캐글의 산탄데르 고객 만족 데이터셋에 대해 LigthGBM과 XGBoost를 활용하여 예측한다. feature은 총 370개, 클래스 레이블 명은 TARGET이고, 이때 해당 값이 1이면 불만을 가진 고객, 0이면 만족한 고객을 의미한다.

이때, 불균형 데이터셋이므로 모델 성능 평가는 정확도가 아닌 roc-auc로 진행한다.

ch4.9 Data

데이터셋은 여기 https://www.kaggle.com/c/santander-customer-satisfaction 에서 다운받을 수 있다.

- 데이터 로드

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import matplotlibcust_df = pd.read_csv("/content/drive/MyDrive/파이썬 머신러닝 완벽 가이드/data/santander-customer-satisfaction/train.csv", encoding='latin-1')cust_df.shape- 데이터 확인

- 370개의 feature, 1개의 class 열로 구성된 dataframe

- 260개의 정수형 feature, 111개의 실수형 feature로 구성됨

- 결측값은 없음

cust_df.info()

## 각 피처의 분포 확인

cust_df.describe()

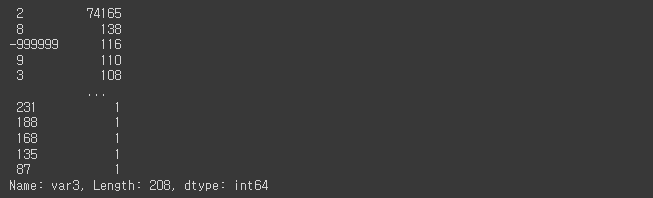

위 결과를 살펴보면, var3의 경우 min 값이 -999999이다. 해당 값은 NaN 또는 이상치 값에 해당되므로 가장 값이 많은 2로 변환할 예정이다. (아래 전처리 정리 내용 참고)

ch4.9 Preprocessing

- feature var3 의 이상치 부분 확인

## var3의 -999999 값 => 116개 은 결측값 혹은 이상치에 해당함

## 해당 값을 가장 값이 많은 2로 변환함

cust_df['var3'].value_counts()

- 해당 값을 값이 가장 많은 2로 변환

## -999999 => 2

cust_df['var3'].replace(-99999, 2, inplace=True)- feature ID 는 단순 식별자에 해당하므로 드롭

## ID 열은 단순 식별자에 해당하므로 드롭

cust_df.drop('ID', axis=1, inplace=True)

- feature 과 class 분리

## feature과 class 분리

X_features = cust_df.iloc[:, :-1]

y_labels = cust_df.iloc[:, -1]- train, val, test 으로 데이터셋 분리 (불균형 데이터셋임을 고려하여 비슷한 비율로 split 되었는지를 확인!)

from sklearn.model_selection import train_test_split

## train, test 데이터 분리

X_train, X_test, y_train, y_test = train_test_split(

X_features,

y_labels,

test_size=0.2,

random_state=0

)## 불균형한 데이터셋이므로 traget 값 분포도 확인

print(y_train.value_counts() / y_train.count())

print(y_test.value_counts() / y_test.count())## XGBoost, LightGBM의 early stopping을 사용하기 위해 train => train, val로 다시 분리

X_tr, X_val, y_tr, y_val = train_test_split(

X_train,

y_train,

test_size=0.3,

random_state=0

)ch4.9 XGBoost Model

- HyperOpt를 사용하여 XGBoost 최적 하이퍼 파라미터 찾기

- 지난 글에서 정리한 바와 같이 HyperOpt를 사용하여 하이퍼 파라미터 튜닝을 수행할 때, 1) 검색 공간 설정 2) 목적 함수 설정 3) fmin()으로 최적 하이퍼 파라미터 찾기 순서로 진행됨

- 주의사항은 XGBoost와 LightGBM에서는 cross_val_score()를 적용하면 early stopping 지원 불가하다는 것! 따라서 KFold 방식으로 직접 구현해야 함

## 1) 검색 공간 설정

from hyperopt import hp

xgb_search_space = {

'max_depth':hp.quniform('max_depth', 5, 15, 1), ## 정수형 하이퍼 파라미터 => quniform 사용

'min_child_weight':hp.quniform('min_child_weight', 1, 6, 1), ## 정수형 하이퍼 파라미터 => quniform 사용

'learning_rate':hp.uniform('learning_rate', 0.01, 0.2),

'colsample_bytree':hp.uniform('colsample_bytree', 0.5, 0.95),

}

## 2) 목적 함수 설정

from sklearn.model_selection import KFold

from sklearn.metrics import roc_auc_score

from xgboost import XGBClassifier

from sklearn.metrics import roc_auc_score

def objective_func(search_space):

xgb_clf = XGBClassifier(

n_estimators=100,

max_depth=int(search_space['max_depth']), ## int형으로 형변환 필요

min_child_weight=int(search_space['min_child_weight']), ## int형으로 형변환 필요

learning_rate=search_space['learning_rate'],

colsample_bytree=search_space['colsample_bytree'],

#eval_metric='logloss' => 불균형 데이터셋이므로 성능 평가 지표를 roc-auc로 설정

)

## XGBoost와 LightGBM에서는 cross_val_score()를 적용하면 early stopping 지원 불가, KFold 방식으로 직접 구현해야 함

## 3개의 k-fold 방식으로 평가된 roc-auc 지표를 담는 list

roc_auc_list = []

## 3개의 k-fold 방식 적용

kf = KFold(n_splits=3)

for tr_index, val_index in kf.split(X_train):

X_tr, y_tr = X_train.iloc[tr_index], y_train.iloc[tr_index]

X_val, y_val = X_train.iloc[val_index], y_train.iloc[val_index]

xgb_clf.fit(

X_tr, y_tr,

early_stopping_rounds=30,

eval_metric='auc',

eval_set=[(X_tr, y_tr), (X_val, y_val)]

)

score = roc_auc_score(

y_val,

xgb_clf.predict_proba(X_val)[:, 1]

)

roc_auc_list.append(score)

return (-1) * np.mean(roc_auc_list)

## 3) fmin()을 사용하여 최적 하이퍼 파라미터 찾기

from hyperopt import fmin, tpe, Trials

trials = Trials()

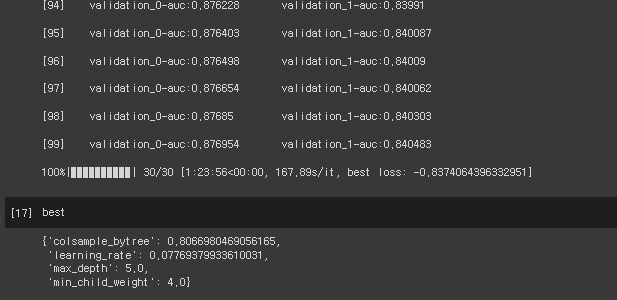

best = fmin(

fn=objective_func,

space=xgb_search_space,

algo=tpe.suggest,

max_evals=50,

trials=trials,

)

- 최적 하이퍼 파라미터를 이용하여 XGBoost 모델 선언

## 획득한 최적의 하이퍼 파라미터를 이용하여 모델 선언

xgb_wrapper = XGBClassifier(

n_estimators=500,

learning_rate=round(best['learning_rate'], 5),

max_depth=int(best['max_depth']),

min_child_weight=int(best['min_child_weight']),

colsample_bytree=round(best['colsample_bytree'], 5)

)- 모델 학습

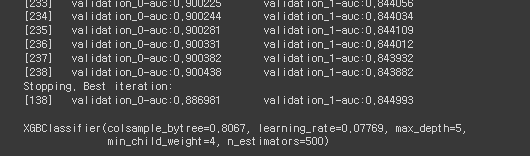

xgb_wrapper.fit(

X_tr, y_tr,

early_stoppin_rounds=100,

eval_metric='auc',

eval_set=[(X_tr, y_tr), (X_test, y_test)]

)

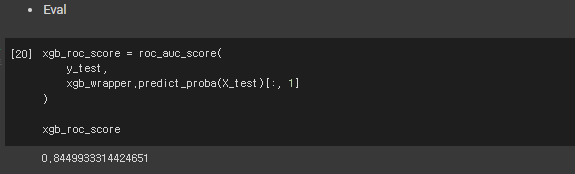

- 모델 평가

xgb_roc_score = roc_auc_score(

y_test,

xgb_wrapper.predict_proba(X_test)[:, 1]

)

xgb_roc_score

- feature importance 확인

from xgboost import plot_importance

import matplotlib.pyplot as plt

fig, ax = plt.subplots(1, 1, figsize=(10, 8))

plot_importance(xgb_wrapper,

ax=ax,

max_num_features=20,

height=0.4,

)

행복한 소히의 이것저것