE

##

kknn.confusion$byClass

## Sensitivity Specificity Pos Pred Value

## 0.45104895 0.74056302 0.24134705

## Neg Pred Value Precision Recall

## 0.88056295 0.24134705 0.45104895

## F1 Prevalence Detection Rate

## 0.31444241 0.15467820 0.06976744

## Detection Prevalence Balanced Accuracy

## 0.28907518 0.59580599Accuracy : 0.690, Kappa : 0.121, F1-score : 0.298의 성능이 나왔다.

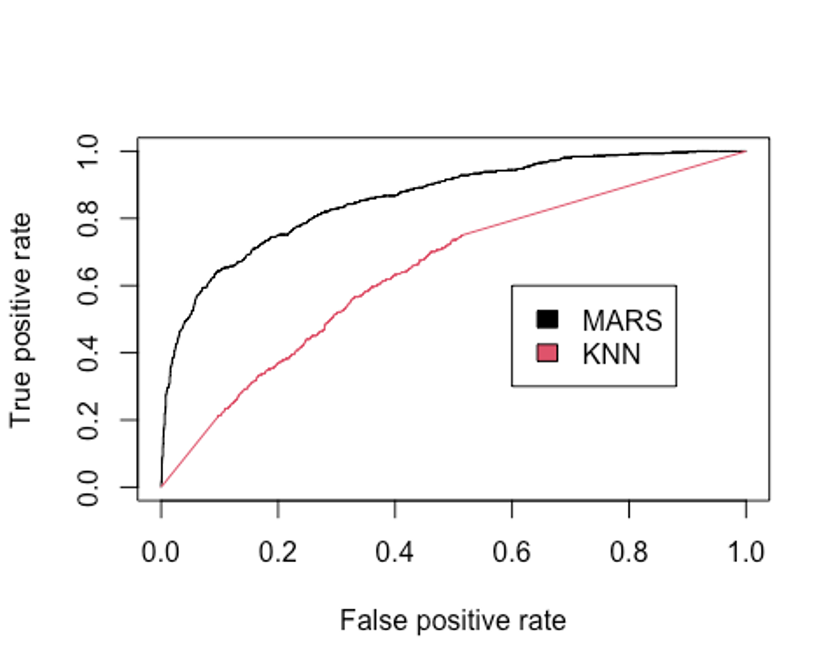

- ROC커브를 그려보자.

plot(perf.earth, col = 1)

knn.pred <- predict(kknn.train2, newdata = scaled_test_dummy, type = 'prob')

head(knn.pred)

## FALSE TRUE

## [1,] 1 0

## [2,] 1 0

## [3,] 1 0

## [4,] 1 0

## [5,] 1 0

## [6,] 1 0

knn.pred.true <- knn.pred[, 2]

pred.knn <- prediction(knn.pred.true, scaled_test_dummy$Revenue)

perf.knn <- performance(pred.knn, 'tpr', 'fpr')

plot(perf.knn, col = 2, add = TRUE)

legend(0.6, 0.6, c('MARS', 'KNN'), 1:2)

- AUC를 알아보자.

performance(pred.earth, 'auc')@y.values

## [[1]]

## [1] 0.8597294

performance(pred.knn, 'auc')@y.values

## [[1]]

## [1] 0.6454863KNN모형이 MARS모형보다 현저히 성능이 떨어지는 것으로 나타났다.

SVM

- 다음으로 SVM모형을 만들어 보자.

– scaled_train_ROSE, scaled_test를 사용한다.

– 선형 SVM모형부터 만들어보자.

– tune.svm()함수를 사용해 파라미터를 튜닝하고 커널 함수를 선택해 보자.

set.seed(321)

linear.tune <- tune.svm(Revenue ~., data = scaled_train_ROSE, kernel = 'linear',

cost = c(0.001, 0.01, 0.05, 0.1, 0.5, 1, 2, 5, 10))

summary(linear.tune)

##

## Parameter tuning of 'svm':

##

## - sampling method: 10-fold cross validation

##

## - best parameters:

## cost

## 0.5

##

## - best performance: 0.2438627

##

## - Detailed performance results:

## cost error dispersion

## 1 1e-03 0.2546346 0.01065937

## 2 1e-02 0.2445572 0.01319503

## 3 5e-02 0.2447894 0.01512409

## 4 1e-01 0.2445572 0.01444559

## 5 5e-01 0.2438627 0.01488985

## 6 1e+00 0.2442100 0.01432033

## 7 2e+00 0.2442101 0.01424995

## 8 5e+00 0.2445578 0.01443419

## 9 1e+01 0.2447893 0.01423905이 문제에서 최적의 cost함수는 0.5로 나왔고, 분류 오류 비율은 대략 24.3%이다.

- predict()함수로 scaled_test데이터 예측을 실행해보자.

best.linear <- linear.tune$best.model

tune.fit <- predict(best.linear, newdata = scaled_test, type = 'class')

tune.fit <- as.factor(tune.fit)

linear.svm.confusion <- confusionMatrix(tune.fit, scaled_test$Revenue, positive = 'TRUE')

linear.svm.confusion

## Confusion Matrix and Statistics

##

## Reference

## Prediction FALSE TRUE

## FALSE 3110 465

## TRUE 16 107

##

## Accuracy : 0.8699

## 95% CI : (0.8587, 0.8806)

## No Information Rate : 0.8453

## P-Value [Acc > NIR] : 1.301e-05

##

## Kappa : 0.2678

##

## Mcnemar's Test P-Value : < 2.2e-16

##

## Sensitivity : 0.18706

## Specificity : 0.99488

## Pos Pred Value : 0.86992

## Neg Pred Value : 0.86993

## Prevalence : 0.15468

## Detection Rate : 0.02893

## Detection Prevalence : 0.03326

## Balanced Accuracy : 0.59097

##

## 'Positive' Class : TRUE

##

linear.svm.confusion$byClass

## Sensitivity Specificity Pos Pred Value

## 0.18706294 0.99488164 0.86991870

## Neg Pred Value Precision Recall

## 0.86993007 0.86991870 0.18706294

## F1 Prevalence Detection Rate

## 0.30791367 0.15467820 0.02893456

## Detection Prevalence Balanced Accuracy

## 0.03326122 0.59097229Accuracy : 0.870, Kappa : 0.268, F1-score : 0.308의 성능이 나왔다.

- 비선형 방법을 이용해 성능을 더 높혀보자.

– 먼저 polynomial커널함수를 적용해보자.

– polynomial의 차수는 2, 3, 4, 5의 값을 주고, 커널 계수는 0.1부터 4의 값을 준다.

set.seed(321)

poly.tune <- tune.svm(Revenue ~., data = scaled_train_ROSE,

kernel = 'polynomial',

degree = c(2, 3, 4, 5),

coef0 = c(0.1, 0.5, 1, 2, 3, 4))

summary(poly.tune)

##

## Parameter tuning of 'svm':

##

## - sampling method: 10-fold cross validation

##

## - best parameters:

## degree coef0

## 5 3

##

## - best performance: 0.1244228

##

## - Detailed performance results:

## degree coef0 error dispersion

## 1 2 0.1 0.2136248 0.011477565

## 2 3 0.1 0.2238190 0.009216139

## 3 4 0.1 0.2569478 0.017482042

## 4 5 0.1 0.3772197 0.067941242

## 5 2 0.5 0.2151309 0.009976831

## 6 3 0.5 0.2025036 0.012627937

## 7 4 0.5 0.1974070 0.015111708

## 8 5 0.5 0.1961331 0.014705826

## 9 2 1.0 0.2167530 0.010793538

## 10 3 1.0 0.1921929 0.014408994

## 11 4 1.0 0.1719198 0.013520288

## 12 5 1.0 0.1539638 0.011488268

## 13 2 2.0 0.2183747 0.011273876

## 14 3 2.0 0.1784065 0.014240946

## 15 4 2.0 0.1452737 0.011683276

## 16 5 2.0 0.1292888 0.015147768

## 17 2 3.0 0.2176798 0.011264743

## 18 3 3.0 0.1726146 0.012825017

## 19 4 3.0 0.1384393 0.013437336

## 20 5 3.0 0.1244228 0.012136994

## 21 2 4.0 0.2176799 0.011201394

## 22 3 4.0 0.1672857 0.014499167

## 23 4 4.0 0.1363551 0.015486386

## 24 5 4.0 0.1275511 0.011526925이 모형은 다항식의 차수 degree의 값으로 5, 커널계수는 3을 선택했다.

- scaled_test데이터로 예측을 해보자.

best.poly <- poly.tune$best.model

poly.test <- predict(best.poly, newdata = scaled_test, type = 'class')

poly.test <- as.factor(poly.test)

poly.svm.confusion <- confusionMatrix(poly.test, scaled_test$Revenue, positive = 'TRUE')

poly.svm.confusion

## Confusion Matrix and Statistics

##

## Reference

## Prediction FALSE TRUE

## FALSE 1161 290

## TRUE 1965 282

##

## Accuracy : 0.3902

## 95% CI : (0.3744, 0.4061)

## No Information Rate : 0.8453

## P-Value [Acc > NIR] : 1

##

## Kappa : -0.0617

##

## Mcnemar's Test P-Value : <2e-16

##

## Sensitivity : 0.49301

## Specificity : 0.37140

## Pos Pred Value : 0.12550

## Neg Pred Value : 0.80014

## Prevalence : 0.15468

## Detection Rate : 0.07626

## Detection Prevalence : 0.60763

## Balanced Accuracy : 0.43220

##

## 'Positive' Class : TRUE

##

poly.svm.confusion$byClass

## Sensitivity Specificity Pos Pred Value

## 0.49300699 0.37140115 0.12550067

## Neg Pred Value Precision Recall

## 0.80013784 0.12550067 0.49300699

## F1 Prevalence Detection Rate

## 0.20007095 0.15467820 0.07625744

## Detection Prevalence Balanced Accuracy

## 0.60762574 0.43220407Accuracy : 0.390, Kappa : -0.062, F1-score : 0.200의 성능이 나왔다. 선형 SVM모델보다 성능이 떨어진다.

- 다음으로 방사 기저 함수를 커널로 설정해보자.

– 매개변수는 gamma로 최적값을 찾기위해 0.01부터 4까지 증가시켜 본다.

– gamma값이 너무 작을 때는 모형이 결정분계선을 제대로 포착하지 못할 수도 있고, 값이 너무 클 때는 모형이 지나치게 과적합될 수 있으므로 주의가 필요하다.

set.seed(321)

rbf.tune <- tune.svm(Revenue ~., data = scaled_train_ROSE,

kernel = 'radial',

gamma = c(0.01, 0.05, 0.1, 0.5, 1, 2, 3, 4))

summary(rbf.tune)

##

## Parameter tuning of 'svm':

##

## - sampling method: 10-fold cross validation

##

## - best parameters:

## gamma

## 0.1

##

## - best performance: 0.133227

##

## - Detailed performance results:

## gamma error dispersion

## 1 0.01 0.2209232 0.01139738

## 2 0.05 0.1594092 0.01383613

## 3 0.10 0.1332270 0.01325140

## 4 0.50 0.1342693 0.01149102

## 5 1.00 0.1789874 0.01099134

## 6 2.00 0.4136877 0.02304142

## 7 3.00 0.4829677 0.01365227

## 8 4.00 0.4904989 0.01121232최적의 gamma값은 0.1이다.

- 마찬가지로 성능을 예측해보자.

best.rbf <- rbf.tune$best.model

rbf.test <- predict(best.rbf, newdata = scaled_test, type = 'class')

rbf.test <- as.factor(rbf.test)

rbf.svm.confusion <- confusionMatrix(rbf.test, scaled_test$Revenue, positive = 'TRUE')

rbf.svm.confusion

## Confusion Matrix and Statistics

##

## Reference

## Prediction FALSE TRUE

## FALSE 122 57

## TRUE 3004 515

##

## Accuracy : 0.1723

## 95% CI : (0.1602, 0.1848)

## No Information Rate : 0.8453

## P-Value [Acc > NIR] : 1

##

## Kappa : -0.0195

##

## Mcnemar's Test P-Value : <2e-16

##

## Sensitivity : 0.90035

## Specificity : 0.03903

## Pos Pred Value : 0.14635

## Neg Pred Value : 0.68156

## Prevalence : 0.15468

## Detection Rate : 0.13926

## Detection Prevalence : 0.95160

## Balanced Accuracy : 0.46969

##

## 'Positive' Class : TRUE

##

rbf.svm.confusion$byClass

## Sensitivity Specificity Pos Pred Value

## 0.90034965 0.03902751 0.14634839

## Neg Pred Value Precision Recall

## 0.68156425 0.14634839 0.90034965

## F1 Prevalence Detection Rate

## 0.25177218 0.15467820 0.13926447

## Detection Prevalence Balanced Accuracy

## 0.95159546 0.46968858Accuracy : 0.172, Kappa : -0.195, F1-score : 0.252의 성능이 나왔다.

- 다시 성능 개선을 위해 sigmoid함수로 설정해보자.

– 매개변수인 gamma와 coef0이 최적의 값이 되도록 계산해보자.

set.seed(321)

sigmoid.tune <- tune.svm(Revenue ~., data = scaled_train_ROSE,

kernel = 'sigmoid',

gamma = c(0.1, 0.5, 1, 2, 3, 4),

coef0 = c(0.1, 0.5, 1, 2, 3, 4))

summary(sigmoid.tune)

##

## Parameter tuning of 'svm':

##

## - sampling method: 10-fold cross validation

##

## - best parameters:

## gamma coef0

## 0.1 4

##

## - best performance: 0.3468407

##

## - Detailed performance results:

## gamma coef0 error dispersion

## 1 0.1 0.1 0.3723386 0.01751505

## 2 0.5 0.1 0.4221501 0.01779125

## 3 1.0 0.1 0.4336186 0.01507837

## 4 2.0 0.1 0.4623463 0.03823503

## 5 3.0 0.1 0.4577106 0.03611425

## 6 4.0 0.1 0.4521562 0.02767209

## 7 0.1 0.5 0.4016492 0.02395204

## 8 0.5 0.5 0.4490297 0.01701384

## 9 1.0 0.5 0.4471733 0.01441787

## 10 2.0 0.5 0.4771777 0.04066548

## 11 3.0 0.5 0.4478606 0.02883916

## 12 4.0 0.5 0.4662848 0.03207388

## 13 0.1 1.0 0.4244720 0.02387098

## 14 0.5 1.0 0.4713884 0.02291624

## 15 1.0 1.0 0.4677966 0.01943992

## 16 2.0 1.0 0.4695354 0.03100309

## 17 3.0 1.0 0.4889955 0.04213662

## 18 4.0 1.0 0.4745028 0.04511312

## 19 0.1 2.0 0.4472937 0.01638526

## 20 0.5 2.0 0.4969898 0.02164017

## 21 1.0 2.0 0.4832031 0.02169763

## 22 2.0 2.0 0.4711563 0.01952145

## 23 3.0 2.0 0.4698815 0.02713059

## 24 4.0 2.0 0.5048693 0.02830511

## 25 0.1 3.0 0.4187918 0.01903577

## 26 0.5 3.0 0.5186545 0.02377845

## 27 1.0 3.0 0.5048649 0.01550109

## 28 2.0 3.0 0.4777603 0.02428690

## 29 3.0 3.0 0.4717361 0.01963229

## 30 4.0 3.0 0.5007038 0.02914465

## 31 0.1 4.0 0.3468407 0.03217296

## 32 0.5 4.0 0.5217822 0.01849434

## 33 1.0 4.0 0.5142523 0.02199626

## 34 2.0 4.0 0.4870263 0.02597384

## 35 3.0 4.0 0.4747484 0.02173184

## 36 4.0 4.0 0.4811119 0.03115664최적의 gamma값은 0.1이고, coef0값은 4이다.

- 예측을 해보자.

best.sigmoid <- sigmoid.tune$best.model

sigmoid.test <- predict(best.sigmoid, newdata = scaled_test, type = 'class')

sigmoid.test <- as.factor(sigmoid.test)

sigmoid.svm.confusion <- confusionMatrix(sigmoid.test, scaled_test$Revenue, positive = 'TRUE')

sigmoid.svm.confusion

## Confusion Matrix and Statistics

##

## Reference

## Prediction FALSE TRUE

## FALSE 3069 511

## TRUE 57 61

##

## Accuracy : 0.8464

## 95% CI : (0.8344, 0.8579)

## No Information Rate : 0.8453

## P-Value [Acc > NIR] : 0.4388

##

## Kappa : 0.1308

##

## Mcnemar's Test P-Value : <2e-16

##

## Sensitivity : 0.10664

## Specificity : 0.98177

## Pos Pred Value : 0.51695

## Neg Pred Value : 0.85726

## Prevalence : 0.15468

## Detection Rate : 0.01650

## Detection Prevalence : 0.03191

## Balanced Accuracy : 0.54420

##

## 'Positive' Class : TRUE

##

sigmoid.svm.confusion$byClass

## Sensitivity Specificity Pos Pred Value

## 0.10664336 0.98176583 0.51694915

## Neg Pred Value Precision Recall

## 0.85726257 0.51694915 0.10664336

## F1 Prevalence Detection Rate

## 0.17681159 0.15467820 0.01649540

## Detection Prevalence Balanced Accuracy

## 0.03190914 0.54420460Accuracy : 0.846, Kappa : 0.131, F1-score : 0.177의 성능이 나왔다.

- 가장 좋은 성능을 보인 sigmoid 함수를 사용한 SVM의 ROC그래프를 그려보자.

set.seed(321)

sigmoid.model <- svm(Revenue ~., data = scaled_train_ROSE, kernel = 'sigmoid', gamma = 0.1, coef0 = 0.1, scale = FALSE, probability = TRUE)

pred_svm <- predict(sigmoid.model, scaled_test, probability = TRUE)

prob <- attr(pred_svm, 'probabilities')

head(prob)

## FALSE TRUE

## 4 0.9718696 0.02813039

## 5 0.8936604 0.10633958

## 9 0.9026196 0.09738039

## 10 0.7246909 0.27530908

## 13 0.8644836 0.13551642

## 17 0.9846849 0.01531511

pred.svm <- prediction(prob[, 2], scaled_test$Revenue)

perf.svm <- performance(pred.svm, 'tpr', 'fpr')

plot(perf.earth, col = 1)

plot(perf.knn, col = 2, add = TRUE)

plot(perf.svm, col = 3, add = TRUE)

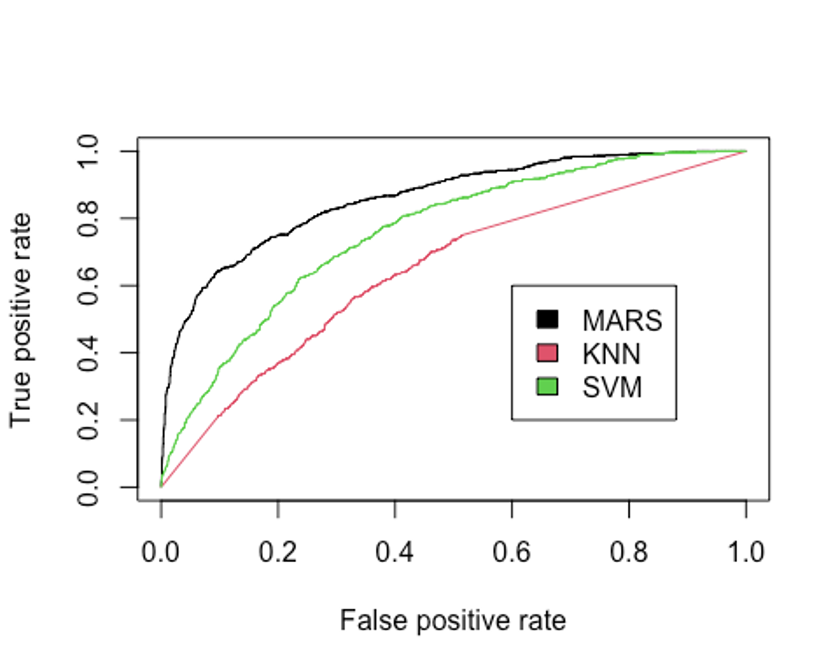

legend(0.6, 0.6, c('MARS', 'KNN', 'SVM'), 1:3)

- AUC를 알아보자.

performance(pred.earth, 'auc')@y.values

## [[1]]

## [1] 0.8597294

performance(pred.knn, 'auc')@y.values

## [[1]]

## [1] 0.6454863

performance(pred.svm, 'auc')@y.values

## [[1]]

## [1] 0.7590371AUC를 보면 MARS, SVM, KNN모형 순으로 성능이 좋다.

Random Forest

- 랜덤포레스트 모델을 만들자.

– train, test데이터를 사용해보자.

– 필요한 패키지를 불러오자.

library(rpart)

library(partykit)

## Loading required package: grid

## Loading required package: libcoin

## Loading required package: mvtnorm

library(genridge)

##

## Attaching package: 'genridge'

## The following object is masked from 'package:bestglm':

##

## Detroit

## The following object is masked from 'package:caret':

##

## precision

library(randomForest)

## randomForest 4.7-1

## Type rfNews() to see new features/changes/bug fixes.

##

## Attaching package: 'randomForest'

## The following object is masked from 'package:dplyr':

##

## combine

## The following object is masked from 'package:gridExtra':

##

## combine

## The following object is masked from 'package:ggplot2':

##

## margin

## The following object is masked from 'package:psych':

##

## outlier

library(xgboost)

##

## Attaching package: 'xgboost'

## The following object is masked from 'package:dplyr':

##

## slice- 기본 모형을 만들어 보자.

set.seed(321)

rf.model <- randomForest(Revenue ~., data = train)

rf.model

##

## Call:

## randomForest(formula = Revenue ~ ., data = train)

## Type of random forest: classification

## Number of trees: 500

## No. of variables tried at each split: 4

##

## OOB estimate of error rate: 9.68%

## Confusion matrix:

## FALSE TRUE class.error

## FALSE 6999 297 0.04070724

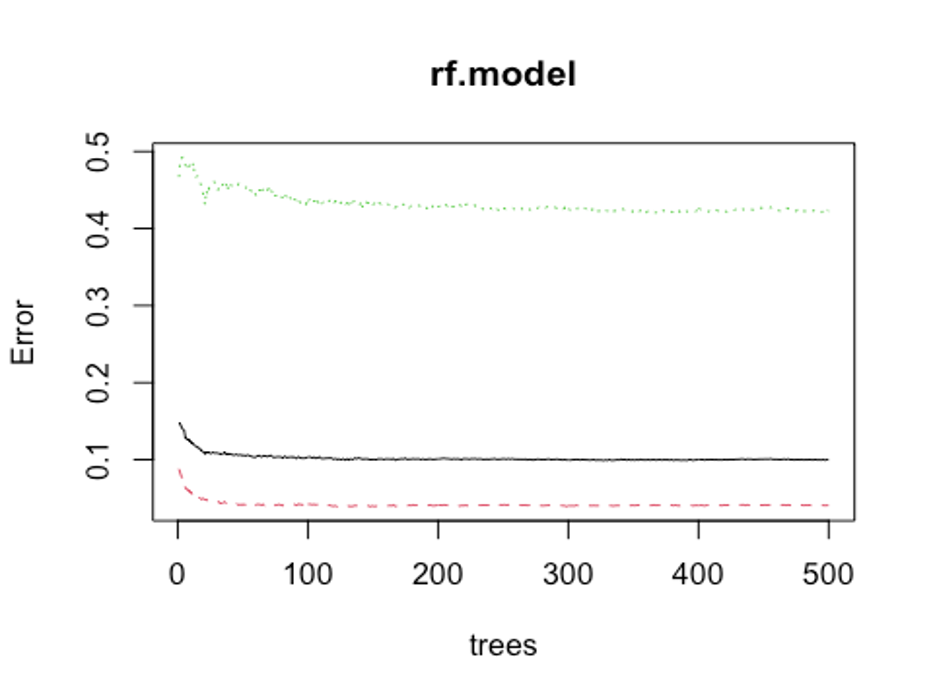

## TRUE 565 771 0.42290419수행 결과 OOB오차율이 9.68%로 나왔다.

- 개선을 위해 최적의 트리 수를 보자.

plot(rf.model)

which.min(rf.model$err.rate[, 1])

## [1] 320모형 정확도를 최적화 하기에 필요한 트리 수가 320개면 된다는 결과를 얻었다.

- 다시 모형을 만들어 보자.

set.seed(321)

rf.model2 <- randomForest(Revenue ~., data = train, ntree = 320)

rf.model2

##

## Call:

## randomForest(formula = Revenue ~ ., data = train, ntree = 320)

## Type of random forest: classification

## Number of trees: 320

## No. of variables tried at each split: 4

##

## OOB estimate of error rate: 9.59%

## Confusion matrix:

## FALSE TRUE class.error

## FALSE 7001 295 0.04043311

## TRUE 567 769 0.42440120OOB오차율이 9.68%에서 9.59%로 약간 떨어졌다.

- test데이터로 어떤 결과가 나오는지 보자.

rf.fit <- predict(rf.model2, newdata = test, type = 'class')

rf.fit <- as.factor(rf.fit)

rf.confusion <- confusionMatrix(rf.fit, test$Revenue, positive = 'TRUE')

rf.confusion

## Confusion Matrix and Statistics

##

## Reference

## Prediction FALSE TRUE

## FALSE 3012 222

## TRUE 114 350

##

## Accuracy : 0.907

## 95% CI : (0.8994, 0.9182)

## No Information Rate : 0.8453

## P-Value [Acc > NIR] : < 2.2e-16

##

## Kappa : 0.6179

##

## Mcnemar's Test P-Value : 5.304e-09

##

## Sensitivity : 0.61189

## Specificity : 0.96353

## Pos Pred Value : 0.75431

## Neg Pred Value : 0.93135

## Prevalence : 0.15468

## Detection Rate : 0.09465

## Detection Prevalence : 0.12547

## Balanced Accuracy : 0.78771

##

## 'Positive' Class : TRUE

##

rf.confusion$byClass

## Sensitivity Specificity Pos Pred Value

## 0.61188811 0.96353167 0.75431034

## Neg Pred Value Precision Recall

## 0.93135436 0.75431034 0.61188811

## F1 Prevalence Detection Rate

## 0.67207568 0.15467820 0.09464575

## Detection Prevalence Balanced Accuracy

## 0.12547323 0.78770989Accuracy : 0.907, Kappa : 0.618, F1-score : 0.672의 성능이 나왔다.

하이퍼 파마미터 조정 없이도 지금까지 만든 모형 중 최고의 성능을 보이고 있다.

- 성능을 좀 더 높여보자.

rf_mtry <- seq(4, ncol(train)*0.8, by = 2)

rf_nodesize <- seq(3, 8, by = 1)

rf_sample_size <- nrow(train) * c(0.7, 0.8)

rf_hyper_grid <- expand.grid(mtry = rf_mtry,

nodesize = rf_nodesize,

samplesize = rf_sample_size)- 설정된 파라미터를 바탕으로 모형을 적합한다.

rf_oob_err <- c()

for(i in 1:nrow(rf_hyper_grid)) {

model <- randomForest(Revenue ~., data = train,

mtry = rf_hyper_grid$mtry[i],

nodesize = rf_hyper_grid$nodesize[i],

samplesize = rf_hyper_grid$samplesize[i])

rf_oob_err[i] <- model$err.rate[nrow(model$err.rate), 'OOB']

}- 최적의 하이퍼 파라미터를 보자.

rf_hyper_grid[which.min(rf_oob_err), ]

## mtry nodesize samplesize

## 55 4 7 6905.6- 위의 파라미터를 토대로 모형을 만들자.

rf_best_model <- randomForest(Revenue ~., data = train,

mtry = 4,

nodesize = 7,

samplesize = 6905.6,

proximity = TRUE,

importance = TRUE)- predict()함수로 예측을 해보자.

rf.predict <- predict(rf_best_model, newdata = test, type = 'class')

rf.predict <- as.factor(rf.predict)

rf.best.confusion <- confusionMatrix(rf.predict, test$Revenue, positive = 'TRUE')

rf.best.confusion

## Confusion Matrix and Statistics

##

## Reference

## Prediction FALSE TRUE

## FALSE 3020 226

## TRUE 106 346

##

## Accuracy : 0.9102

## 95% CI : (0.9005, 0.9192)

## No Information Rate : 0.8453

## P-Value [Acc > NIR] : < 2.2e-16

##

## Kappa : 0.6245

##

## Mcnemar's Test P-Value : 6.534e-11

##

## Sensitivity : 0.60490

## Specificity : 0.96609

## Pos Pred Value : 0.76549

## Neg Pred Value : 0.93038

## Prevalence : 0.15468

## Detection Rate : 0.09356

## Detection Prevalence : 0.12223

## Balanced Accuracy : 0.78549

##

## 'Positive' Class : TRUE

##

rf.best.confusion$byClass

## Sensitivity Specificity Pos Pred Value

## 0.60489510 0.96609085 0.76548673

## Neg Pred Value Precision Recall

## 0.93037585 0.76548673 0.60489510

## F1 Prevalence Detection Rate

## 0.67578125 0.15467820 0.09356409

## Detection Prevalence Balanced Accuracy

## 0.12222823 0.78549298Accuracy : 0.910, Kappa : 0.625, F1-score : 0.676의 성능이 나왔다. F1-score를 성능 평가의 기준으로 본다면 기본 랜덤 포레스트 모델보다 성능이 약간 더 올라갔다.

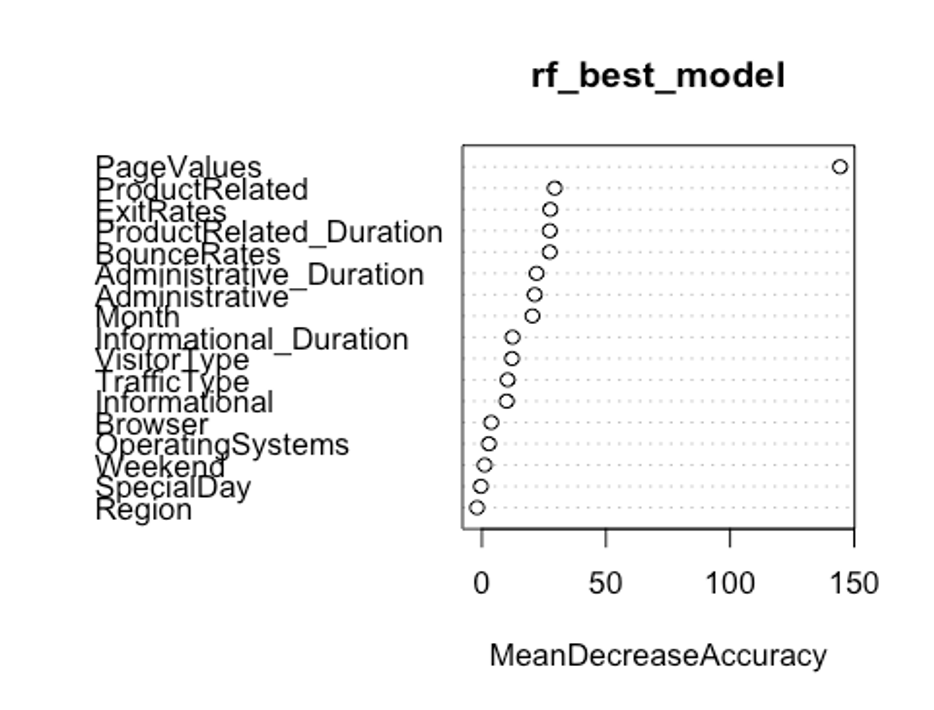

- 변수 중요도를 보자.

varImpPlot(rf_best_model, type = 1)

PageValues, ExitRates, ProductRelated, BounceRates순으로 중요한 변수인 것으로 나타났다.

- type를 바꿔서 변수 중요도를 보자.

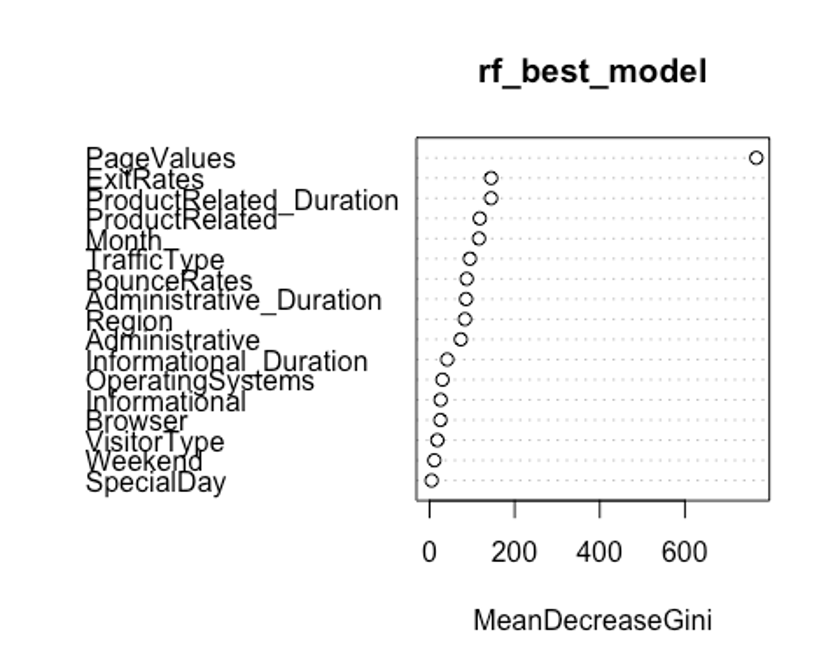

varImpPlot(rf_best_model, type = 2)

여기서는 PageValues, ExitRates, ProductRelated_Duration, Month순으로 중요한 변수인 것으로 나타났다.

첫번째 plot을 보자. 변수의 값을 랜덤하게 섞었다면, 모델의 정확도가 감소하는 정도를 측정한다.(type = 1)

변수를 랜덤하게 섞는다는 것은 해당 변수가 예측에 미치는 모든 영향력을 제거하는 것을 의미한다. 정확도는 OOB데이터로부터 얻는다. 이는 결국 교차 타당성과 같은 효과를 얻는다.

두번째 plot을 보자. 특정 변수를 기준으로 분할이 일어난 모든 노드에서 불순도 점수의 평균 감소량을 측정한다.(type = 2)

이 지표는 해당 변수가 노드의 불순도를 개선하는데 얼마나 기여했는지를 나타낸다.

그러나 이 지표는 학습데이터를 기반으로 측정되기 때문에 OOB데이터를 가지고 계산한 것에 비해 믿을 만하지 않다.

우리의 plot에서 첫번째와 두번째 plot의 변수 중요도 순서가 다소 다른 것을 볼 수 있는데, OOB데이터로부터 정확도 감소량을 측정한 첫번째 plot이 더 믿을 만하다.

- 랜덤포레스트 모형의 ROC그래프를 그려보자.

rf.pred <- predict(rf_best_model, newdata = test, type = 'prob')

head(rf.pred)

## FALSE TRUE

## 4 0.998 0.002

## 5 1.000 0.000

## 9 1.000 0.000

## 10 0.980 0.020

## 13 1.000 0.000

## 17 1.000 0.000

rf.pred.true <- rf.pred[, 2]

pred.rf <- prediction(rf.pred.true, test$Revenue)

perf.rf <- performance(pred.rf, 'tpr', 'fpr')

plot(perf.earth, col = 1)

plot(perf.knn, col = 2, add = TRUE)

plot(perf.svm, col = 3, add = TRUE)

plot(perf.rf, col = 4, add = TRUE)

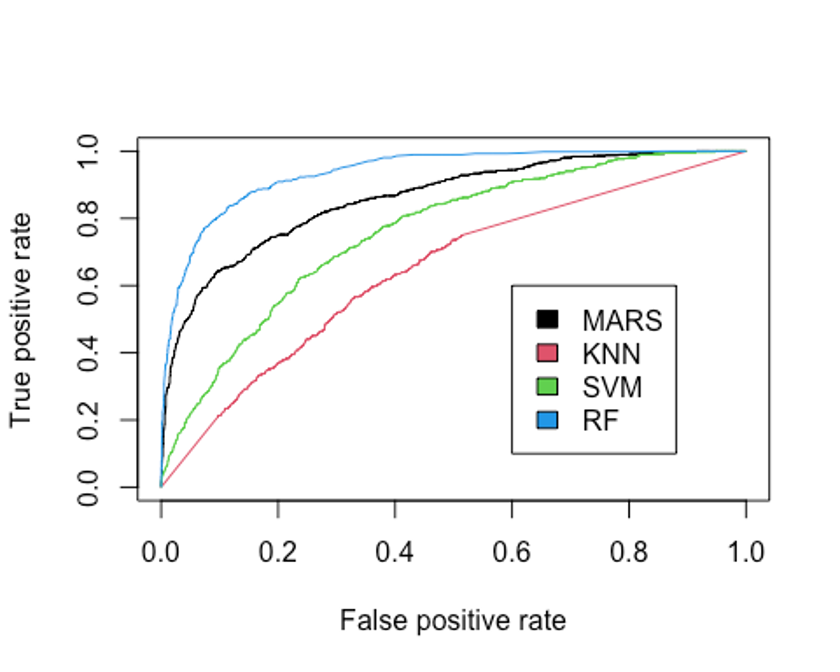

legend(0.6, 0.6, c('MARS', 'KNN', 'SVM', 'RF'), 1:4)

- AUC를 보자.

performance(pred.earth, 'auc')@y.values

## [[1]]

## [1] 0.8597294

performance(pred.knn, 'auc')@y.values

## [[1]]

## [1] 0.6454863

performance(pred.svm, 'auc')@y.values

## [[1]]

## [1] 0.7590371

performance(pred.rf, 'auc')@y.values

## [[1]]

## [1] 0.9365532랜덤포레스트 모형의 AUC는 0.937, F1-score는 0.676으로 지금까지 만든 모형 중 가장 좋은 성능을 보인다.

XGBoost

- XGBoost모형을 만들어보자.

– scaled_train_ROSE_dummy, scaled_test_dummy데이터를 사용한다.

– 그리드를 만들어 보자.

grid <- expand.grid(nrounds = seq(50, 200, by = 25),

colsample_bytree = 1,

min_child_weight = 1,

eta = c(0.01, 0.1, 0.3),

gamma = c(0.5, 0.25, 0.1),

subsample = 0.5,

max_depth = c(1, 2, 3))- trainControl인자를 조정한다. 여기서는 10-fold교차검증을 사용해보자.

cntrl <- trainControl(method = 'cv',

number = 10,

verboseIter = TRUE,

returnData = FALSE,

returnResamp = 'final')- train()함수를 이용해 데이터를 학습시킨다.

set.seed(321)

train.xgb <- train(x = scaled_train_ROSE_dummy[, 1:63],

y = scaled_train_ROSE_dummy[, 64],

trControl = cntrl,

tuneGrid = grid,

method = 'xgbTree')

## + Fold01: eta=0.01, max_depth=1, gamma=0.10, colsample_bytree=1, min_child_weight=1, subsample=0.5, nrounds=200

...[생략]...

## - Fold10: eta=0.30, max_depth=3, gamma=0.50, colsample_bytree=1, min_child_weight=1, subsample=0.5, nrounds=200

## Aggregating results

## Selecting tuning parameters

## Fitting nrounds = 200, max_depth = 2, eta = 0.3, gamma = 0.1, colsample_bytree = 1, min_child_weight = 1, subsample = 0.5 on full training set모형을 생성하기 위한 최적 인자들의 조합이 출력되었다.

- xgb.train()에서 사용할 인자 목록을 생성하고, 데이터 프레임과 입력피처의 행렬과 숫자 레이블을 붙힌 결과 목록으로 변환한다. 그런 다음, 피처와 식별값을 xgb.DMatrix에서 사용할 입력값으로 변환한다.

param <- list(objective = 'binary:logistic',

booster = 'gbtree',

eval_metric = 'error',

eta = 0.1,

max_depth = 3,

subsample = 0.5,

colsample_bytree = 1,

gamma = 0.25)

x <- as.matrix(scaled_train_ROSE_dummy[, 1:63])

y <- ifelse(scaled_train_ROSE_dummy$Revenue == 'TRUE', 1, 0)

train.mat <- xgb.DMatrix(data = x, label = y)- 이제 모형을 만들어 보자.

set.seed(321)

xgb.fit <- xgb.train(params = param, data = train.mat, nrounds = 200)- 테스트 세트에 관한 결과를 보기 전에 변수 중요도를 그려 검토해보자.

– 항목은 gain, cover, frequency이렇게 세가지를 검사할 수 있다.

– gain은 피처가 트리에 미치는 정확도의 향상 정도를 나타내는 값, cover는 이 피처와 연관된 전체 관찰값의 상대 수치, frequency는 모든 트리에 관해 피처가 나타난 횟수를 백분율로 나타낸 값이다.

impMatrix <- xgb.importance(feature_names = dimnames(x)[[2]], model = xgb.fit)

impMatrix

## Feature Gain Cover Frequency

## 1: PageValues 0.4784240125 1.869656e-01 0.1305361305

## 2: BounceRates 0.1727421906 1.656120e-01 0.1507381507

## 3: ExitRates 0.0971338718 1.277573e-01 0.1181041181

## 4: Informational_Duration 0.0348257955 6.528953e-02 0.0769230769

## 5: ProductRelated 0.0309641404 5.490478e-02 0.0582750583

## 6: SpecialDay 0.0295982800 6.593116e-02 0.0675990676

## 7: Administrative_Duration 0.0280666341 5.798735e-02 0.0745920746

## 8: ProductRelated_Duration 0.0250421770 4.861642e-02 0.0543900544

## 9: Informational 0.0224339615 4.806354e-02 0.0574980575

## 10: Browser 0.0172514589 4.705973e-02 0.0505050505

## 11: Month.Nov 0.0168688132 1.935782e-02 0.0108780109

## 12: Administrative 0.0143997535 3.341250e-02 0.0458430458

## 13: Month.Mar 0.0039715597 1.218894e-02 0.0108780109

## 14: Month.Dec 0.0033040929 9.343259e-03 0.0077700078

## 15: OperatingSystems.3 0.0028385066 3.381270e-03 0.0062160062

## 16: TrafficType.20 0.0023210578 4.025680e-03 0.0054390054

## 17: Month.Jul 0.0021296866 7.617290e-03 0.0062160062

## 18: TrafficType.13 0.0018176052 7.297333e-03 0.0062160062

## 19: VisitorType.New_Visitor 0.0015648864 2.219472e-03 0.0046620047

## 20: OperatingSystems.2 0.0015277417 1.083584e-03 0.0046620047

## 21: TrafficType.3 0.0013789892 3.162833e-03 0.0054390054

## 22: Month.May 0.0011153780 7.819642e-04 0.0054390054

## 23: Month.Oct 0.0010995887 3.329312e-03 0.0023310023

## 24: VisitorType.Returning_Visitor 0.0010903772 9.601673e-04 0.0038850039

## 25: TrafficType.1 0.0010818693 9.101117e-04 0.0038850039

## 26: Month.Sep 0.0007981466 3.477941e-03 0.0038850039

## 27: TrafficType.11 0.0007492348 3.699442e-03 0.0023310023

## 28: Region.5 0.0007079333 3.789249e-03 0.0031080031

## 29: TrafficType.8 0.0006311398 3.683572e-03 0.0023310023

## 30: Region.8 0.0006180287 7.662673e-04 0.0023310023

## 31: Region.2 0.0005618941 1.360264e-03 0.0023310023

## 32: TrafficType.4 0.0005498389 5.493061e-04 0.0023310023

## 33: Weekend.FALSE 0.0004772906 1.266921e-03 0.0023310023

## 34: Region.1 0.0004571332 1.371042e-03 0.0023310023

## 35: OperatingSystems.1 0.0003640132 2.657992e-04 0.0015540016

## 36: Region.3 0.0003319009 1.319690e-04 0.0015540016

## 37: TrafficType.2 0.0002404024 8.414712e-05 0.0023310023

## 38: Month.Aug 0.0002016128 1.181909e-03 0.0007770008

## 39: Region.9 0.0001671186 1.063640e-03 0.0007770008

## 40: Region.7 0.0001518840 4.954983e-05 0.0007770008

## Feature Gain Cover Frequency

xgb.plot.importance(impMatrix, main = 'Gain by Feature')BounceRates, Informational_Duration, SpecialDay순으로 중요한 변수인 것으로 나타났다.

- 다음으로 scaled_test_dummy데이터에 관한 수행 결과를 보자.

library(InformationValue)

##

## Attaching package: 'InformationValue'

## The following object is masked from 'package:genridge':

##

## precision

## The following objects are masked from 'package:caret':

##

## confusionMatrix, precision, sensitivity, specificity

pred <- predict(xgb.fit, x)

optimalCutoff(y, pred)

## [1] 0.4397303

testMat <- as.matrix(scaled_test_dummy[, 1:63])

y.test <- ifelse(scaled_test_dummy$Revenue == 'TRUE', 1, 0)

xgb.test <- predict(xgb.fit, testMat)

confusionMatrix(y.test, xgb.test, threshold = 0.4697492)

## 0 1

## 0 298 104

## 1 2930 468

1 - misClassError(y.test, xgb.test, threshold = 0.4697492)

## [1] 0.1796약 17.96%의 정확도를 보였다.

- F1-score를 계산해보자.

precision <- 468 / (104 + 468)

recall <- 468 / (2930 + 468)

f1 <- (2*precision*recall) / (precision + recall)

f1

## [1] 0.2357683F1-score는 0.236이다.

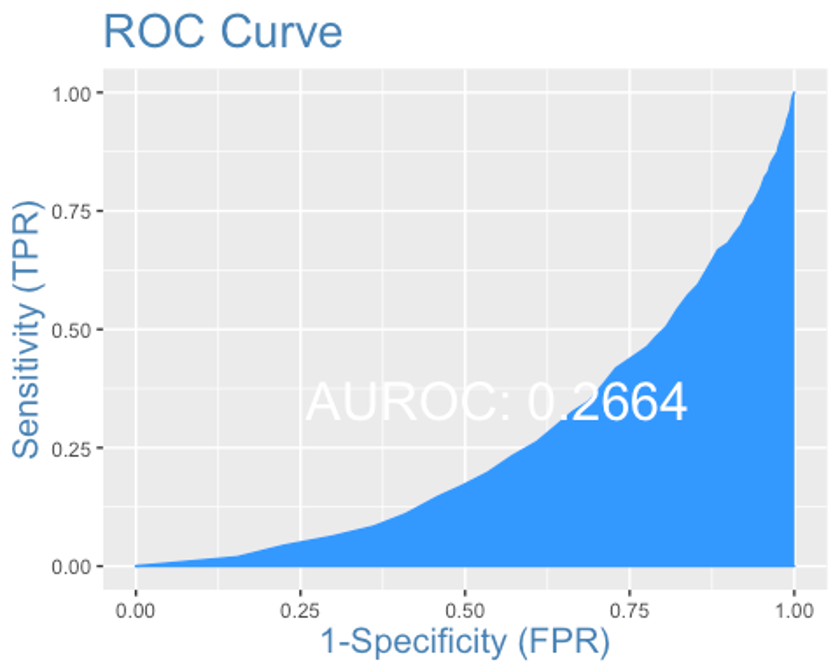

- ROC커브를 그려보자.

plotROC(y.test, xgb.test)

AUC는 0.266로 형편없는 성능이 나왔다.

앙상블

- 앙상블 분석을 해보자.

– 데이터는 scaled_train_ROSE, scaled_test데이터를 사용하자.

– 먼저 필요한 패키지들을 불러오자.

library(caretEnsemble)

##

## Attaching package: 'caretEnsemble'

## The following object is masked from 'package:ggplot2':

##

## autoplot

library(caTools)

library(mlr)

## Loading required package: ParamHelpers

## Warning message: 'mlr' is in 'maintenance-only' mode since July 2019.

## Future development will only happen in 'mlr3'

## (<https://mlr3.mlr-org.com>). Due to the focus on 'mlr3' there might be

## uncaught bugs meanwhile in {mlr} - please consider switching.

##

## Attaching package: 'mlr'

## The following object is masked _by_ '.GlobalEnv':

##

## f1

## The following object is masked from 'package:e1071':

##

## impute

## The following object is masked from 'package:ROCR':

##

## performance

## The following object is masked from 'package:caret':

##

## train

library(HDclassif)

library(gbm)

## Loaded gbm 2.1.8

library(mboost)

## Loading required package: parallel

## Loading required package: stabs

##

## Attaching package: 'stabs'

## The following object is masked from 'package:mlr':

##

## subsample

##

## Attaching package: 'mboost'

## The following object is masked from 'package:partykit':

##

## varimp

## The following object is masked from 'package:ggplot2':

##

## %+%

## The following objects are masked from 'package:psych':

##

## %+%, AUC

## The following object is masked from 'package:pastecs':

##

## extract- 10-fold 교차검증을 사용하자.

control <- trainControl(method = 'cv', number = 10,

savePredictions = 'final',

classProbs = TRUE,

summaryFunction = twoClassSummary)- 모형을 학습시키자. rpart, MARS, knn을 사용해 보자.

set.seed(321)

levels(scaled_train_ROSE$Revenue)[levels(scaled_train_ROSE$Revenue) == 'TRUE'] <- 'Yes'

levels(scaled_train_ROSE$Revenue)[levels(scaled_train_ROSE$Revenue) == 'FALSE'] <- 'No'

levels(scaled_test$Revenue)[levels(scaled_test$Revenue) == 'TRUE'] <- 'Yes'

levels(scaled_test$Revenue)[levels(scaled_test$Revenue) == 'FALSE'] <- 'No'

Models <- caretList(Revenue ~., data = scaled_train_ROSE,

trControl = control,

metric = 'ROC',

methodList = c('rpart', 'earth', 'knn'))

Models

## $rpart

## CART

##

## 8632 samples

## 17 predictor

## 2 classes: 'No', 'Yes'

##

## No pre-processing

## Resampling: Cross-Validated (10 fold)

## Summary of sample sizes: 7768, 7768, 7770, 7769, 7768, 7769, ...

## Resampling results across tuning parameters:

##

## cp ROC Sens Spec

## 0.01593999 0.8319226 0.9232685 0.7372222

## 0.11298640 0.8108015 0.9221244 0.6977845

## 0.54688233 0.5758940 0.9791589 0.1726292

##

## ROC was used to select the optimal model using the largest value.

## The final value used for the model was cp = 0.01593999.

##

## $earth

## Multivariate Adaptive Regression Spline

##

## 8632 samples

## 17 predictor

## 2 classes: 'No', 'Yes'

##

## No pre-processing

## Resampling: Cross-Validated (10 fold)

## Summary of sample sizes: 7768, 7768, 7770, 7769, 7768, 7769, ...

## Resampling results across tuning parameters:

##

## nprune ROC Sens Spec

## 2 0.7503215 0.9216641 0.6258612

## 14 0.9497227 0.8879915 0.8600587

## 27 0.9573285 0.8939501 0.8776347

##

## Tuning parameter 'degree' was held constant at a value of 1

## ROC was used to select the optimal model using the largest value.

## The final values used for the model were nprune = 27 and degree = 1.

##

## $knn

## k-Nearest Neighbors

##

## 8632 samples

## 17 predictor

## 2 classes: 'No', 'Yes'

##

## No pre-processing

## Resampling: Cross-Validated (10 fold)

## Summary of sample sizes: 7768, 7768, 7770, 7769, 7768, 7769, ...

## Resampling results across tuning parameters:

##

## k ROC Sens Spec

## 5 0.8472500 0.6852954 0.8347429

## 7 0.8248064 0.6788734 0.8124727

## 9 0.8100880 0.6745229 0.7932601

##

## ROC was used to select the optimal model using the largest value.

## The final value used for the model was k = 5.

##

## attr(,"class")

## [1] "caretList"scaled_train_ROSE의 Revenue변수의 levels 이름이 TRUE와 FALSE면 오류가 나서 이름을 Yes와 No로 바꿔줬다.

- 데이터 프레임 안의 테스트 세트에서 ’Yes’에 관한 예측값을 얻어오자.

model_preds <- lapply(Models, predict, newdata = scaled_test, type = 'prob')

model_preds <- lapply(model_preds, function(x) x[, 'Yes'])

model_preds <- data.frame(model_preds)- stack으로 로지스틱 회귀 모형을 쌓아보자.

stack <- caretStack(Models, method = 'glm', metric = 'ROC',

trControl = trainControl(

method = 'boot', number = 10,

savePredictions = 'final',

classProbs = TRUE,

summaryFunction = twoClassSummary

))

summary(stack)

##

## Call:

## NULL

##

## Deviance Residuals:

## Min 1Q Median 3Q Max

## -3.0708 -0.2660 -0.1108 0.2792 2.9108

##

## Coefficients:

## Estimate Std. Error z value Pr(>|z|)

## (Intercept) 4.8122 0.1170 41.130 < 2e-16 ***

## rpart -0.6179 0.1676 -3.688 0.000226 ***

## earth -5.5790 0.1614 -34.556 < 2e-16 ***

## knn -3.8415 0.1482 -25.924 < 2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## (Dispersion parameter for binomial family taken to be 1)

##

## Null deviance: 11965.3 on 8631 degrees of freedom

## Residual deviance: 3983.7 on 8628 degrees of freedom

## AIC: 3991.7

##

## Number of Fisher Scoring iterations: 6모형의 계수가 모두 유의하다.

- 앙상블에 사용된 학습자의 각 예측 결과를 비교해보자.

prob <- 1 - predict(stack, newdata = scaled_test, type = 'prob')

model_preds$ensemble <- prob

colAUC(model_preds, scaled_test$Revenue)

## rpart earth knn ensemble

## No vs. Yes 0.6463632 0.7198927 0.6373395 0.539174각 모형의 AUC를 봤을 때 앙상블 모형이 오히려 단독 모형들보다 성능이 떨어진다.

- 앙상블 모형으로 confusion matrix를 만들어 보자.

class <- predict(stack, newdata = scaled_test, type = 'raw')

head(class)

## [1] Yes Yes Yes Yes Yes Yes

## Levels: No Yes

detach('package:InformationValue', unload = TRUE)

ensemble.confusion <- confusionMatrix(class, scaled_test$Revenue, positive = 'Yes')

ensemble.confusion

## Confusion Matrix and Statistics

##

## Reference

## Prediction No Yes

## No 168 75

## Yes 2958 497

##

## Accuracy : 0.1798

## 95% CI : (0.1676, 0.1926)

## No Information Rate : 0.8453

## P-Value [Acc > NIR] : 1

##

## Kappa : -0.0253

##

## Mcnemar's Test P-Value : <2e-16

##

## Sensitivity : 0.86888

## Specificity : 0.05374

## Pos Pred Value : 0.14385

## Neg Pred Value : 0.69136

## Prevalence : 0.15468

## Detection Rate : 0.13440

## Detection Prevalence : 0.93429

## Balanced Accuracy : 0.46131

##

## 'Positive' Class : Yes

##

ensemble.confusion$byClass

## Sensitivity Specificity Pos Pred Value

## 0.8688811 0.0537428 0.1438495

## Neg Pred Value Precision Recall

## 0.6913580 0.1438495 0.8688811

## F1 Prevalence Detection Rate

## 0.2468339 0.1546782 0.1343970

## Detection Prevalence Balanced Accuracy

## 0.9342888 0.4613120앙상블 모형의 성능은 Accuracy : 0.180, Kappa : -0.025, F1-score : 0.247, AUC : 0.539로 지금까지 만든 다른 모형보다 성능이 떨어지는 편이다.

Conclusion

- 모든 분석이 끝났다.

- 총 6개의 모형을 만들었고, 각 모형의 평가 지표가 어떻게 나왔는지 비교해보자.

| - | MARS | KNN | SVM | Random Forest | XGBoost | Ensemble |

|---|---|---|---|---|---|---|

| Accuracy | 0.713 | 0.690 | 0.846 | 0.910 | 0.180 | 0.180 |

| F1-score | 0.468 | 0.298 | 0.177 | 0.676 | 0.236 | 0.247 |

| AUC | 0.860 | 0.645 | 0.759 | 0.937 | 0.266 | 0.539 |

6개의 모형 중 랜덤포레스트 모형이 성능이 월등히 좋은 것으로 나타났다.

다만 Accuracy가 0.909로 매우 높은 수치를 보인 것에 비해 F1-score가 0.676으로 비교적 낮은 수치를 보이고 있는데, 이는 Accuracy가 전체 데이터에서 올바르게 분류한 데이터의 비율로 bias에 관한 단점을 가지기 때문이다.

랜덤 포레스트 모형의 Confusion Matrix를 보면 아래의 표와 같다.

| - | Reference | Reference |

|---|---|---|

| Prediction | FALSE | TRUE |

| FALSE | 3020 | 226 |

| TRUE | 106 | 346 |

Accuracy : 전체 데이터에서 올바르게 분류한 데이터의 비율은 (3020 + 346) / (3020 + 226 + 106 + 346) = 0.910

Precision : TRUE로 예측한 것 중에서 실제로 TRUE인 데이터의 비율은 346 / (106 + 346) = 0.765

Recall : 실제 TRUE인 값 중 TRUE로 예측한 비율은 226 / (226 + 346) = 0.395

여기서 Precision과 Recall이 둘 다 높으면 가장 좋은 방법이겠지만, 이 둘은 반비례하는 경향이 있다. 이를 보완하기 위해 이 둘의 조화평균을 사용하는 F1-score를 사용한다.