There were a lot of improvement for this model.

Change in # of Features

The biggest change is that I added more columns for the dataset. It now refers to:

- RSI

- MACD

- Bollinger Bands

- ATR

- VIX_Relative

def get_dataset_columns(ticker, period="1y", window_size=60):

df = yf.Tickers(ticker).history(period=period, progress=False)

vix_data = yf.Tickers("^VIX").history(period=period, progress=False)

if isinstance(df.columns, pd.MultiIndex):

df.columns = df.columns.droplevel(1)

if isinstance(vix_data.columns, pd.MultiIndex):

vix_data.columns = vix_data.columns.droplevel(1)

df = df.ffill().dropna()

vix_data = vix_data.reindex(df.index).ffill()

open_trend = apply_ssa_trend(df['Open'].values, window=int((window_size/4)))

vix_trend = apply_ssa_trend(vix_data['Open'].values, window=int((window_size/4)))

min_len = min(len(df), len(open_trend), len(vix_trend))

df = df.iloc[:min_len]

########################################################################

# Features

df['Open_Trend'] = open_trend[:min_len]

df['Vix_Trend'] = vix_trend[:min_len]

df['Trend_Diff'] = df['Open'] - df['Open_Trend']

df['Vix_Trend_Diff'] = vix_data['Open'] - df['Vix_Trend']

df['RSI'] = ta.rsi(df['Open'], length=14)

macd = ta.macd(df['Open'])

df = pd.concat([df, macd], axis=1)

bbands = ta.bbands(df['Open'], length=20)

df = pd.concat([df, bbands], axis=1)

df['ATR'] = ta.atr(df['High'], df['Low'], df['Open'], length=14)

df['VIX_Rel'] = vix_data['Open'] / vix_data['Open'].rolling(20).mean()

########################################################################

# Target

df['Target'] = (df['Open'].shift(-1) - df['Open']) / df['Open'] * 100

# df['Target'] = np.log(df['Open'].shift(-1) / df['Open']) * 100

# df['Target'] = df['Open'].shift(-1)

########################################################################

df = df.iloc[:-1]

df = df.drop(df.index[0])

# df = df.drop(['High', 'Low', 'Volume', 'Close', 'Stock Splits', 'Dividends'], axis=1)

df.columns.name = None

exclude_cols = ['Open', 'High', 'Low', 'Close', 'Adj Close', 'Volume', 'Target']

feature_cols = [c for c in df.columns if c not in exclude_cols]

target_col = ["Target"]

return df, feature_cols, target_col

def get_full_dataset(tickers, period="1y", window_size=60, test_size=0.2):

X_total, y_total = [], []

for ticker in tickers:

df, feature_cols, target_col = get_dataset_columns(ticker, period=period, window_size=window_size)

data_x = df[feature_cols].values

data_y = df[target_col].values

for i in range(len(df) - window_size):

window_x = data_x[i : i + window_size]

window_y = data_y[i + window_size]

window_x = normalize_window(window_x)

X_total.append(window_x)

y_total.append(window_y)

X_data = np.array(X_total)

y_data = np.array(y_total)

nan_mask = np.isnan(X_data).any(axis=(1, 2))

X_data = X_data[~nan_mask]

y_data = y_data[~nan_mask]

print(f"NaN Deleted: {np.sum(nan_mask)}")

test_first_index = int(len(X_data) * (1 - test_size))

X_train, X_test = X_data[:test_first_index], X_data[test_first_index:]

y_train, y_test = y_data[:test_first_index], y_data[test_first_index:]

print("""

X_train Shape : {}

X_test Shape : {}

y_train Shape : {}

y_test Shape : {}

""".format(X_train.shape, X_test.shape, y_train.shape, y_test.shape))

return X_train, X_test, y_train, y_testSame preprocessing steps can be performed for real life predictions

def get_data_for_prediction(ticker, period="120d", window_size=60):

df, feature_cols, _ = get_dataset_columns(ticker, period=period, window=window_size)

if len(df) < window_size:

raise ValueError("Not enough rows")

X = df[feature_cols].iloc[-window_size:].values

if np.isnan(X).any():

raise ValueError("NaN detected in prediction window")

X = normalize_window(X)

X = X.reshape(1, window_size, len(feature_cols))

return XThe same CNN-LSTM model is used

def get_CNN_LSTM_hybrid(window_size=60, feature_num=3):

dropout_rate = 0.2

input_layer = Input(shape=(window_size, feature_num), name="Input")

x = Conv1D(filters=64, kernel_size=3, strides=1, padding='same', activation='relu', name="Conv1D_1")(input_layer)

x = LayerNormalization(name="LayerNormalization_1")(x)

x = Conv1D(filters=64, kernel_size=3, strides=1, padding='same', activation='relu', name="Conv1D_2")(x)

x = LayerNormalization(name="LayerNormalization_2")(x)

x = MaxPooling1D(pool_size=2, name="Max_Pooling")(x)

x = LSTM(64, return_sequences=True, name="LSTM_1")(x)

x = Dropout(dropout_rate, name="Dropout_1")(x)

x = BatchNormalization(name="BatchNormalization_1")(x)

x = LSTM(32, return_sequences=False, name="LSTM_2")(x)

x = Dropout(dropout_rate, name="Dropout_2")(x)

x = BatchNormalization(name="BatchNormalization_2")(x)

x = Dense(16, activation="relu", name="FullyConnected_1")(x)

output_layer = Dense(1, activation="linear", name="Output")(x)

model = Model(inputs=input_layer, outputs=output_layer, name='SSA_CNN_LSTM_Hybrid')

optimizer = tf.keras.optimizers.Adam(learning_rate=0.001)

model.compile(optimizer=optimizer,

loss='mse',

metrics=['mae', tf.keras.metrics.RootMeanSquaredError()])

return model

CNN_LSTM_model = get_CNN_LSTM_hybrid(window_size, feature_num)Evaluating

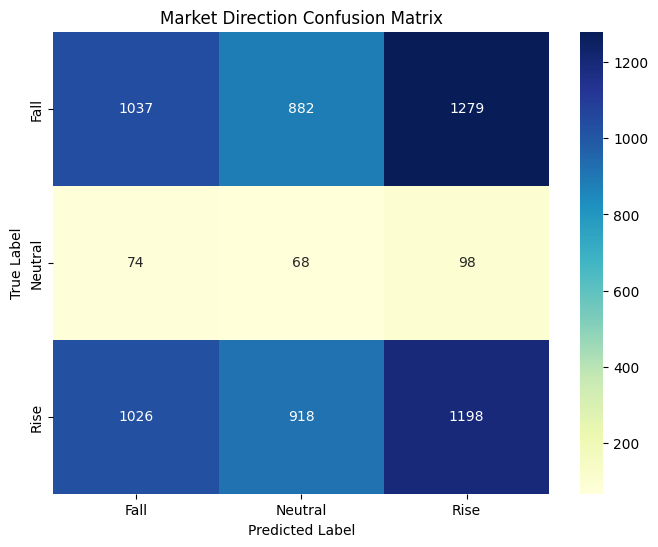

Unlike how I only evaluated the model by ‘rise’ and ‘fall’, now I added ‘neutral (hold)’.

def make_3class_label(y, threshold=0.05):

labels = np.zeros_like(y, dtype=int)

labels[y > threshold] = 2

labels[(y > 0) & (y <= threshold)] = 1

labels[y <= 0] = 0

return labels

predictions = CNN_LSTM_model.predict(X_test)

print(pd.DataFrame(predictions).describe())

# base_point = pd.DataFrame(predictions).mean().item()

base_point = 0

class_names = ['Fall', 'Neutral', 'Rise']

threshold = 0.1

y_test_class = make_3class_label(y_test, threshold)

predictions_class = make_3class_label(predictions, threshold)

unique, counts = np.unique(y_test_class, return_counts=True)

print("Test set class distribution:")

for u, c in zip(unique, counts):

print(f"Class {u}: {c} samples")

unique, counts = np.unique(predictions_class, return_counts=True)

print("\nPrediction set class distribution:")

for u, c in zip(unique, counts):

print(f"Class {u}: {c} samples")

plt.figure(figsize=(8, 6))

cm = confusion_matrix(y_test_class, predictions_class)

sns.heatmap(cm, annot=True, fmt='d', cmap='YlGnBu',

xticklabels=class_names,

yticklabels=class_names)

plt.title('Market Direction Confusion Matrix')

plt.xlabel('Predicted Label')

plt.ylabel('True Label')

plt.show()

print("\nClassification Report:")

print(classification_report(y_test_class, predictions_class, target_names=class_names))

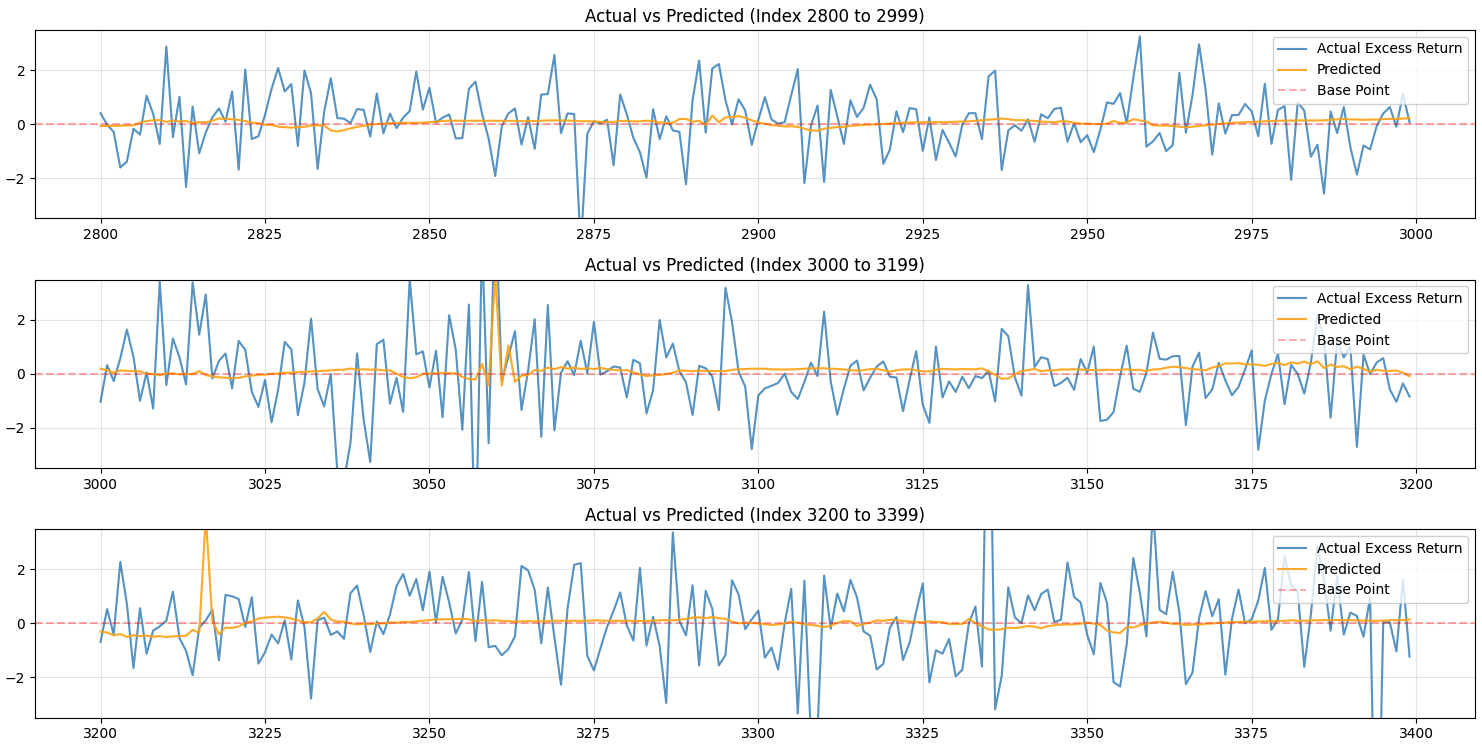

y_test_flat = y_test.flatten()

preds_flat = predictions.flatten()

comparison_df = pd.DataFrame({

'Actual': y_test_flat,

'Predicted': preds_flat

})

chunk_size = 200

y_min_limit = -3.5

y_max_limit = 3.5

total_len = len(comparison_df)

num_plots = int(np.ceil(total_len / chunk_size))

fig, axes = plt.subplots(num_plots, 1, figsize=(15, 2.5 * num_plots), sharex=False)

if num_plots == 1:

axes = [axes]

for i in range(num_plots):

start = i * chunk_size

end = min((i + 1) * chunk_size, total_len)

subset = comparison_df.iloc[start:end]

axes[i].plot(subset.index, subset['Actual'], label='Actual Excess Return', alpha=0.7)

axes[i].plot(subset.index, subset['Predicted'], label='Predicted', alpha=0.9, color='orange')

axes[i].set_ylim(y_min_limit, y_max_limit)

axes[i].axhline(base_point, label='Base Point', color='red', linestyle='--', alpha=0.3)

axes[i].set_title(f'Actual vs Predicted (Index {start} to {end-1})')

axes[i].legend(loc='upper right')

axes[i].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()This is how my model is performing right now:

Test set class distribution:

Class 0: 3198 samples

Class 1: 240 samples

Class 2: 3142 samples

Prediction set class distribution:

Class 0: 2137 samples

Class 1: 1868 samples

Class 2: 2575 samples

Classification Report:

precision recall f1-score support

Fall 0.49 0.32 0.39 3198

Neutral 0.04 0.28 0.06 240

Rise 0.47 0.38 0.42 3142

accuracy 0.35 6580

macro avg 0.33 0.33 0.29 6580

weighted avg 0.46 0.35 0.39 6580

It is hard to say that my model is performing well, but it some times predict the return movement fairly well.

Backtesting

Next I implemented backtesting to evaluate the model in more detail.

def get_backtest_data(ticker, period="2y", window_size=60):

df, feature_cols, target_col = get_dataset_columns(ticker, period=period, window_size=window_size)

data_x = df[feature_cols].values

data_y = df[target_col].values

data_open_close = df[["Open", "Close"]].values

X_list = []

y_real = []

dates_list = []

actual_opens_list = []

for i in range(len(df) - window_size):

window_x = data_x[i : i + window_size]

window_y = data_y[i + window_size]

if np.isnan(window_x).any() or np.isnan(window_y).any():

continue

window_x = normalize_window(window_x)

current_open = data_open_close[i + window_size]

X_list.append(window_x)

y_real.append(window_y)

dates_list.append(df.index[i + window_size])

actual_opens_list.append(current_open)

return np.array(X_list), np.array(y_real), dates_list, feature_cols, np.array(actual_opens_list)

def backtest(model, ticker, period="1y", window_size=60, initial_capital=10000):

X_bt, y_bt, bt_dates, feature_cols, data_open = get_backtest_data(ticker, period=period, window_size=window_size)

predictions = model.predict(X_bt, verbose=0).flatten()

previous_signal = "INIT"

previous_correct_signal = "INIT"

cash = initial_capital

cash_when_not_traded = initial_capital

cash_fixed = 0

shares = 0

threshold = 0.1

portfolio_history = []

buy_count = 0

buy_correct_count = 0

actual_buy_count = 0

sell_count = 0

sell_correct_count = 0

actual_sell_count = 0

hold_count = 0

hold_correct_count = 0

actual_hold_count = 0

correct_pred_count = 0

wrong_pred_count = 0

current_open_price = data_open[0][0]

shares_when_not_traded = cash_when_not_traded // current_open_price

cash_when_not_traded -= shares_when_not_traded * current_open_price

for i in range(len(bt_dates)):

current_open_price = data_open[i][0]

y_act = y_bt[i][0]

cash_when_not_traded = shares_when_not_traded * current_open_price

if y_act >= threshold:

correct_signal = "BUY"

actual_buy_count += 1

elif y_act <= -0.5 * threshold:

correct_signal = "SELL"

actual_sell_count += 1

else:

correct_signal ="HOLD"

actual_hold_count += 1

correct = False

if predictions[i] >= threshold:

signal = "BUY"

buy_count += 1

if correct_signal == "BUY":

correct = True

elif predictions[i] <= -1 * threshold:

signal = "SELL"

sell_count += 1

if correct_signal == "SELL":

correct = True

else:

signal ="HOLD"

hold_count += 1

if correct_signal == "HOLD":

correct = True

action = "HOLD" if signal == previous_signal else signal

previous_signal = previous_signal if signal == "HOLD" else signal

if signal=="BUY" and cash > current_open_price:

share_num = cash // current_open_price

cash -= share_num * current_open_price

shares += share_num

elif signal=="SELL" and shares > 0:

cash += shares * current_open_price

shares = 0

if cash > initial_capital:

rev = cash - initial_capital

cash -= rev

cash_fixed += rev

total_value = cash_fixed + cash + (shares * current_open_price)

if correct:

correct_pred_count += 1

if signal == "BUY":

buy_correct_count += 1

elif signal == "SELL":

sell_correct_count += 1

elif signal == "HOLD":

hold_correct_count += 1

else :

wrong_pred_count += 1

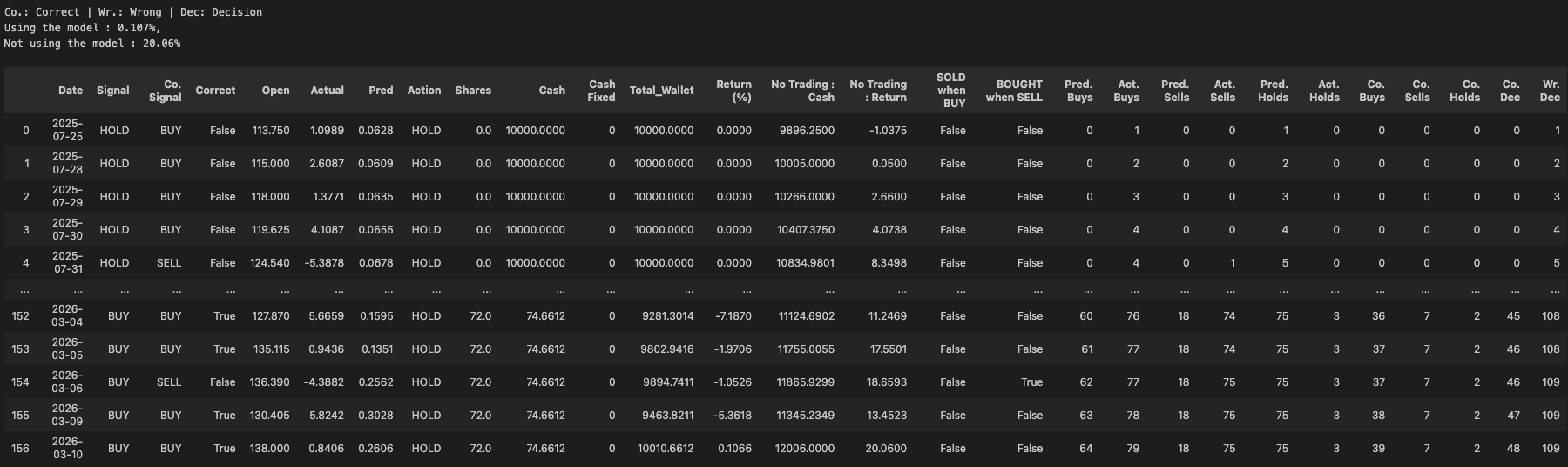

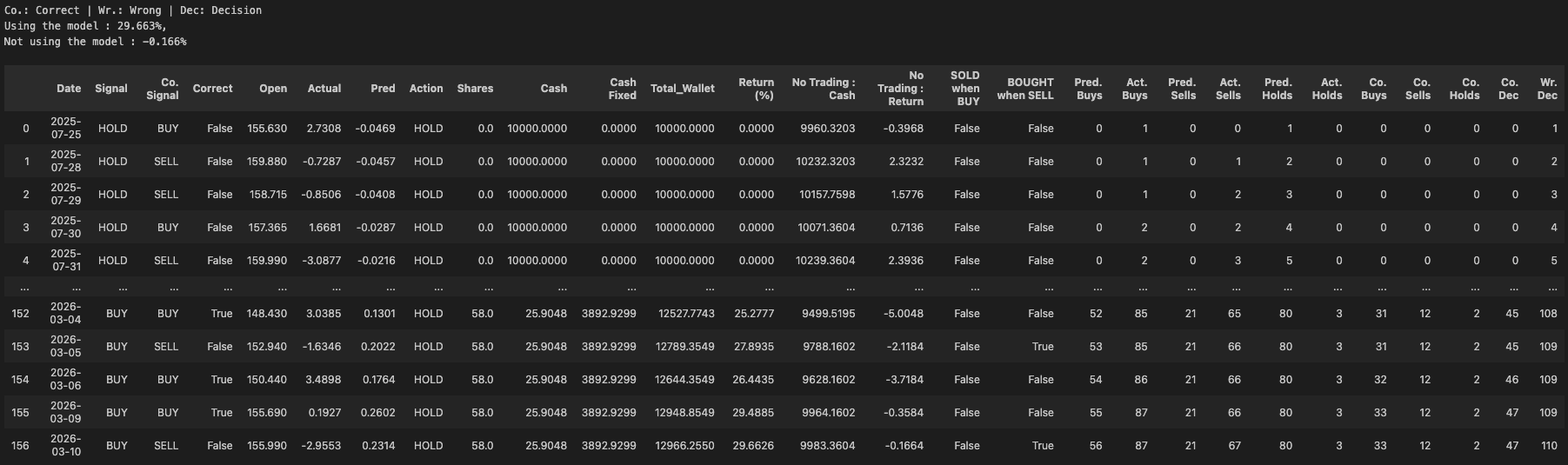

portfolio_history.append({

'Date': bt_dates[i],

'Signal': signal,

'Co. Signal': correct_signal,

'Correct': correct,

'Open': current_open_price,

'Actual': y_act,

'Pred': predictions[i],

'Action': action,

'Shares': shares,

'Cash': cash,

'Cash Fixed': cash_fixed,

'Total_Wallet': total_value,

'Return (%)': ((total_value - initial_capital) / initial_capital) * 100,

'No Trading : Cash': cash_when_not_traded,

'No Trading : Return': ((cash_when_not_traded - initial_capital) / initial_capital) * 100,

'SOLD when BUY':signal=="SELL" and correct_signal=="BUY",

'BOUGHT when SELL': signal=="BUY" and correct_signal=="SELL",

'Pred. Buys': buy_count,

'Act. Buys': actual_buy_count,

'Pred. Sells': sell_count,

'Act. Sells': actual_sell_count,

'Pred. Holds': hold_count,

'Act. Holds': actual_hold_count,

'Co. Buys': buy_correct_count,

'Co. Sells': sell_correct_count,

'Co. Holds': hold_correct_count,

'Co. Dec': correct_pred_count,

'Wr. Dec': wrong_pred_count,

})

result_df = pd.DataFrame(portfolio_history)

return result_df

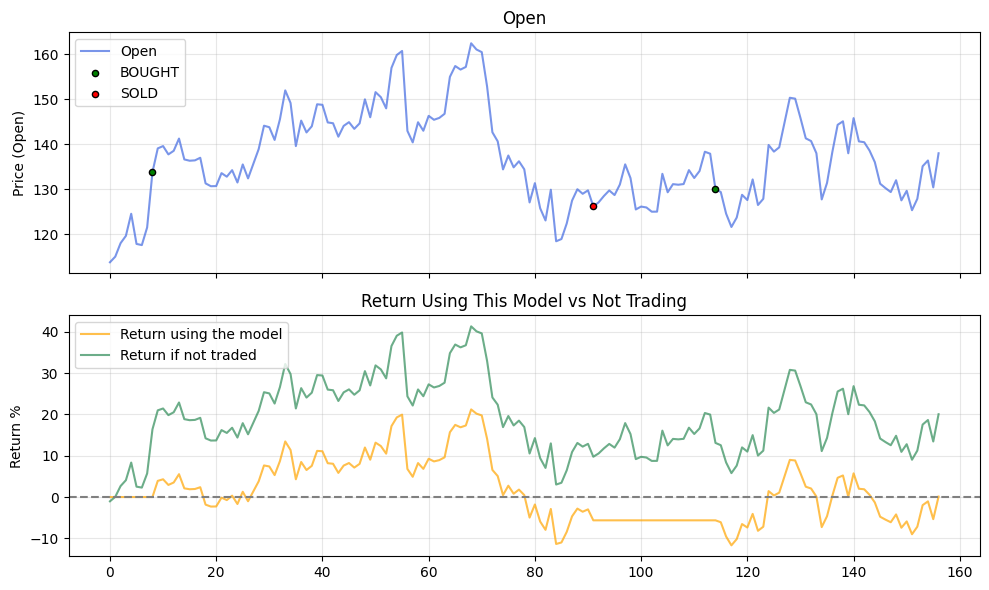

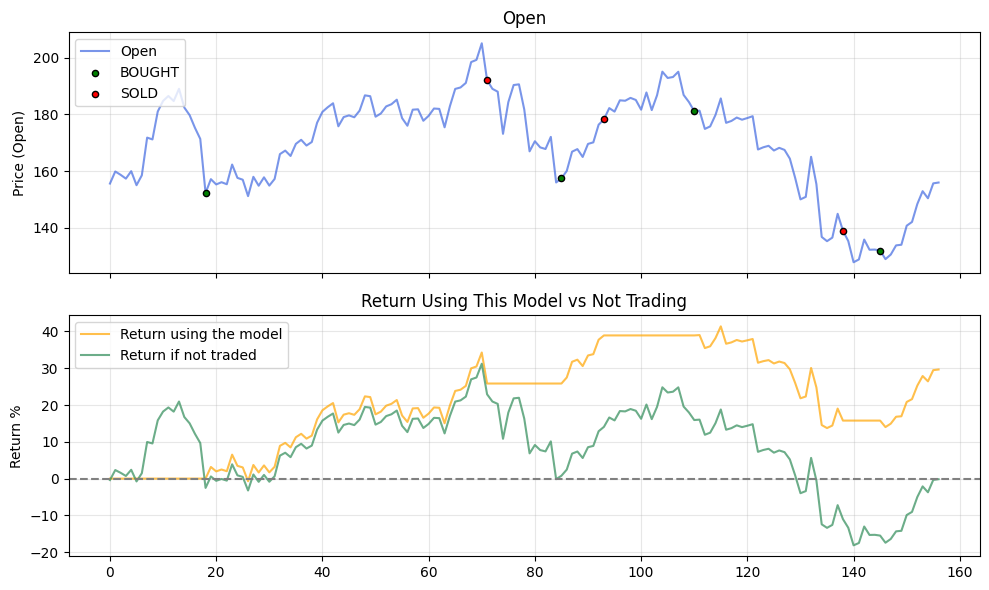

def plotBacktestResult(df, print_detail=False):

row_num = 5 if print_detail else 2

figsize = (10, 12) if print_detail else (10, 6)

fig, axs = plt.subplots(row_num, 1, figsize=figsize, sharex=True)

other_cols = ["Shares", "Cash", "Cash Fixed"]

other_colors = ["#DC143C", "#9370DB", "#4169E1"]

buy_signals = df[df['Action'] == 'BUY']

sell_signals = df[df['Action'] == 'SELL']

axs[0].plot(df.index, df['Open'], label='Open', color='#4169E1', alpha=0.7)

axs[0].scatter(buy_signals.index, buy_signals['Open'],

marker='o', color='green', s=20, label='BOUGHT', edgecolor='black', zorder=5)

axs[0].scatter(sell_signals.index, sell_signals['Open'],

marker='o', color='red', s=20, label='SOLD', edgecolor='black', zorder=5)

axs[0].set_ylabel('Price (Open)')

axs[0].set_title('Open')

axs[0].legend(loc='upper left')

axs[1].plot(df.index, df['Return (%)'], label='Return using the model', color='#FFA500', alpha=0.7)

axs[1].plot(df.index, df['No Trading : Return'], label='Return if not traded', color='#2E8B57', alpha=0.7)

axs[1].axhline(y=0, color='gray', linestyle='--', linewidth=1.5)

axs[1].set_ylabel('Return %')

axs[1].set_title('Return Using This Model vs Not Trading')

axs[1].legend(loc='upper left')

if (print_detail):

for i, col_name in enumerate(other_cols):

ax_idx = i + 2

axs[ax_idx].plot(df.index, df[col_name], label=col_name, color=other_colors[i])

axs[ax_idx].set_title(col_name)

axs[ax_idx].legend(loc='upper left')

for ax in axs:

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()I used about 68 more companies to evaluate the model.

When I tested the model with Arista Networks Inc, the model resulted in a smaller return value than not buying anything.

This is how the full result look like.

However, when I tested with Palantir, it resulted in a higher return.

From these results, I found out that the model’s performance relies more on the actual movement of the stock price rather than its choices.

When testing with all 68 companies, the model performed better than the buy-and-hold strategy only 35 of the time.

Future Improvements

- Finding a better trading strategy is essential, as I believe that it will provide a better insight for my model’s performance.