개요

Kaggle에서 주관하는 2024 Kaggle Playground Series Season 4, Episode 1

https://www.kaggle.com/competitions/playground-series-s4e1?rvi=1

원본 데이터

Bank Customer Churn Prediction

목표

은행 고객 이탈 예측

이진 분류 문제

데이터 소개

Customer ID : 각 고객의 고유 식별자

Surname : 고객의 성

Credit Score : 고객의 신용 점수를 나타내는 값

Geography : 고객이 거주하는 국가(프랑스, 스페인 또는 독일)

Gender : 고객의 성별

Age : 고객의 연령

Tenure : 고객 은행 이용 기간(년)

Balance : 고객의 계좌 잔고

NumOfProducts : 고객이 사용하는 은행 상품 수(예: 저축 계좌, 신용 카드)

HasCrCard : 고객의 신용 카드 보유 여부(1 = 예, 0 = 아니오)

IsActiveMember : 고객 활동 여부(1 = 예, 0 = 아니오)

EstimatedSalary : 고객 추정 급여

Exited : 고객이 이탈 여부(1 = 예, 0 = 아니오)

Feature Engineering

def drop_useless(df):

df.drop(['id', 'CustomerId', 'Surname'], axis=1, inplace=True)

return df

drop_useless(train)

drop_useless(origin)

drop_useless(test)

# train과 원본 데이터 병합

train = pd.concat([train, origin], ignore_index=True)

# 중복 열 제거

train.drop_duplicates(inplace=True)

# 각 열의 최빈값(mode)을 구하고 이를 딕셔너리에 저장

mode_values_train = train.mode().iloc[0]

# 각 열의 결측치를 해당 열의 최빈값으로 대체

train.fillna(mode_values_train, inplace=True)

# test에 대해서 동일하게 적용

mode_values_test = test.mode().iloc[0]

test.fillna(mode_values_test, inplace=True)

# 수치형 데이터를 구분 후 각각의 변수에 저장

# train과 test 두 데이터에 대해 각각 적용

num_cols = list(train.select_dtypes(exclude=['object']).columns)

num_cols_test = list(test.select_dtypes(exclude=['object']).columns)

# Encoding이 필요하지 않은 경우 저장하지 않음

num_cols = [col for col in num_cols if col not in ['Exited', 'IsActiveMember', 'HasCrCard']]

num_cols_test = [col for col in num_cols_test if col not in ['Exited', 'IsActiveMember', 'HasCrCard']]

# Gender Encoding

labelencoder = LabelEncoder()

train['Gender']=labelencoder.fit_transform(train['Gender'])

test['Gender']=labelencoder.fit_transform(test['Gender'])

# Geography OneHotEncoding

train = pd.get_dummies(train, columns=['Geography'])

test = pd.get_dummies(test, columns=['Geography'])Standard Scaler 사용

# StandardScaler를 통해 수치형 데이터를 표준화

scaler = StandardScaler()

train[num_cols] = scaler.fit_transform(train[num_cols])

test[num_cols_test] = scaler.transform(test[num_cols_test])MinMax Scaler 사용

# MinMaxScaler 통해 수치형 데이터를 표준화

scaler = MinMaxScaler()

train[num_cols] = scaler.fit_transform(train[num_cols])

test[num_cols_test] = scaler.transform(test[num_cols_test])MinMax Scaler가 조금 더 높은 성능을 보임

Model Building

모델 선택

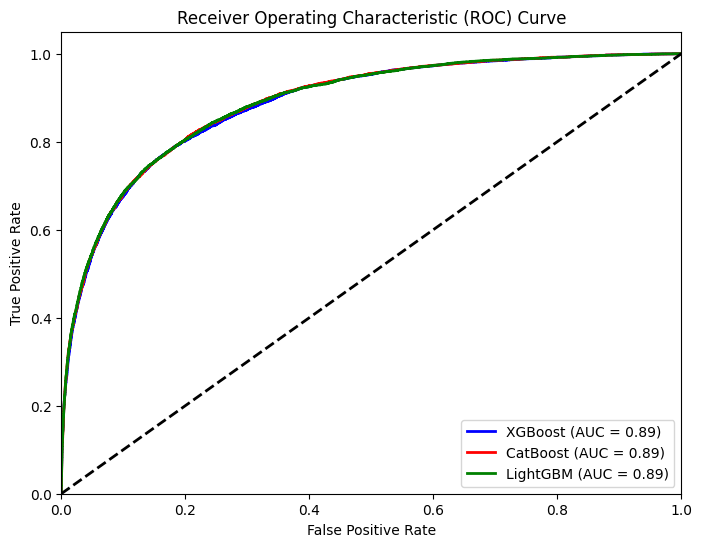

Catboost / XGBoost / LGBM 세 가지 모델 비교

ROC Curve

xgb = XGBClassifier()

cb = CatBoostClassifier()

lg = LGBMClassifier()

xgb.fit(X_train, y_train)

cb.fit(X_train, y_train)

lg.fit(X_train, y_train)

y_score_xgb = xgb.predict_proba(X_valid)[:, 1]

y_score_cb = cb.predict_proba(X_valid)[:, 1]

y_score_lg = lg.predict_proba(X_valid)[:, 1]

fpr_xgb, tpr_xgb, _ = roc_curve(y_valid, y_score_xgb)

roc_auc_xgb = auc(fpr_xgb, tpr_xgb)

fpr_cb, tpr_cb, _ = roc_curve(y_valid, y_score_cb)

roc_auc_cb = auc(fpr_cb, tpr_cb)

fpr_lg, tpr_lg, _ = roc_curve(y_valid, y_score_lg)

roc_auc_lg = auc(fpr_lg, tpr_lg)

plt.figure(figsize=(8, 6))

plt.plot(fpr_xgb, tpr_xgb, color='blue', lw=2, label='XGBoost (AUC = %0.2f)' % roc_auc_xgb)

plt.plot(fpr_cb, tpr_cb, color='red', lw=2, label='CatBoost (AUC = %0.2f)' % roc_auc_cb)

plt.plot(fpr_lg, tpr_lg, color='green', lw=2, label='LightGBM (AUC = %0.2f)' % roc_auc_lg)

plt.plot([0, 1], [0, 1], color='black', lw=2, linestyle='--')

plt.xlim([0.0, 1.0])

plt.ylim([0.0, 1.05])

plt.xlabel('False Positive Rate')

plt.ylabel('True Positive Rate')

plt.title('Receiver Operating Characteristic (ROC) Curve')

plt.legend(loc='lower right')

plt.show()

각 모델의 성능 차이는 매우 적게 나타남

제출을 통한 비교

4 - CatBoost

5 - XGBoost

6 - LGBM

LGBM이 가장 높은 결과를 보여줬기 때문에 LGBM으로 진행

1. predict를 통한 결과 확인

Grid Search를 통해 하이퍼파라미터 튜닝을 한 결과 미세하게 성능을 향상시킬 수 있었음

하지만 다른 사람들에 비해 낮은 정확도를 보였기 때문에 개선이 요구됨

2. predict_proba를 통한 결과 확인

예측을 하고 제출 할 때, 다른 사람들은 0과 1로만 제출하는 것이 아닌 .predict_proba() 값을 그대로 제출하는 것을 확인

위 방법 그대로 진행한 결과 약 10% 높은 결과를 확인할 수 있었음