scikit-learn 주요 모듈 : 강의

- 다양한 머신러닝 알고리즘을 구현한 파이썬 라이브러리

- 심플하고 일관성 있는 API, 유용한 온라인 문서, 풍부한 예제

- 머신러닝을 위한 쉽고 효율적인 개발 라이브러리 제공

- 다양한 머신러닝 관련 알고리즘과 개발을 위한 프레임워크와 API 제공

- 많은 사람들이 사용하며 다양한 환경에서 검증된 라이브러리

scikit-learn 주요 모듈

| sklearn.datasets | 내장된 예제 데이터 세트 |

|---|---|

| sklearn.preprocessing | 다양한 데이터 전처리 기능 제공 (변환, 정규화, 스케일링 등) |

| sklearn.feature_selection | 특징(feature)를 선택할 수 있는 기능 제공 |

| sklearn.feature_extraction | 특징(feature) 추출에 사용 |

| sklearn.decomposition | 차원 축소 관련 알고리즘 지원 (PCA, NMF, Truncated SVD 등) |

| sklearn.model_selection | 교차 검증을 위해 데이터를 학습/테스트용으로 분리, 최적 파라미터를 추출하는 API 제공 (GridSearch 등) |

| sklearn.metrics | 분류, 회귀, 클러스터링, Pairwise에 대한 다양한 성능 측정 방법 제공 (Accuracy, Precision, Recall, ROC-AUC, RMSE 등) |

| sklearn.pipeline | 특징 처리 등의 변환과 ML 알고리즘 학습, 예측 등을 묶어서 실행할 수 있는 유틸리티 제공 |

| sklearn.linear_model | 선형 회귀, 릿지(Ridge), 라쏘(Lasso), 로지스틱 회귀 등 회귀 관련 알고리즘과 SGD(Stochastic Gradient Descent) 알고리즘 제공 |

| sklearn.svm | 서포트 벡터 머신 알고리즘 제공 |

| sklearn.neighbors | 최근접 이웃 알고리즘 제공 (k-NN 등) |

| sklearn.naive_bayes | 나이브 베이즈 알고리즘 제공 (가우시안 NB, 다항 분포 NB 등) |

| sklearn.tree | 의사 결정 트리 알고리즘 제공 |

| sklearn.ensemble | 앙상블 알고리즘 제공 (Random Forest, AdaBoost, GradientBoost 등) |

| sklearn.cluster | 비지도 클러스터링 알고리즘 제공 (k-Means, 계층형 클러스터링, DBSCAN 등) |

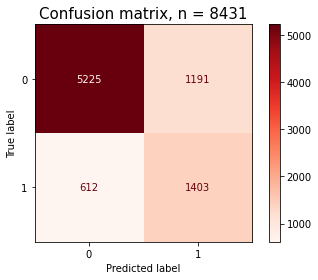

confusion matrix

# model1, Random Forest, confusion matrix

pcm = ConfusionMatrixDisplay.from_predictions(y_val,

y_pred_optimal1,

cmap=plt.cm.Reds)

plt.title(f'Confusion matrix, n = {len(y_val)}', fontsize=15)

RandomForestClassifier : 참고

pipe = make_pipeline(

OrdinalEncoder(),

SimpleImputer(),

RandomForestClassifier(

n_estimators=500,

criterion="entropy",

random_state=10,

oob_score=True,

# max_depth=3,

# oob_score=True,

# warm_start=True,

# max_features=0.25,

n_jobs=-1

)

)

pipe.fit(X_train, y_train)# roc_curve(타겟값, prob of 1)

y_pred_proba = model1.predict_proba(X_val)[:, 1]

fpr1, tpr1, thresholds1 = roc_curve(y_val, y_pred_proba)

# threshold 최대값의 인덱스, np.argmax()

optimal_idx = np.argmax(tpr1 - fpr1)

optimal_threshold = thresholds1[optimal_idx]

# threshold 최대값으로 설정

y_pred_optimal = y_pred_proba >= optimal_threshold

print(f'auc score:{roc_auc_score(y_val, y_pred_proba)}')

print('검증세트 F1-score', f1_score(y_val, y_pred_optimal))

print(classification_report(y_val, y_pred_optimal))# 테스트 데이터 입력 후 결과 출력

y_pred = model1.predict(X_test)

y_pred_optimal = y_pred >= optimal_threshold

y_pred_optimal = y_pred_optimal.astype(int)

sample_submission['vacc_h1n1_f'] = y_pred

sample_submission.to_csv('submission_op.csv',index=False)XGBClassifier: 참고

from xgboost import XGBClassifier

# xgboost model

model2 = make_pipeline(

OrdinalEncoder(),

SimpleImputer(),

XGBClassifier(

n_estimators=3000,

learning_rate=0.01

)

)

model2.fit(X_train, y_train)교차검증(k-fold cross-validation(CV)):참고

#cross_val_score

from category_encoders import OneHotEncoder

from sklearn.feature_selection import f_regression, SelectKBest

from sklearn.impute import SimpleImputer

from sklearn.linear_model import Ridge

from sklearn.model_selection import cross_val_score

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import StandardScaler

# (참고) warning 제거를 위한 코드

np.seterr(divide='ignore', invalid='ignore')

target = 'SalePrice'

features = train.columns.drop([target])

X_train = train[features]

y_train = train[target]

X_test = test[features]

y_test = test[target]

pipe = make_pipeline(

OneHotEncoder(use_cat_names=True),

SimpleImputer(strategy='mean'),

StandardScaler(),

SelectKBest(f_regression, k=20),

Ridge(alpha=1.0)

)

# 3-fold 교차검증을 수행합니다.

k = 3

scores = cross_val_score(pipe, X_train, y_train, cv=k,

scoring='neg_mean_absolute_error')

print(f'MAE ({k} folds):', -scores)# 랜덤포레스트

from category_encoders import TargetEncoder

from sklearn.ensemble import RandomForestRegressor

pipe = make_pipeline(

# TargetEncoder: 범주형 변수 인코더로, 타겟값을 특성의 범주별로 평균내어 그 값으로 인코딩

TargetEncoder(min_samples_leaf=1, smoothing=1),

SimpleImputer(strategy='median'),

RandomForestRegressor(max_depth = 10, n_jobs=-1, random_state=2)

)

k = 3

scores = cross_val_score(pipe, X_train, y_train, cv=k,

scoring='neg_mean_absolute_error')

print(f'MAE for {k} folds:', -scores)TargetEncoder: 참고

범주형 변수 인코더로, 타겟값을 특성의 범주별로 평균내어 그 값으로 인코딩

enc = TargetEncoder(min_samples_leaf=1, smoothing=1000)

enc.fit_transform(X_train,y_train)['LotShape'].value_counts()하이퍼파라미터튜닝

Randomized Search CV :참고

# ridge 회귀

from sklearn.model_selection import RandomizedSearchCV

pipe = make_pipeline(

OneHotEncoder(use_cat_names=True)

, SimpleImputer()

, StandardScaler()

, SelectKBest(f_regression)

, Ridge()

)

# 튜닝할 하이퍼파라미터의 범위를 지정해 주는 부분

dists = {

'simpleimputer__strategy': ['mean', 'median'],

'selectkbest__k': range(1, len(X_train.columns)+1),

'ridge__alpha': [0.1, 1, 10],

}

clf = RandomizedSearchCV(

pipe,

param_distributions=dists,

n_iter=50,

cv=3,

scoring='accuracy',

verbose=1,

n_jobs=-1

)

clf.fit(X_train, y_train);

print('최적 하이퍼파라미터: ', clf.best_params_)

# 위에서 찾은 최적 하이퍼파라미터를 적용한 모델 생성.

pipe = clf.best_estimator_

# 위 최적 모델에 훈련/검증 데이터 넣고 스코어 추출.

y_val_pred = pipe.predict(X_val)

y_train_pred = pipe.predict(X_train)

print('훈련 f1 score: ', f1_score(y_train, y_train_pred, average='binary'))

print('검증 f1 score: ', f1_score(y_val, y_val_pred, average='binary'))#랜덤포레스트

from scipy.stats import randint, uniform

pipe = make_pipeline(

OrdinalEncoder(),

SimpleImputer(),

RandomForestClassifier(random_state=2)

)

dists = {

'simpleimputer__strategy': ['mean', 'median', 'most_frequent'],

'randomforestclassifier__n_estimators': randint(50, 500),

'randomforestclassifier__max_depth': [5, 10, 15, 20, None],

'randomforestclassifier__max_features': uniform(0, 1)

}

clf = RandomizedSearchCV(

pipe,

param_distributions=dists,

n_iter=50,

cv=3,

scoring='accuracy',

verbose=1,

n_jobs=-1

)

clf.fit(X_train, y_train);

print('최적 하이퍼파라미터: ', clf.best_params_)

print('MAE: ', -clf.best_score_)

# 위에서 찾은 최적 하이퍼파라미터를 적용한 모델 생성.

pipe = clf.best_estimator_

# 위 최적 모델에 훈련/검증 데이터 넣고 스코어 추출.

y_val_pred = pipe.predict(X_val)

y_train_pred = pipe.predict(X_train)

print('훈련 f1 score: ', f1_score(y_train, y_train_pred, average='binary'))

print('검증 f1 score: ', f1_score(y_val, y_val_pred, average='binary'))# 위에서 찾은 최적 하이퍼파라미터를 적용한 모델 생성. 특성 중요도(feature importance)

# 특성 중요도(ordinal)

rf_ord = pipe.named_steps['randomforestclassifier']

importances_ord = pd.Series(rf_ord.feature_importances_, X_train.columns)

n = 10

plt.figure(figsize=(10,n/4))

plt.title(f'Top {n} features with ordinalencoder')

importances_ord.sort_values()[-n:].plot.barh();Bayesian Search

- 검증하고자 하는 하이퍼파라미터의 범위 내에서, 이전에 탐색한 조합들의 성능을 기반으로 성능이 잘 나오는 조합들을 중심으로 확률적으로 탐색합니다.

- 랜덤 서치보다 상대적으로 똑똑하고 효율적으로 탐색하는 방법으로, 한정된 자원 내에서 좋은 하이퍼파라미터 조합을 발견할 가능성이 더 높습니다.

sklearn에서는 이 기능을 제공하지 않으며, 일반적으로hyperopt등의 라이브러리를 추가 사용해서 탐색을 진행하게 됩니다.

[hyperopt](http://hyperopt.github.io/hyperopt/getting-started/search_spaces/) 라이브러리

hyperopt라이브러리를 이용해 하이퍼파라미터를 탐색할 때는 하이퍼파라미터 범위를hyperopt라이브러리에서 제공하는stochastic expressions로 지정해 주어야 합니다.- 몇 가지 자주 사용하는

expression들을 소개합니다.hp.choice(label, options): 리스트나 튜플 형태의 선택지 중 하나를 선택합니다.hp.randint(label, upper): [0, upper] 범위 내의 정수값을 랜덤으로 선택합니다.hp.uniform(label, low, high): [low, high] 범위 내의 실수값을 랜덤으로 선택합니다.hp.quniform(label, low, high, q): [low, high] 사이 균등분포에서 q 간격의 일정 지점들로부터 값을 랜덤으로 선택합니다.hp.normal(label, mu, sigma): 평균 mu, 표준편차 sigma를 갖는 정규분포로부터 실수값을 랜덤으로 선택합니다.

- • 자세한 내용은 여기를 참고하세요.

from hyperopt import hp

params = {

"simpleimputer__strategy": hp.choice("strategy", ["median", "mean"]),

"randomforestclassifier__max_depth": hp.quniform("max_depth", 2, 10, 2),

"randomforestclassifier__max_features": hp.uniform("max_features", 0.5, 1.0),

}hyperopt라이브러리 사용 시 학습 및 검증 함수를 직접 작성해 주어야 합니다.hyperopt.fmin은 주어진 함수로부터 loss 정보를 얻고, 이 정보로부터 다음 탐색할 하이퍼파라미터 조합을 선택합니다.- 최종으로

loss를 가장 작게 만드는 하이퍼파라미터 조합을 선택하므로, 클수록 좋은 metric의 경우 -부호를 붙여 반환해 주어야 합니다. - 따라서 학습 및 검증을 위한 함수는 아래와 같이 loss와 status라는 상태를 반환해야 합니다.

fmin의max_evals만큼 fitting을 진행하게 됩니다.

from hyperopt import fmin, tpe, Trials, STATUS_OK

from sklearn.model_selection import cross_val_score

import numpy as np

def get_pipe(params):

params["randomforestclassifier__max_depth"] = int(

params["randomforestclassifier__max_depth"]

) # max_depth는 정수형으로 변환해 줍니다.

pipe = make_pipeline(

OrdinalEncoder(),

SimpleImputer(),

RandomForestClassifier(

n_estimators=500,

random_state=42,

n_jobs=-1,

),

)

pipe = pipe.set_params(**params)

return pipe

def fit_and_eval(params):

pipe = get_pipe(params) # 주어진 params로 파이프라인을 만들어 가져옵니다.

score = cross_val_score(pipe, X_train, y_train, cv=3, scoring="roc_auc")

avg_cv_score = np.mean(score)

# roc_auc는 클수록 좋은 metric이므로, hyperopt.fmin이 roc_auc를 최대화하도록 하기 위해 -부호를 붙여 반환합니다.

return {"loss": -avg_cv_score, "status": STATUS_OK}

trials = (

Trials()

) # Trials() 객체를 fmin에 함께 넣어 실행하면, 실행되는 매 fit의 학습 정보 및 학습 결과가 해당 객체에 모두 저장됩니다.

best_params = fmin(

fn=fit_and_eval, trials=trials, space=params, algo=tpe.suggest, max_evals=10

) # max_evals 횟수만큼 하이퍼파라미터 조합을 탐색합니다.trials.trials # 모든 trial 정보에 대해 직접 접근할 수 있습니다.print("최적 하이퍼파라미터: ", trials.best_trial["misc"]["vals"])

print("최적 AUC: ", -trials.best_trial["result"]["loss"])

ENTJ 데이터 분석가 준비중입니다:)