Let and be a precision matrix

Off-diagonal entry of

indicates the marginal dependence between the variables

indicates the conditional independence between the variables

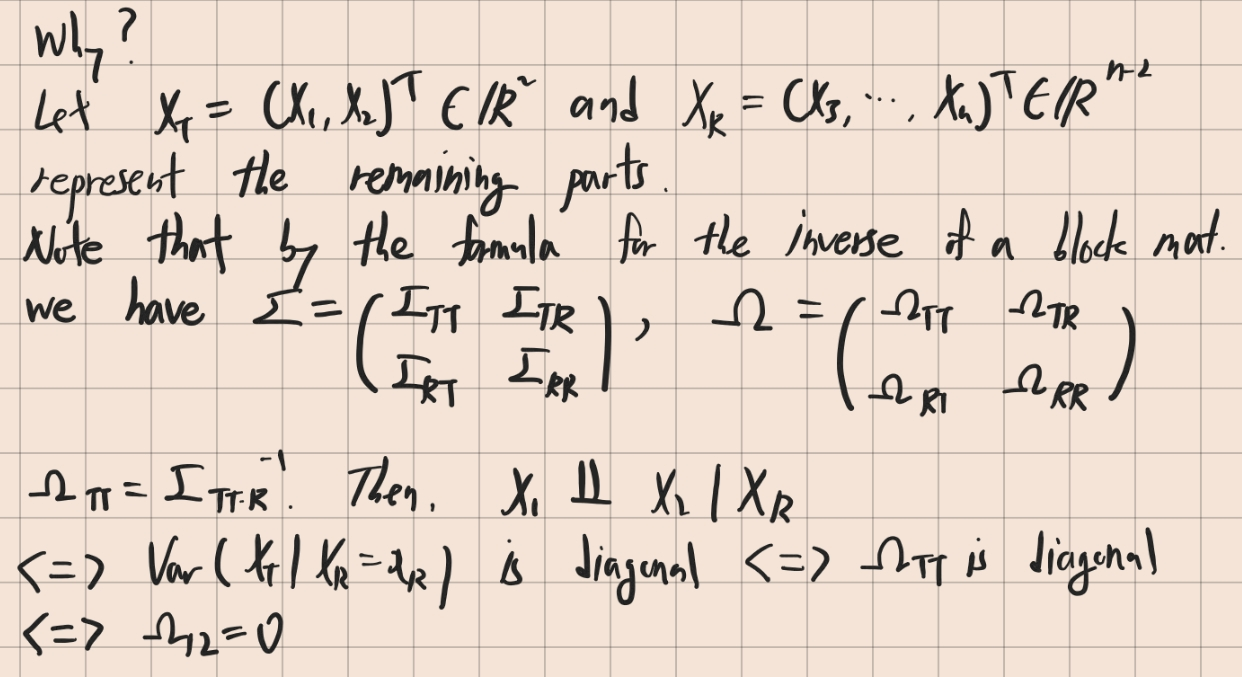

pf)

Let and be a precision matrix

Off-diagonal entry of

indicates the marginal dependence between the variables

indicates the conditional independence between the variables

pf)