Optuna

Optuna는 TPE(Tree-structured Parzen Estimator) 알고리즘을 적용하여 이전의 평가 결과를 기반으로 하이퍼파라미터의 새로운 조합을 제안하는 효율적인 하이퍼파라미터 최적화 프레임워크

- 기존의 랜덤 또는 격자(grid) 검색 방법보다 효율적으로 탐색 공간을 탐색

- 모델의 성능을 가장 잘 향상시킬 것으로 예상되는 하이퍼파라미터 조합에 더 많은 자원을 할당

- Optuna는 이러한 과정을 자동화하는 내부 wrapper class를 지원한다는 점에서 편리

여러 모델 튜닝용 코드

# !pip install optunaimport optuna

import lightgbm as lgb

from sklearn.linear_model import LogisticRegression

from sklearn.ensemble import RandomForestClassifier, GradientBoostingClassifier

from xgboost import XGBClassifier

from sklearn.neighbors import KNeighborsClassifier

from sklearn.svm import SVC

from sklearn.tree import DecisionTreeClassifier

from sklearn.metrics import accuracy_score, f1_score, precision_score, recall_score, roc_auc_score

from sklearn.model_selection import train_test_split

def objective(trial):

# 최적화할 모델 목록

classifier_name = trial.suggest_categorical("classifier", ["Random Forest", "XGBoost", "LightGBM"])

# Define hyperparameter search space based on the chosen model

if classifier_name == "Random Forest":

param = {

'n_estimators': trial.suggest_int('n_estimators', 50, 300),

'max_depth': trial.suggest_int('max_depth', 3, 20),

'min_samples_split': trial.suggest_int('min_samples_split', 2, 20),

'min_samples_leaf': trial.suggest_int('min_samples_leaf', 1, 10),

'random_state': 42

}

model = RandomForestClassifier(**param)

elif classifier_name == "XGBoost":

param = {

'objective': 'binary:logistic',

'eval_metric': 'logloss',

'n_estimators': trial.suggest_int('n_estimators', 50, 300),

'learning_rate': trial.suggest_loguniform('learning_rate', 1e-4, 1e-1),

'max_depth': trial.suggest_int('max_depth', 3, 9),

'subsample': trial.suggest_uniform('subsample', 0.4, 1.0),

'colsample_bytree': trial.suggest_uniform('colsample_bytree', 0.4, 1.0),

'random_state': 42,

'use_label_encoder': False

}

model = XGBClassifier(**param)

elif classifier_name == "LightGBM":

param = {

'objective': 'binary',

'metric': 'binary_logloss',

'verbosity': -1,

'boosting_type': 'gbdt',

'num_leaves': trial.suggest_int('num_leaves', 20, 100),

'max_depth': trial.suggest_int('max_depth', 3, 9),

'learning_rate': trial.suggest_loguniform('learning_rate', 1e-4, 1e-1),

'n_estimators': trial.suggest_int('n_estimators', 50, 300),

'min_child_samples': trial.suggest_int('min_child_samples', 5, 100),

'feature_fraction': trial.suggest_uniform('feature_fraction', 0.4, 1.0),

'bagging_fraction': trial.suggest_uniform('bagging_fraction', 0.4, 1.0),

'bagging_freq': trial.suggest_int('bagging_freq', 1, 7),

'reg_alpha': trial.suggest_loguniform('reg_alpha', 1e-8, 10.0),

'reg_lambda': trial.suggest_loguniform('reg_lambda', 1e-8, 10.0),

'random_state': 42

}

model = lgb.LGBMClassifier(**param)

# 다른 모델 추가하고 싶으면 하단에 elif 분기로 추기

# Model training and evaluation

# Optuna는 train-validation을 학습시킨 뒤 각 조합에서 어떻게 결과가 나왔는지, best trial은 무엇인지에 대한 것.

# CrossValidation를 수행하기 위해선 OptunaSearchCV wrapper를 활용할 수 있음

# from optuna.integration import OptunaSearchCV

# 사용자가 직접 지정한 train-validation split

model.fit(X_train, y_train)

y_pred = model.predict(X_valid)

# 1.성능 지표 계산

f1 = f1_score(y_valid, y_pred)

precision = precision_score(y_valid, y_pred)

recall = recall_score(y_valid, y_pred)

roc_auc = roc_auc_score(y_valid, y_pred)

accuracy = accuracy_score(y_valid, y_pred)

# 2. 최종적으로 가장 최적화하고 싶은 것을 return

return accuracy

#return accuracy, roc_auc

study = optuna.create_study(direction='maximize')

# objective 함수 구성에 따라 다르게 study 설정 가능

# study = optuna.create_study(directions=['maximize', 'maximize'])

study.optimize(objective, n_trials=10)

print('Number of finished trials:', len(study.trials))

print('Best trial:', study.best_trial.params)

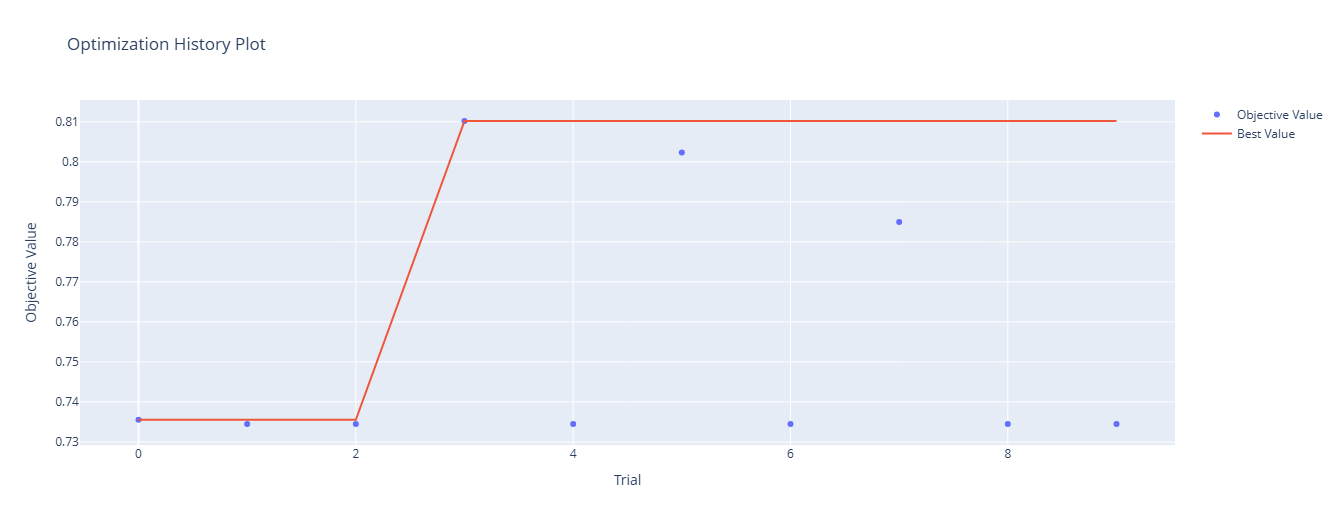

print('Best accuracy:', study.best_value)- 결과

Number of finished trials: 10

Best trial: {'classifier': 'LightGBM', 'num_leaves': 28, 'max_depth': 5, 'learning_rate': 0.040654569686204275, 'n_estimators': 151, 'min_child_samples': 72, 'feature_fraction': 0.7663710558769723, 'bagging_fraction': 0.5588317156910854, 'bagging_freq': 1, 'reg_alpha': 0.0003681518033200165, 'reg_lambda': 3.7016272682914537}

Best accuracy: 0.8101997896950578# Multi-objective 문제를 푸는 경우 study.best_trials로서 접근가능

study.best_trials[0]# Optuna 시각화

from optuna.visualization import plot_optimization_history, plot_param_importances

# 최적화 과정 시각화

plot_optimization_history(study)

Best param 조합으로 훈련

# 모델 훈련을 위한 est_params 불러오기

best_params = study.best_params

# 가장 좋은 알고리즘은 무엇이었는지

best_model_name = best_params.pop('classifier')

# 훈련 진행

# Add other model initializations here if needed based on best_model_name

if best_model_name == "Random Forest":

best_model = RandomForestClassifier(**best_params, random_state=42)

elif best_model_name == "XGBoost":

best_model = XGBClassifier(**best_params, random_state=42)

elif best_model_name == "LightGBM":

best_model = LGBMClassifier(**best_params, random_state=42)

best_model.fit(X_train, y_train)

# 3) Valid Set 성능 확인

val_preds = best_model.predict(X_valid)

val_accuracy = accuracy_score(y_valid, val_preds)

val_f1 = f1_score(y_valid, val_preds)

val_precision = precision_score(y_valid, val_preds)

val_recall = recall_score(y_valid, val_preds)

val_roc_auc = roc_auc_score(y_valid, val_preds)

print("Final validation accuracy with best model: ", val_accuracy)

print("Final validation f1 with best model: ", val_f1)

print("Final validation precision with best model: ", val_precision)

print("Final validation recall with best model: ", val_recall)

print("Final validation roc_auc with best model: ", val_roc_auc)- 결과

Final validation accuracy with best model: 0.8101997896950578

Final validation f1 with best model: 0.6002214839424141

Final validation precision with best model: 0.6809045226130653

Final validation recall with best model: 0.5366336633663367

Final validation roc_auc with best model: 0.7228622862286229모델 성능 지표 의미 및 해석

-

Accuracy (0.808)

- 의미: 전체 데이터 중 모델이 맞춘 비율

- 장점: 직관적, 전체적인 성능 파악 가능

- 단점: 클래스 불균형에 취약

- 비즈니스 해석: 고객 이탈 예측과 같이 불균형 데이터에서는 단순 참고용. 높은 정확도가 실제로 중요한 고객을 잘 잡는다는 의미는 아님

-

Precision (0.674)

- 의미: 모델이 긍정(예: 이탈)으로 예측한 고객 중 실제로 맞는 비율

- 중요 비즈니스 상황:

- 마케팅/프로모션 비용이 제한적일 때

- 예: 비용이 높은 프로모션은 실제 이탈 가능성이 높은 고객만 선택

-

Recall (0.537)

- 의미: 실제 긍정 고객 중 모델이 잡아낸 비율

- 중요 비즈니스 상황:

- 놓치는 고객이 큰 손실로 이어질 때

- 예: 고객 이탈을 막는 것이 수익에 직결 → 가능한 많은 이탈 고객 포착 필요

-

F1 Score (0.598)

- 의미: Precision과 Recall의 조화 평균 → 불균형 데이터에서 균형 잡힌 성능 평가

-

ROC-AUC (0.72)

- 의미: 전체 클래스 구분 능력, threshold에 상관없이 모델 성능 평가

- 비즈니스 해석: 전체 고객군을 대상으로 모델이 얼마나 잘 이탈/비이탈을 구분하는지 평가.

현재 성능 기반 개선 방향성 탐구

- 제한된 마케팅 자원을 가진 상황 → Precision 우선: 낭비 최소화

- 이탈 고객 수를 최대한 막고 싶다면 → Recall 개선 필요

- F1 Score → Precision/Recall 균형 확인

- ROC-AUC → 전체 모델 신뢰도 평가, threshold 조정 시 성능 최적화 가능

모델 해석

Feature Importance

-

의미: 모델이 예측을 할 때, 각 입력 피처가 결과에 얼마나 영향을 주는지를 보고자하는 지표

-

용도:

- 모델 해석 가능성 확보

- 중요한 피처를 식별하여 데이터 전처리/선별 (e.g. Baseline을 fitting 시키고 -> 피쳐 중요도 TOP10만 사용하는 방식 등을 활용할 수 있음)

if hasattr(best_model, 'coef_'):

feature_importances = pd.Series(best_model.coef_[0], index=X_train.columns)

title = "Feature Importances (Coefficients)"

elif hasattr(best_model, 'feature_importances_'):

# feature importance의 경우 tree 기반 모형에 attribute로 저장됨

feature_importances = pd.Series(best_model.feature_importances_, index=X_train.columns)

title = "Feature Importances"

else:

feature_importances = None

print("Feature importances are not available for this model type.")

if feature_importances is not None:

# Sort importances and select top N (e.g., top 20)

top_n = 20

top_feature_importances = feature_importances.nlargest(top_n)

plt.figure(figsize=(10, 6))

top_feature_importances.plot(kind='barh')

plt.title(title)

plt.xlabel("Importance")

plt.ylabel("Feature")

plt.gca().invert_yaxis() # Display most important at the top

plt.show()SHAP

- 의미: 게임 이론 기반으로 각 피처가 예측값에 기여한 정도를 정량화

- 특징:

- 전역(Global) 해석: 전체 모델에서 피처 영향 확인

- 국소(Local) 해석: 특정 샘플 예측에 대한 피처 기여 확인

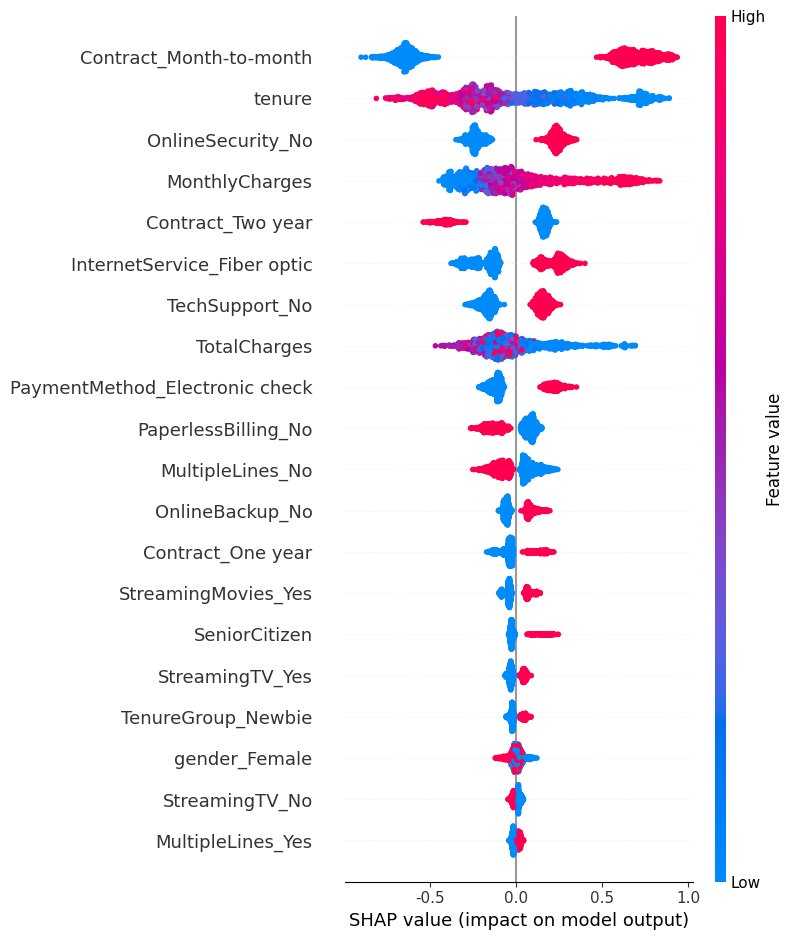

- 하위 플롯 종류:

- Summary Plot

- 모든 피처의 영향도와 분포 시각화

- 색상: 피처 값 크기 (high/low)

- Dependence Plot

- 특정 피처 값 변화에 따른 SHAP 값 변동

- 다른 피처와 상호작용 관계 확인 가능

- Force Plot

- 단일 예측에 대한 피처 기여 시각화

- 예측값이 baseline에서 어떻게 이동했는지 보여줌

- Bar Plot

- 각 피처 평균 절댓값 SHAP 값 기준 중요도 표시

- Summary Plot

import shap

# SHAPExplainer 생성

if isinstance(best_model, (XGBClassifier, LGBMClassifier, RandomForestClassifier)):

explainer = shap.TreeExplainer(best_model)

elif isinstance(best_model, LogisticRegression):

explainer = shap.LinearExplainer(best_model, X_train)

shap_values = explainer.shap_values(X_valid)

print("SHAP values calculated.")

print("Shape of shap_values:", [s.shape for s in shap_values] if isinstance(shap_values, list) else shap_values.shape)- 결과

SHAP values calculated.

Shape of shap_values: (1902, 7094)# SHAP summary plot 시각화

if isinstance(best_model, (XGBClassifier, LGBMClassifier, RandomForestClassifier)):

# TreeExplainer의 경우 shap_values는 리스트 형태 (클래스별)

# 보통 이진 분류에서는 클래스 1에 대한 SHAP 값 사용함

if isinstance(shap_values, list):

shap.summary_plot(shap_values[1], X_valid, feature_names=X_valid.columns)

else:

shap.summary_plot(shap_values, X_valid, feature_names=X_valid.columns)

elif isinstance(best_model, LogisticRegression):

if isinstance(shap_values, list):

shap.summary_plot(shap_values[1], X_valid, feature_names=X_valid.columns)

else:

shap.summary_plot(shap_values, X_valid, feature_names=X_valid.columns)

SHAP Summary Plot 해석 방법

- 각 점: 실제 데이터 포인트

-

X축 (SHAP value)

- 피처가 예측 결과에 미치는 영향의 크기와 방향

- 양수(+): 예측을 1(positive) 방향으로 밀어줌

- 음수(−): 예측을 0(negative) 방향으로 밀어줌

-

Y축 (Feature)

- 피처 이름

- 위쪽에 있을수록 모델 전체에서 영향력이 큰 피처

-

점 색상 (Feature 값 크기)

- 빨강(High): 피처 값이 큼

- 파랑(Low): 피처 값이 작음

모델 피쳐 해석

-

가장 영향력 큰 피처:

Contract_Month-to-month: 값이 높을수록(빨간 점) 이탈 가능성을 높임 (SHAP 양수 방향)tenure: 값이 높을수록(빨간 점) SHAP 음수 방향 → 장기 고객일수록 이탈 가능성 낮음MonthlyCharges: 값이 높을수록(빨간 점) 이탈 가능성 증가OnlineSecurity_No,TechSupport_No: 서비스 부재(1)일수록 이탈 가능성 증가

-

인사이트 도출:

- Contract 타입: Month-to-month 계약 고객은 이탈 가능성이 높고, 2년 계약은 낮음

- 서비스 관련 피처: 온라인 보안/기술 지원 없으면 이탈 확률 상승

- tenure(가입 기간): 오래 가입할수록 이탈 가능성 낮음

- 요금 관련(MonthlyCharges): 요금이 높으면 이탈 확률 상승

-

비즈니스 인사이트:

- 단기 계약 고객, 고요금, 서비스 미가입 고객에게 맞춤형 유지 전략 필요

tenure와 결합하면 장기 고객 유지를 위한 보상 정책 설계 가능

Analyse the world