Mobile Banking App Development: Why White-Label Platforms Are Reshaping the Build Decision

Every fintech founder eventually hits the same fork in the road: build the mobile banking app from scratch, hire a specialist agency, or start from an existing platform. The decision usually gets framed as a UI question which app will look and feel best to end users. That framing is backwards. Mobile banking is, first and foremost, a backend engineering problem. The screens a user taps are the easy part. What's hard is everything underneath: ledger accuracy, transaction processing, multi-currency handling, fraud controls, and the compliance scaffolding that has to hold up under audit.

That distinction matters because it changes what "fast" actually means in mobile banking app development, and it sets up the question this article is really about: which build path lets a team move quickly without giving up control of the product they're building.

The backend is the product

A banking app's interface is a thin layer over a transaction engine. Behind every balance shown on screen sits a chain of decisions: how accounts are structured, how currencies and exchange rates are managed, how fees and limits are calculated per customer segment, how a transfer moves from pending to settled, and how all of that gets logged for compliance review. Get the UI wrong and users complain. Get the ledger wrong and you have a regulatory incident.

This is why mobile banking app projects so often run over budget and over schedule teams underestimate the backend and overinvest in the frontend. A polished interface connected to a fragile transaction core is not a banking app; it's a liability with good typography.

Three ways to build, and what each one actually costs you

Founders generally choose between three paths, and each comes with a different risk profile.

Building in-house from scratch gives full control and no vendor dependency, but it means assembling ledger logic, account and currency management, role-based permissions, KYC/compliance workflows, payment integrations, and a back-office admin panel --- all before writing a single customer-facing screen. Realistic timelines run 12-18 months for a competent team, before ongoing security audits, PCI DSS work, and the maintenance burden of owning every layer of the stack.

Outsourcing to a fintech development specialist speeds things up by bringing in people who've solved these problems before, but it introduces a different kind of risk: dependency on the vendor's roadmap, codebase, and continued availability. If the relationship ends, the client is often left holding a black box. Costs are typically lower than full in-house builds but still substantial, since the vendor is usually building bespoke rather than reusing a mature core.

Starting from a white-label banking platform flips the order of operations. Instead of building the transaction engine first and the UI second, teams start with a working core accounts, currencies, fees, limits, providers, APIs, compliance foundations and configure or extend it to fit their product. The accelerant here is significant: weeks or months instead of a year-plus, because the hardest 80% of the work is already done and already battle-tested.

The trade-off with white-label is worth naming honestly: not every vendor offers the same depth of configurability, and the biggest objection founders raise is vendor lock-in permanent dependency on someone else's SaaS, roadmap, and pricing. That objection is fair against a pure SaaS white-label model. It's the problem the next section solves.

SDK.finance: a practical foundation for mobile banking app development

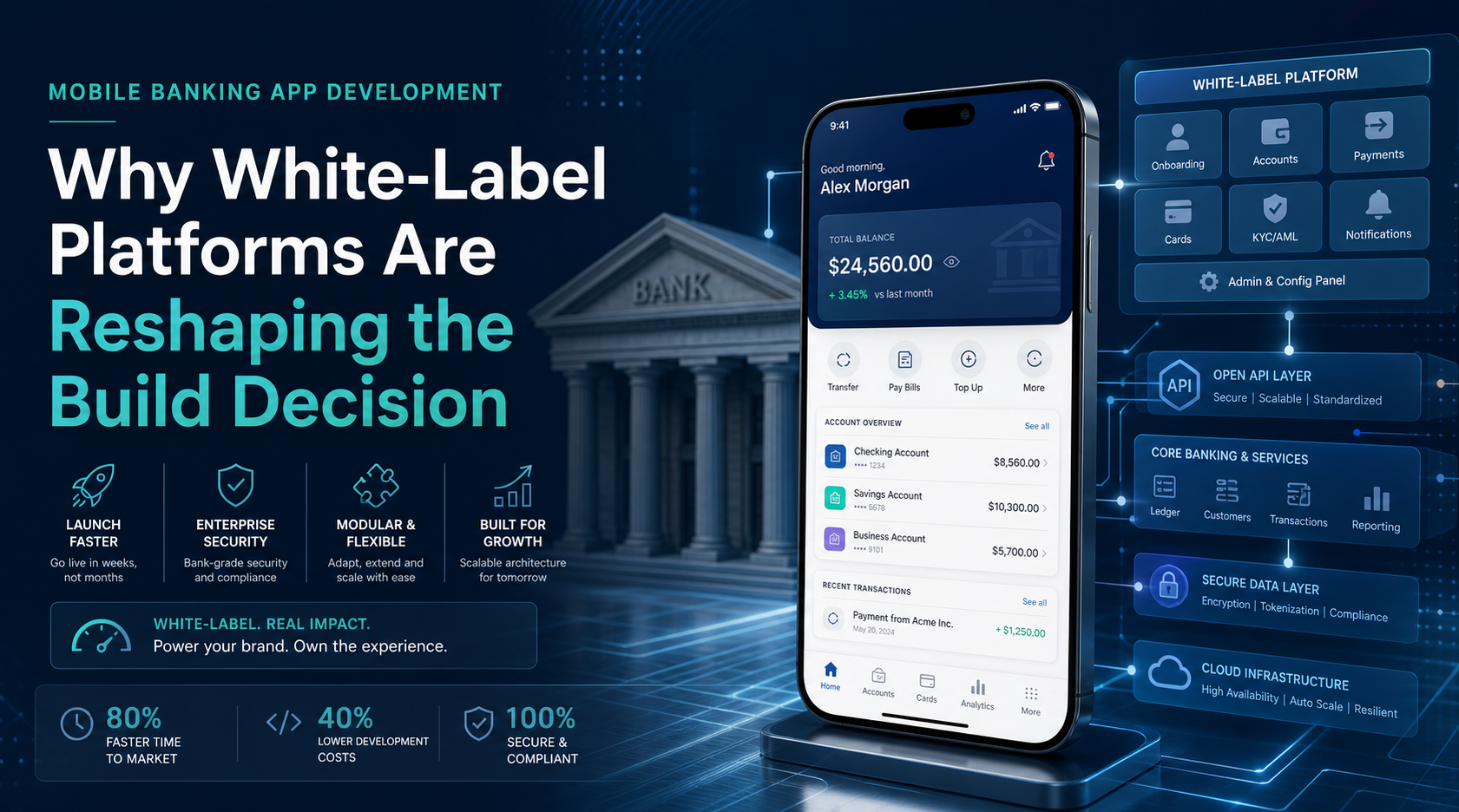

SDK.finance helps fintechs and banks launch mobile banking apps without spending years building the backend infrastructure from scratch. The Platform provides the core components every banking app needs: a real-time ledger, multi-currency accounts, transaction processing, fees and limits management, customer onboarding, KYC workflows, reconciliation tools, and operational backoffice.

Instead of building these systems from the ground up, teams can start with a ready-made fintech Platform and focus on creating their customer experience. With 570+ APIs, SDK.finance supports custom iOS, Android, and web applications while providing a single backend for all channels.

Unlike many white-label solutions, SDK.finance is available both as SaaS and as a Source Code licence. This gives businesses the flexibility to launch quickly while retaining long-term control over their technology stack, infrastructure, and product roadmap.

For companies building a mobile banking app, SDK.finance offers a faster path to market with a proven financial infrastructure already in place, allowing teams to focus on product differentiation rather than backend engineering.

What a serious evaluation should look at

Whichever path a team leans toward, a few questions tend to separate a good decision from an expensive mistake:

How deep does the configurability actually go? Some white-label platforms only let you change colors and logos. Others let you reshape currency handling, fee structures, account types, and integrate new payment providers without touching core code.

Is compliance built in or bolted on? PCI DSS certification, KYC/AML tooling, and audit-ready transaction logging are expensive and slow to build correctly. A platform with this foundation already in place removes one of the largest hidden costs of a banking product.

What does the API surface look like? Broad, well-documented API coverage means the mobile app, web app, and any future channel can be built against the same transaction core.

What happens if the relationship ends? This is the question source code licensing answers definitively and the question most pure SaaS white-label arrangements can't.

The real decision isn't build vs. buy

Framing mobile banking development as "build it yourself" versus "buy a white-label solution" misses the more useful framing: how much backend engineering risk does a team want to absorb itself, and how much control does it want to retain in exchange for taking on less of it. In-house development absorbs the most risk and offers the most control, at the highest cost in time and capital. Pure SaaS white-label absorbs the least risk but caps long-term control.

Source-code-licensed platforms like SDK.finance occupy the rare middle ground that's favorable on both axes at once: a mature, compliant, API-rich backend ready on day one, paired with full ownership of the codebase going forward. For a founder trying to ship a banking app this year rather than next, that's not just the fastest path it's the one that doesn't ask them to trade away control to get there.