위의 결과는 각각 캔들차트를 monthly, weekly 옵션을 넣어서 돌렸을 때 걸린 시간을 나타낸 것이다.

Application Level

기존에는 다음과 같이 시간복잡도가 O(n^2) 인 코드를 작성했다.

class StockCandleChart(View):

def get(self, request):

chart_type = request.GET.get('chart_type', 'daily')

code = request.GET.get('ticker', None)

error_handler_res = handle_candle_chart_input_error(chart_type, code)

if isinstance(error_handler_res, JsonResponse):

return error_handler_res

two_years_from_now = datetime.datetime.now() - relativedelta(years=2)

ticker = Ticker.objects.get(code=code)

stock_prices_qs = StockPrice.objects.filter(ticker=ticker, date__gte=two_years_from_now).order_by('date')

if chart_type == 'daily':

stock_prices = [

{

'date' : str(stock_price_qs.date),

'bprc_adj': stock_price_qs.bprc_adj,

'prc_adj' : stock_price_qs.prc_adj,

'hi_adj' : stock_price_qs.hi_adj,

'lo_adj' : stock_price_qs.lo_adj,

'volume' : stock_price_qs.volume

} for stock_price_qs in stock_prices_qs]

else:

groups_dict = self.get_stock_price_groups_by_chart_type(chart_type, stock_prices_qs)

stock_prices = self.get_stock_prices_list(groups_dict)

data = {

'name' : ticker.stock_name,

'ticker': ticker.code,

'values': stock_prices

}

return JsonResponse({'results': data}, status=200)

def get_stock_price_groups_by_chart_type(self, chart_type, stock_prices_qs):

pre_group_num = int()

groups_dict = dict()

for stock_price_qs in stock_prices_qs:

if chart_type == 'weekly':

today = datetime.datetime.today()

this_friday = today + datetime.timedelta((calendar.FRIDAY - today.weekday()) % 7)

base_date = this_friday.date()

time_diff = (base_date - stock_price_qs.date).days

current_group_num = int(time_diff / 7)

elif chart_type == 'monthly':

current_group_num = stock_price_qs.date.strftime('%Y-%m')

groups_dict.setdefault(current_group_num, [stock_price_qs])

if current_group_num == pre_group_num:

groups_dict[current_group_num].append(stock_price_qs)

pre_group_num = current_group_num

return groups_dict

def get_stock_prices_list(self, groups_dict):

stock_prices = list()

for group in groups_dict:

stock_price_list = groups_dict[group]

first_stock_price = stock_price_list[0]

last_stock_price = stock_price_list[-1]

bprc_adj = first_stock_price.bprc_adj

prc_adj = last_stock_price.prc_adj

lowest = first_stock_price.lo_adj

highest = first_stock_price.hi_adj

volume = 0

for stock_price in stock_price_list:

if stock_price.lo_adj < lowest:

lowest = stock_price.lo_adj

if stock_price.hi_adj > highest:

highest = stock_price.hi_adj

volume += stock_price.volume

weekly_stock_price = {

'date': last_stock_price.date,

'bprc_adj': bprc_adj,

'prc_adj': prc_adj,

'hi_adj': highest,

'lo_adj': lowest,

'volume': volume

}

stock_prices.append(weekly_stock_price)

return stock_prices하지만 아무리 생각해도 너무 for 문이 많고 복잡도가 높은 것 같아서,

App Level 이 아니라, DB Level 에서 처리해보기로 했다.

DB Level

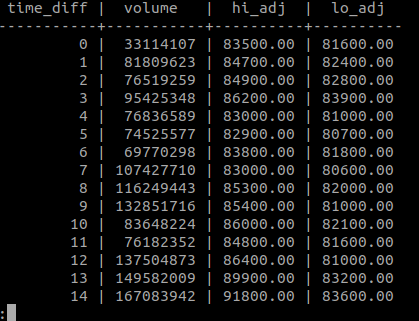

일주일 그룹 데이터의 거래량(volume), 고가(hi_adj), 저가(lo_adj) 구하기

SELECT time_diff, SUM(volume) volume, MAX(hi_adj) hi_adj, MIN(lo_adj) lo_adj

FROM (SELECT *, (date '2021-04-29' - date) / 7 as time_diff

FROM stock_prices WHERE ticker_id=3 ORDER BY date) td

GROUP BY time_diff ORDER BY time_diff;

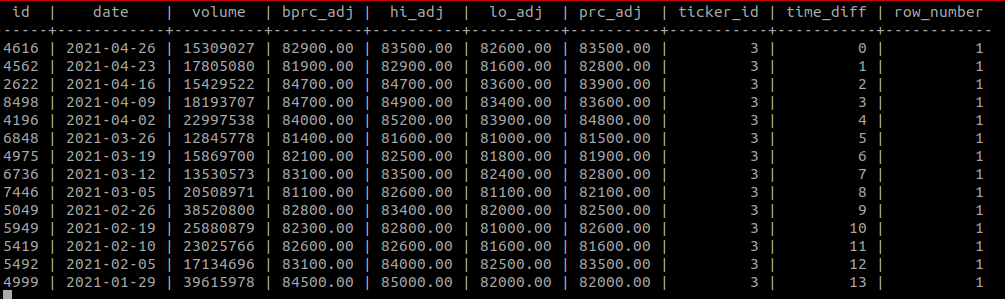

일주일 그룹 데이터의 종가(prc_adj) 구하기

weekly candle chart 는

일주일으로 묶인 주식 가격 그룹의 가장 마지막 날의 종가를 구해야한다.

SELECT *

FROM

(SELECT *, row_number() OVER(PARTITION BY time_diff ORDER BY date DESC) "row_number"

FROM (SELECT *, (date '2021-04-29' - date) / 7 as time_diff

FROM stock_prices

WHERE ticker_id=3

ORDER BY date) td) td2 WHERE row_number=1;

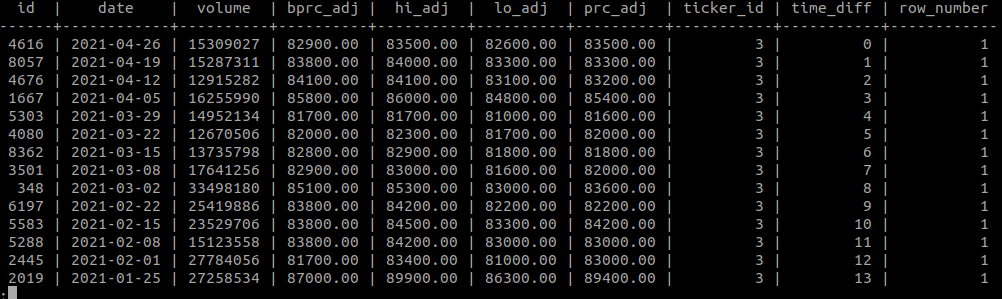

일주일 그룹 데이터의 시가(bprc_adj) 구하기

PARTITION BY 구문에서 DESC 를 ASC 로 바꿔주기만 하면 된다.

위 쿼리들은 각각 (거래량, 고가, 저가), 시가, 종가 를 세번에 걸쳐서 구한다.

이 모든걸 한 번의 쿼리로 수행되게끔 바꿀 수 있는 쿼리는 무엇인지 생각해보았다.

날짜, 거래량, 고가, 저가, 시가, 종가 한번에 SELECT 하기

SELECT

MAX(date), SUM(volume) volume, MAX(hi_adj) hi_adj, MIN(lo_adj) lo_adj, MAX(first_bprc_adj) bprc_adj, MAX(last_prc_adj) prc_adj

FROM

(

SELECT

FIRST_VALUE(bprc_adj) OVER(PARTITION BY group_id ORDER BY date) first_bprc_adj,

FIRST_VALUE(prc_adj) OVER(PARTITION BY group_id ORDER BY date DESC) last_prc_adj,

*

FROM

(SELECT *, (date '2021-04-30' - date) / 7 group_id FROM stock_prices) t1

WHERE ticker_id = 3

) t2

GROUP BY group_id

group by 에서 지정되지 않은 컬럼은 집계함수를 못쓰지만,

어차피 모두 동일한 값을 가지고 있는 필드 값들에서 max 든 min 등 하나의 값을 반환하기 때문에 이렇게 했다.

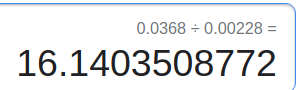

16 times faster

weekly 기준 db level 에서의 속도가 약 16배 빠르다.

Wrap-up (Final Codes)

def get_candle_chart_by_type(self, chart_type, stock_prices_qs):

if chart_type == 'daily':

results_qs = stock_prices_qs.values('date', 'bprc_adj', 'prc_adj', 'hi_adj', 'lo_adj', 'volume').order_by('date')

return list(results_qs)

if chart_type == 'weekly':

today = datetime.datetime.today()

this_friday = today + datetime.timedelta((calendar.FRIDAY - today.weekday()) % 7)

base_date = this_friday.date()

first_qs = stock_prices_qs.annotate(group_id=Cast(

ExtractDay(base_date - F('date')), IntegerField()) / 7).order_by('date')

elif chart_type == 'monthly':

first_qs = stock_prices_qs.annotate(group_id=TruncMonth(F('date'))).order_by('date')

second_qs = first_qs.values('group_id')\

.annotate(

bprc_adj=Window(

expression = FirstValue('bprc_adj'),

partition_by = F('group_id'),

order_by = F('date').asc()

),

prc_adj=Window(

expression = FirstValue('prc_adj'),

partition_by = F('group_id'),

order_by = F('date').desc()

),

date=Window(

expression = Max('date'),

partition_by = F('group_id')

),

hi_adj=Window(

expression = Max('hi_adj'),

partition_by = F('group_id')

),

lo_adj=Window(

expression = Min('lo_adj'),

partition_by = F('group_id')

),

volume=Window(

expression = Sum('volume'),

partition_by = F('group_id')

)

)\

.distinct('date')\

.values('date', 'bprc_adj', 'prc_adj', 'hi_adj', 'lo_adj', 'volume')

results = list(second_qs)

return results

Backend Developer