Adhesion Barrier Market Growth Outlook: Innovations Driving Post-Surgical Healing Solutions

Overview

The global adhesion barrier market has been witnessing significant growth, driven by rising surgical procedures, increased awareness of postoperative complications, and advancements in surgical techniques. Adhesion barriers are medical devices used during surgeries to prevent the formation of internal scar tissue (adhesions), which can lead to complications such as chronic pain, infertility, or bowel obstruction. These barriers, available in the form of films, gels, or liquids, serve as physical obstructions that separate tissues and organs during the healing process.

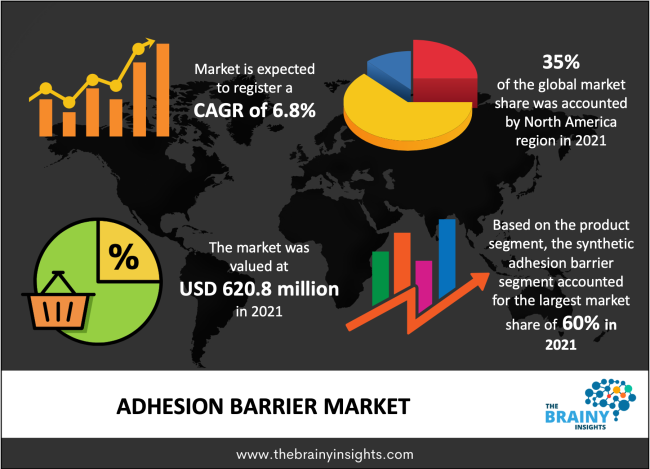

The adhesion barrier market was valued at approximately USD 620.8 million in 2021 and is expected to grow at a CAGR of around 6.8% from 2022 to 2030, reaching an estimated USD 1,120 million by the end of the forecast period.

Market Dynamics

Drivers

1. Rising Surgical Procedures: With the aging population and prevalence of chronic conditions, the demand for surgeries is surging. Adhesion barriers are increasingly being used in surgeries to reduce the risk of post-surgical adhesions.

2. Technological Advancements: Continuous innovation in materials science has resulted in the development of more effective and biocompatible adhesion barriers, enhancing their adoption in complex surgeries.

3. Increased Awareness: Growing awareness among healthcare professionals about the long-term complications of adhesions is boosting the demand for adhesion barriers in both developed and developing nations.

4. Favorable Regulatory Approvals: Regulatory bodies such as the FDA and CE have approved various novel adhesion barrier products, thereby improving their market accessibility.

Restraints

1. High Cost of Products: Adhesion barriers can be expensive, which might limit their usage in low-resource settings or in surgeries where reimbursement is not provided.

2. Limited Awareness in Emerging Markets: In many developing countries, limited awareness and lower healthcare spending restrict the widespread adoption of adhesion barriers.

3. Variable Efficacy: The effectiveness of adhesion barriers may vary based on the type of surgery and product formulation, leading to cautious adoption by surgeons.

Regional Analysis

North America

North America dominates the global adhesion barrier market, led by the U.S., owing to its advanced healthcare infrastructure, high surgical volume, favorable reimbursement landscape, and strong presence of key players. The region also benefits from increasing adoption of minimally invasive surgical techniques and robust R&D efforts.

Europe

Europe is the second-largest market, driven by a high incidence of surgeries, government funding for healthcare innovations, and patient-centric regulations. Countries such as Germany, the U.K., and France are key contributors.

Asia-Pacific

The Asia-Pacific region is expected to grow at the highest CAGR during the forecast period, fueled by the rising medical tourism industry, improving healthcare infrastructure, and growing awareness about surgical adhesions. Countries like China, India, and Japan are the primary markets.

Latin America and Middle East & Africa

These regions show moderate growth due to improving access to healthcare services and increasing surgical rates. However, limited penetration of advanced surgical products poses a challenge.

Segmental Analysis

By Product Type

• Film-Based Adhesion Barriers (dominant segment)

• Gel-Based Adhesion Barriers

• Liquid Adhesion Barriers

Film-based products are most widely used due to their easy application and high efficacy in open and laparoscopic surgeries.

By Application

• Gynecological Surgeries

• General/Abdominal Surgeries

• Orthopedic Surgeries

• Cardiovascular Surgeries

• Neurological Surgeries

• Others

General and gynecological surgeries account for a major share, given the high risk of adhesion formation in procedures like hysterectomies and cesarean sections.

By End User

• Hospitals

• Ambulatory Surgical Centers (ASCs)

• Clinics

Hospitals are the largest end users due to the high number of surgeries performed and the availability of advanced surgical equipment and materials.

Key Trends

• Shift Toward Minimally Invasive Surgeries: The trend toward laparoscopy and robotic surgeries is pushing the demand for adhesion barriers compatible with these approaches.

• Biodegradable Adhesion Barriers: Development of naturally derived and biodegradable barriers is gaining attention, offering improved safety and efficacy.

• Strategic Collaborations: Key players are entering into strategic partnerships, mergers, and acquisitions to expand product portfolios and enter untapped markets.

• Regulatory Advancements: Streamlined approval processes and supportive regulatory frameworks in emerging markets are expected to increase product availability.

Request PDF Brochure: https://www.thebrainyinsights.com/enquiry/sample-request/13058

Key Players

Some of the major players in the global adhesion barrier market include:

• Baxter International Inc.

• Johnson & Johnson (Ethicon Inc.)

• Integra LifeSciences Holdings Corporation

• Sanofi S.A.

• Anika Therapeutics, Inc.

• FzioMed, Inc.

• Mast Biosurgery AG

• Magen OrthoMed Ltd.

• Olympus Corporation

• Medical Device Business Services, Inc.

These companies focus on innovation, regulatory approvals, and geographical expansion to maintain a competitive edge.

Conclusion

The adhesion barrier market is poised for robust growth, driven by the increasing global surgical burden and the need to minimize post-operative complications. While high costs and limited access in low-income regions remain challenges, ongoing technological advancements and expanding healthcare infrastructure are expected to bridge these gaps.

With continued innovation, supportive regulations, and growing awareness, adhesion barriers are likely to become a standard component of surgical protocols, especially in high-risk procedures. The coming years will see more tailored solutions and wider adoption across specialties, firmly positioning adhesion barriers as a crucial tool in modern surgical care.