시계열 모형 종류

- AR(p) - 자기 회귀 모형 ,AR(1)에 적용하기 위해선 −1<ϕ1<1조건이 필요하다

- MA(q) - 이동평균 모형

- ARMA(p,q)

- ARIMA(p,d,q) - 자기회귀누적이동평균 모형 : 차수의 개수(d)는 거의 2를 넘지 않는다.

- SARIMA(Seasonal ARIMA) - 계절 자기회귀이동평균 모형

▪ AR – 자기회기 모형

• AR(Autoregressive) 모델은 자기회귀(Autoregressive) 모델로 자기상관성을 시계열 모델로

구성한 것이다.

• 예측하고 싶은 특정 변수의 과거 자신의 데이터와 선형 결합을 통해 특정 시점 이후 미래값을

예측하는 모델이다.

• 이름 그대로 이전 자신의 데이터가 이후 자신의 미래 관측값에 영향을 끼친다는 것을 기반으로

나온 모델이다.

• AR(1)에 적용하기 위해선 −1<ϕ1<1조건이 필요하다.

# ArmaProcess로 모형 생성하고 nobs 만큼 샘플 생성

from statsmodels.tsa.arima_process import ArmaProcess

def gen_arma_samples (ar,ma,nobs):

arma_model = ArmaProcess(ar=ar, ma=ma) # 모형 정의

arma_samples = arma_model.generate_sample(nobs) # 샘플 생성

return arma_samples

# drift가 있는 모형은 ArmaProcess에서 처리가 안 되어서 수동으로 정의해줘야 함

def gen_random_walk_w_drift(nobs,drift):

init = np.random.normal(size=1, loc = 0)

e = np.random.normal(size=nobs, scale =1)

y = np.zeros(nobs)

y[0] = init

for t in (1,nobs):

y[t] = drift + 1 * y[t-1] + e[t]

return y

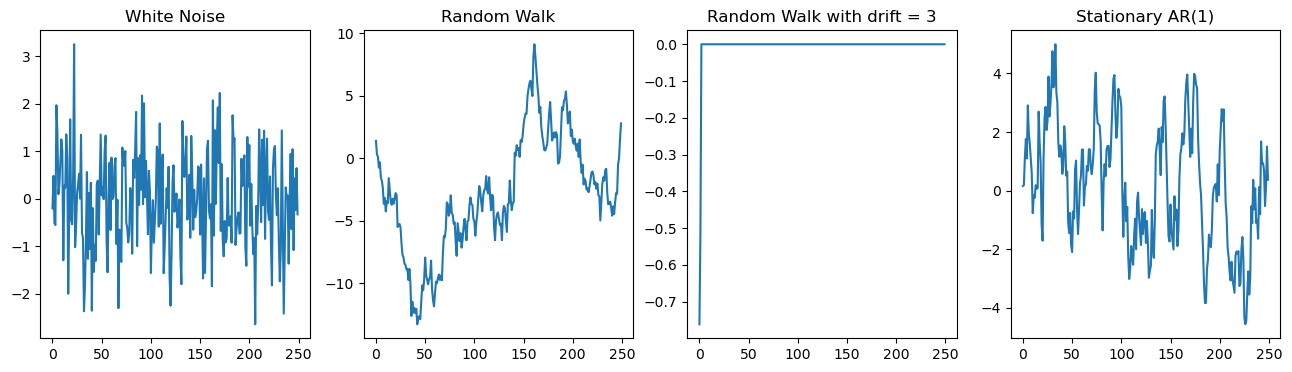

## AR 모형

np.random.seed(12345)

white_noise= gen_arma_samples(ar = [1], ma = [1], nobs = 250)

# y_t = epsilon_t

random_walk = gen_arma_samples(ar = [1,-1], ma = [1], nobs = 250)

# (1 - L)y_t = epsilon_t

random_walk_w_drift = gen_random_walk_w_drift(250, 2)

# y_t = 2 + y_{t-1} + epsilon_t

stationary_ar_1 = gen_arma_samples(ar = [1,-0.9], ma = [1],nobs=250)

# (1 - 0.9L) y_t = epsilon_timport matplotlib.pyplot as plt

fig,ax = plt.subplots(1,4)

ax[0].plot(white_noise)

ax[0].set_title("White Noise")

ax[1].plot(random_walk)

ax[1].set_title("Random Walk")

ax[2].plot(random_walk_w_drift)

ax[2].set_title("Random Walk with drift = 3")

ax[3].plot(stationary_ar_1)

ax[3].set_title("Stationary AR(1)")

fig.set_size_inches(16,4)

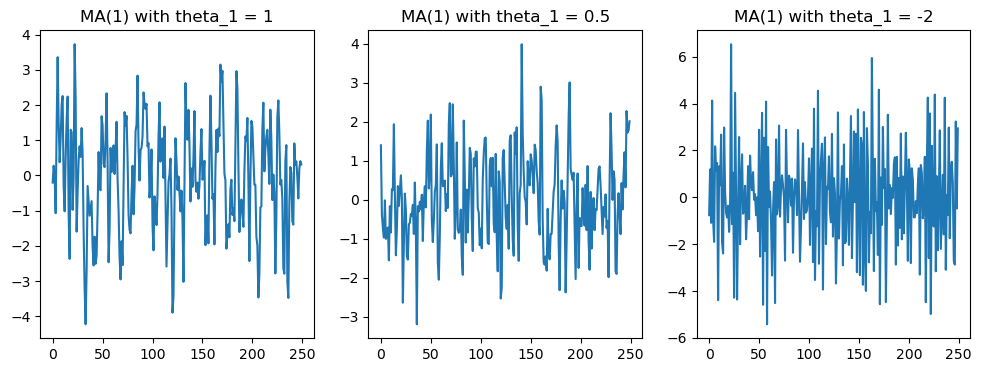

MA 모형

## MA 모형

np.random.seed(12345)

ma_1 = gen_arma_samples(ar = [1], ma = [1,1], nobs = 250) # y_t = (1+L) epsilon_t

ma_2 = gen_arma_samples(ar = [1], ma = [1,0.5], nobs = 250) # y_t = (1+0.5L)epsilon_t

ma_3 = gen_arma_samples(ar = [1], ma = [1,-2], nobs = 250) # y_t = (1-2L) epsilon_t

fig,ax = plt.subplots(1,3, figsize = (12,4))

ax[0].plot(ma_1)

ax[0].set_title("MA(1) with theta_1 = 1")

ax[1].plot(ma_2)

ax[1].set_title("MA(1) with theta_1 = 0.5")

ax[2].plot(ma_3)

ax[2].set_title("MA(1) with theta_1 = -2")

plt.show()

위 그림에서 볼 수 있듯이 θ1의 값에 따라 모형 형태가 약간 다르긴 하지만 특정한

트렌드도 없고 평균과 분산이 일정하기 때문에 정상성을 만족함을 확인하실 수 있다.

Just Enjoy Yourself