여러 모델을 구현하고 튜닝하면서 문법적인 실력이 많이 늘었다. 아직 부족한 게 많은 건 사실이지만, 그래도 이제 머신러닝의 전반적인 진행 순서가 머릿속에 그려진다. 불과 3주 만에 다른 사람이 된 것 같다.

학습시간 09:00~02:00(당일17H/누적278H)

◆ 오늘의 깨달음

- 그리드 서치 시

estimator=XGBClassifier부분에estimator=는 안 적어도 된다.

search = GridSearchCV(

XGBClassifier(

use_label_encoder=False,

eval_metric='logloss',

random_state=42

),

param_grid=params,

scoring='recall',

cv=3,

verbose=1,

n_jobs=-1

).fit(X_train, y_train)- 그리드 서치로 나온 튜닝값을

**변수명.best_params_로 모델 안에 넣어주면 자동으로 언패킹된다. 완전 꿀팁이다.

m_xgb = XGBClassifier(

**search.best_params_,

random_state=42

).fit(X_train, y_train)- 모델의 verbose와 그리드 서치의 verbose는 넣는 숫자가 다르다!! 명심!!!

LGBMClassifier(verbose=-1) 경고 메시지 숨김

GridSearchCV(verbose=1) 진행 메시지 숨김classification_report안에 정확도가 있어서 따로accuracy_score지표를 호출할 필요가 없다.

◆ 학습내용

예금 가입자 예측 모델 구현 2탄

3. 모델 구현

어제에 이어서

어제 df를 2개로 나누는 것까지 했다. df_encoded는 원핫인코딩, df_cat는 카테고리화한 df다. CatBoost랑 LightGBM에는 카테고리 타입을 자동으로 변환하는 기능이 있다고 하는데, 과연 어떤 차이가 있을지 궁금하다.

어제 df를 2개로 나누는 것까지 했다. df_encoded는 원핫인코딩, df_cat는 카테고리화한 df다. CatBoost랑 LightGBM에는 카테고리 타입을 자동으로 변환하는 기능이 있다고 하는데, 과연 어떤 차이가 있을지 궁금하다.

X = df_encoded.drop(columns=['y'])

y = df_encoded['y']일단 이녀석부터 시작해 보자! 결정트리와 앙상블기법을 사용하라고 했으니, 일단 결정트리부터 해봐야겠다. 근데 모델 이름만 보았을 때 랜덤포레스트나 캣부스트가 성능이 좋을 것 같다. 아마도...?

(1) Decision Tree

''' 모델 구현 '''

# 결정트리

from sklearn.model_selection import train_test_split

X = df_encoded.drop(columns=['y'])

y = df_encoded['y']

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42)

from sklearn.tree import DecisionTreeClassifier

m_dtree = DecisionTreeClassifier(

criterion = 'gini',

min_samples_split = 3,

min_samples_leaf = 3,

max_features = None,

max_depth = 5,

max_leaf_nodes = None,

random_state = 42

).fit(X_train, y_train)

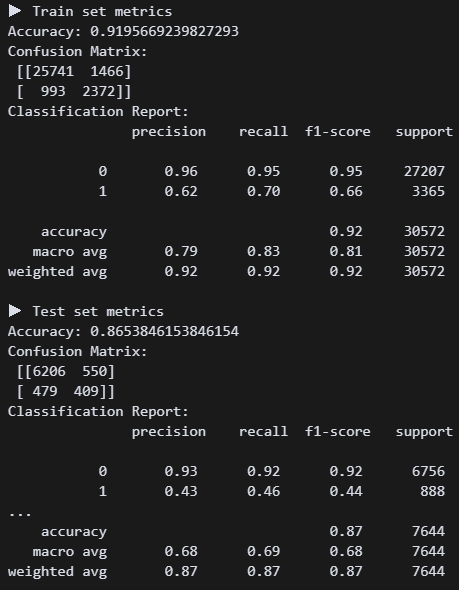

y_train_pred = m_dtree.predict(X_train)

y_test_pred = m_dtree.predict(X_test)

from sklearn.metrics import accuracy_score, confusion_matrix, classification_report

print("▶ Train set metrics")

print("Accuracy:", accuracy_score(y_train, y_train_pred))

print("Confusion Matrix:\n", confusion_matrix(y_train, y_train_pred))

print("Classification Report:\n", classification_report(y_train, y_train_pred))

print("▶ Test set metrics")

print("Accuracy:", accuracy_score(y_test, y_test_pred))

print("Confusion Matrix:\n", confusion_matrix(y_test, y_test_pred))

print("Classification Report:\n", classification_report(y_test, y_test_pred))

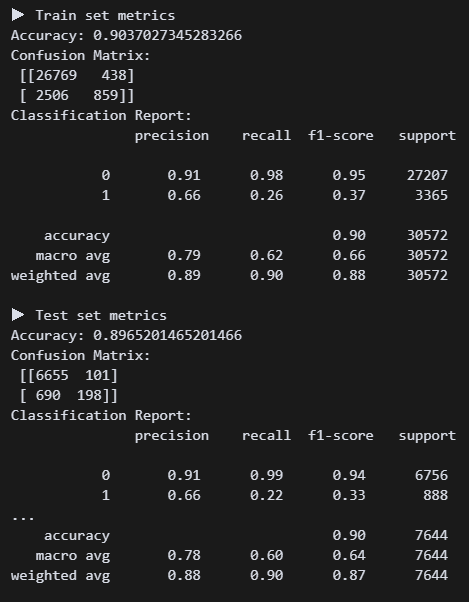

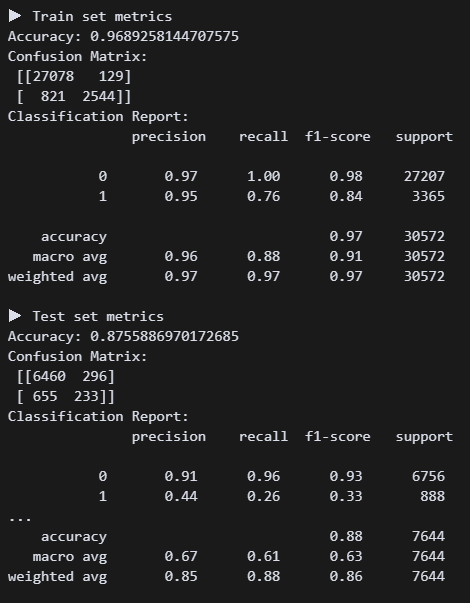

결정트리 모델 구현 결과. 정확도는 괜찮은데 가입자를 못 맞추고 있다. 리콜 점수가 0.22다 ㅠㅠ 튜닝하면 괜찮아지려나?

결정트리 모델 구현 결과. 정확도는 괜찮은데 가입자를 못 맞추고 있다. 리콜 점수가 0.22다 ㅠㅠ 튜닝하면 괜찮아지려나?

from sklearn.model_selection import GridSearchCV

param_grid = {

'max_depth': [3, 5, 7],

'min_samples_split': [5, 10],

'min_samples_leaf': [2, 5],

'class_weight': [None, 'balanced']

}

grid = GridSearchCV(

DecisionTreeClassifier(random_state=42),

param_grid,

scoring='recall',

cv=5

).fit(X_train, y_train)

print("Best params:", grid.best_params_)

print("Best score:", grid.best_score_) 튜닝 결과가 나왔다.

튜닝 결과가 나왔다.

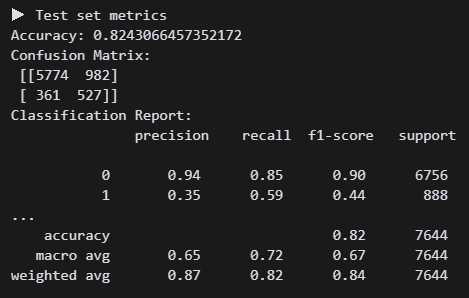

m_dtree = DecisionTreeClassifier(

class_weight = 'balanced',

criterion = 'gini',

min_samples_split = 5,

min_samples_leaf = 5,

max_features = None,

max_depth = 5,

max_leaf_nodes = None,

random_state = 42

).fit(X_train, y_train)바로 반영!

오! 튜닝하니 리콜점수가 0.58로 올랐다. 정확도는 조금 낮아졌지만, 그래도 미가입자보다 가입자를 잡는 게 더 우선 아닐까?

오! 튜닝하니 리콜점수가 0.58로 올랐다. 정확도는 조금 낮아졌지만, 그래도 미가입자보다 가입자를 잡는 게 더 우선 아닐까?

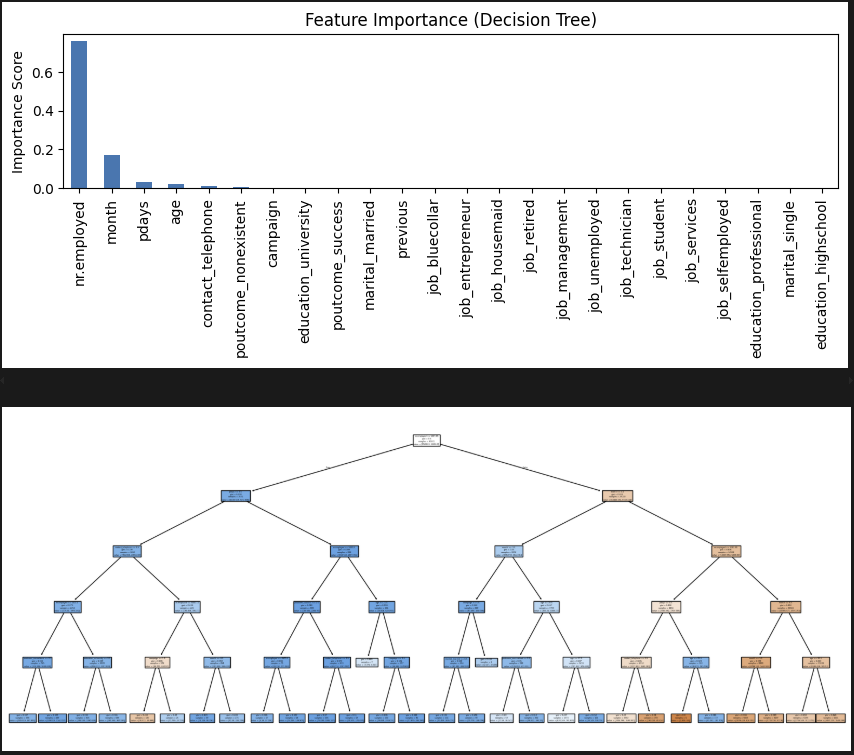

# 시각화

import matplotlib.pyplot as plt

importances = m_dtree.feature_importances_

feat_series = pd.Series(importances, index=X.columns).sort_values(ascending=False)

plt.figure(figsize=(10, 2))

feat_series.plot(kind='bar')

plt.title('Feature Importance (Decision Tree)')

plt.ylabel('Importance Score')

plt.show()

from sklearn.tree import plot_tree

plt.figure(figsize=(20, 8))

plot_tree(m_dtree, filled=True, feature_names=X.columns)

plt.show()어떤 요소를 기준으로 보았는지 확인해 보자!

고용률이 엄청 영향이 크다. 직업은 생각보다 의미가 없네.

고용률이 엄청 영향이 크다. 직업은 생각보다 의미가 없네.

(2) Voting

# 모델 구현

from sklearn.ensemble import VotingClassifier

from sklearn.linear_model import LogisticRegression

from sklearn.tree import DecisionTreeClassifier

from sklearn.ensemble import RandomForestClassifier

m_v1logr = LogisticRegression(max_iter=1000, class_weight='balanced', random_state=42)

m_v2tree = DecisionTreeClassifier(max_depth=5, class_weight='balanced', random_state=42)

m_v3forest = RandomForestClassifier(n_estimators=100, class_weight='balanced', random_state=42)

m_voting = VotingClassifier(

estimators = [

('LOGR', m_v1logr),

('TREE', m_v2tree),

('FOREST', m_v3forest)

],voting = 'soft'

).fit(X_train, y_train)

y_train_pred = m_voting.predict(X_train)

y_test_pred = m_voting.predict(X_test)

from sklearn.metrics import accuracy_score, confusion_matrix, classification_report

print("▶ Train set metrics")

print("Accuracy:", accuracy_score(y_train, y_train_pred))

print("Confusion Matrix:\n", confusion_matrix(y_train, y_train_pred))

print("Classification Report:\n", classification_report(y_train, y_train_pred))

print("▶ Test set metrics")

print("Accuracy:", accuracy_score(y_test, y_test_pred))

print("Confusion Matrix:\n", confusion_matrix(y_test, y_test_pred))

print("Classification Report:\n", classification_report(y_test, y_test_pred))보팅 모델을 구현했다. logr+tree+forest가 대표적인 조합이라고 한다.

튜닝 전인데 리콜점수가 결정트리보다 좋다. 튜닝 3개를 언제 하지 ㅠㅠ

튜닝 전인데 리콜점수가 결정트리보다 좋다. 튜닝 3개를 언제 하지 ㅠㅠ

# 튜닝(LogisticRegression)

from sklearn.model_selection import GridSearchCV

param_grid_logr = {

'C': [0.01, 0.1, 1, 10],

'penalty': ['l2'],

'class_weight': ['balanced']

}

grid_logr = GridSearchCV(

LogisticRegression(max_iter=1000, solver='lbfgs', random_state=42),

param_grid_logr,

scoring='recall',

cv=3, verbose=0, n_jobs=-1

).fit(X_train, y_train)

print("Best LogisticRegression:", grid_logr.best_params_)

# 튜닝(DecisionTreeClassifier)

param_grid_tree = {

'max_depth': [3, 5, 7],

'min_samples_leaf': [1, 5, 10],

'class_weight': ['balanced']

}

grid_tree = GridSearchCV(

DecisionTreeClassifier(random_state=42),

param_grid_tree,

scoring='recall',

cv=3, verbose=0, n_jobs=-1

).fit(X_train, y_train)

print("Best DecisionTree:", grid_tree.best_params_)

# 튜닝(RandomForestClassifier)

param_grid_forest = {

'n_estimators': [100, 200],

'max_depth': [5, 10, None],

'max_features': ['sqrt', 'log2'],

'class_weight': ['balanced']

}

grid_forest = GridSearchCV(

RandomForestClassifier(random_state=42),

param_grid_forest,

scoring='recall',

cv=3, verbose=0, n_jobs=-1

).fit(X_train, y_train)

print("Best RandomForest:", grid_forest.best_params_)헉헉,,, 이렇게 하면 되는 건가...

일단 최적의 조합이 나온 것 같다. 이대로 해보자.

일단 최적의 조합이 나온 것 같다. 이대로 해보자.

m_v1logr = LogisticRegression(

C=0.01,

class_weight='balanced',

penalty=12,

random_state=42

)

m_v2tree = DecisionTreeClassifier(

class_weight='balanced',

max_depth=5,

min_samples_leaf=10,

random_state=42

)

m_v3forest = RandomForestClassifier(

class_weight='balanced',

max_depth=5,

max_features='sqrt'

n_estimators=200,

random_state=42

)제발!!!

오 0.59가 나왔다. 근데 결정트리랑 큰 차이가 없네.

오 0.59가 나왔다. 근데 결정트리랑 큰 차이가 없네.

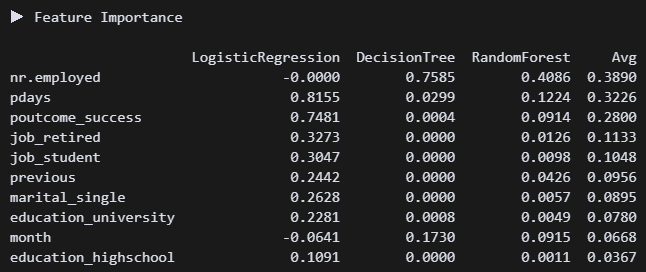

# 차트화

import pandas as pd

m_v1logr.fit(X_train, y_train)

m_v2tree.fit(X_train, y_train)

m_v3forest.fit(X_train, y_train)

logr_importance = pd.Series(m_v1logr.coef_[0], index=X.columns)

tree_importance = pd.Series(m_v2tree.feature_importances_, index=X.columns)

forest_importance = pd.Series(m_v3forest.feature_importances_, index=X.columns)

importance_df = pd.DataFrame({

'LogisticRegression': logr_importance,

'DecisionTree': tree_importance,

'RandomForest': forest_importance

})

importance_df['Avg'] = importance_df.mean(axis=1)

importance_df = importance_df.sort_values(by='Avg', ascending=False).head(10)

print("\n▶ Feature Importance \n")

print(importance_df.round(4))3개 모델 중요도를 차트로 만들어봤다.

고용률, 연락한 적 있는 사람, 은퇴자, 학생이 영향이 큰 것으로 보인다.

고용률, 연락한 적 있는 사람, 은퇴자, 학생이 영향이 큰 것으로 보인다.

(2) Begging

''' Bagging '''

# 모델 구현

from sklearn.ensemble import RandomForestClassifier

m_forest = RandomForestClassifier(

random_state=42,

n_jobs=-1

).fit(X_train, y_train)

y_train_pred = m_forest.predict(X_train)

y_test_pred = m_forest.predict(X_test)

# 평가

print_metrics()배깅의 대표모델 랜덤포레스트로 간다!(사실 다른 모델 모름)

튜닝 성능좀 보려고 하이퍼 파라미터를 아무것도 안 넣었다. 리콜수치가 0.26이다.

튜닝 성능좀 보려고 하이퍼 파라미터를 아무것도 안 넣었다. 리콜수치가 0.26이다.

# 튜닝

from sklearn.model_selection import RandomizedSearchCV

params = {

'n_estimators': [100, 200, 300],

'max_depth': [5, 10, 20, None],

'min_samples_split': [2, 5, 10],

'min_samples_leaf': [1, 3, 5],

'max_features': ['sqrt', 'log2'],

'class_weight': ['balanced'],

'bootstrap': [True, False]

}

search = RandomizedSearchCV(

RandomForestClassifier(random_state=42, n_jobs=-1),

param_distributions=params,

n_iter=30,

scoring='recall',

cv=3,

verbose=1,

random_state=42,

n_jobs=-1

).fit(X_train, y_train)

print("Best RandomForestClassifier:", search.best_params_)

그리드서치 20분 넘게 걸려서 랜덤서치로 변경했다. 나온 값을 넣어보자!

그리드서치 20분 넘게 걸려서 랜덤서치로 변경했다. 나온 값을 넣어보자!

# 모델 구현

from sklearn.ensemble import RandomForestClassifier

m_forest = RandomForestClassifier(

bootstrap=False,

class_weight='balanced',

max_features='log2',

min_samples_leaf=5,

min_samples_split=5,

n_jobs=-1,

random_state=42

).fit(X_train, y_train)

y_train_pred = m_forest.predict(X_train)

y_test_pred = m_forest.predict(X_test)과연!?

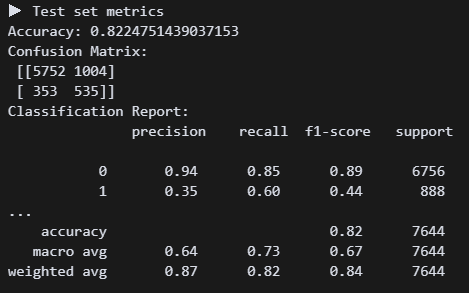

와우! 정확도는 약간 떨어졌지만 리콜이 0.6으로 올라갔다.

와우! 정확도는 약간 떨어졌지만 리콜이 0.6으로 올라갔다.

# 시각화

importances = m_forest.feature_importances_

feat_series = pd.Series(importances, index=X.columns).sort_values(ascending=False)

plt.figure(figsize=(10, 5))

feat_series.head(10).sort_values().plot(kind='barh')

plt.title('Top 10 Feature Importance (Random Forest)')

plt.xlabel('Importance Score')

plt.tight_layout()

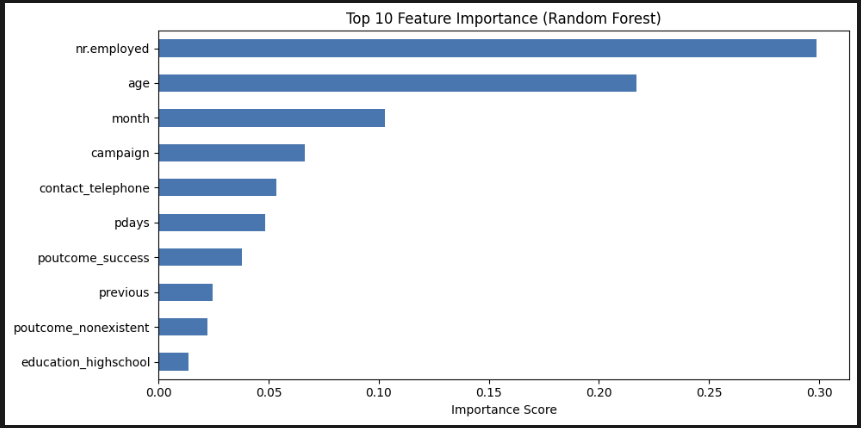

plt.show() 중요도 상위 10개를 봤다. 고용률, 나이, 월 순서로 중요하다. 트리도 보고 싶긴 한데, 결정 트리처럼 하나만 있는 게 아니라 모든 트리를 한 번에 볼 수 없다고 한다. 아쉽다.

중요도 상위 10개를 봤다. 고용률, 나이, 월 순서로 중요하다. 트리도 보고 싶긴 한데, 결정 트리처럼 하나만 있는 게 아니라 모든 트리를 한 번에 볼 수 없다고 한다. 아쉽다.

# 임계값 조정

from sklearn.metrics import confusion_matrix

from sklearn.metrics import classification_report

y_proba_forest = m_forest.predict_proba(X_test)[:, 1]

threshold = 0.4

y_pred_custom = (y_proba_forest >= threshold).astype(int)

print(f"▶ RandomForest Threshold {threshold} Evaluation")

print("Confusion Matrix:\n", confusion_matrix(y_test, y_pred_custom))

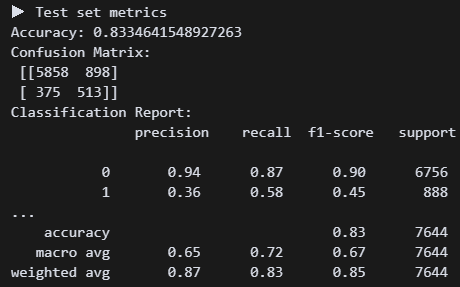

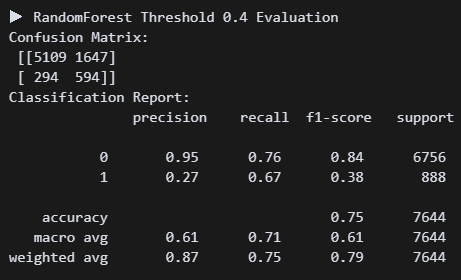

print("Classification Report:\n", classification_report(y_test, y_pred_custom))이건 지선생이 추천해줘서 해본 건데, 아직 무슨 코드인지 정확히 이해할 수 없다. 임계값을 낮춰 내가 원하는 요소를 조금 더 잘 찾도록 하는 것 같다. threshold = 0.4 으로 했다.

정확도는 더 낮아졌지만 리콜 수치가 0.07 상승했다. 나는 미가입자를 찾는 것보다 가입자를 찾는 게 더 중요하다고 판단했다. 그래서 리콜 수치를 높여주는 이 방식이 맞는 것 같다. 일단 임계치 코드는 저장해놨다가 나중에 써봐야지!

정확도는 더 낮아졌지만 리콜 수치가 0.07 상승했다. 나는 미가입자를 찾는 것보다 가입자를 찾는 게 더 중요하다고 판단했다. 그래서 리콜 수치를 높여주는 이 방식이 맞는 것 같다. 일단 임계치 코드는 저장해놨다가 나중에 써봐야지!

(3) XGBoost

''' Boosting(XGBoost) '''

# 모델 구현

from xgboost import XGBClassifier

m_xgb = XGBClassifier(

random_state=42

).fit(X_train, y_train)

y_train_pred = m_xgb.predict(X_train)

y_test_pred = m_xgb.predict(X_test)

# 평가

print_metrics() 명성이 자자한 XGB. 튜닝 전후 비교를 위해 하파는 깡통으로 진행. 현재 리콜 0.26이다. 처참하군..

명성이 자자한 XGB. 튜닝 전후 비교를 위해 하파는 깡통으로 진행. 현재 리콜 0.26이다. 처참하군..

# 튜닝

from sklearn.model_selection import GridSearchCV

params = {

'n_estimators': [100, 200],

'max_depth': [3, 5, 7],

'learning_rate': [0.05, 0.1],

'min_child_weight': [1, 5],

'gamma': [0, 1],

'subsample': [0.8],

'colsample_bytree': [0.8],

'scale_pos_weight': [3, 5]

}

search = GridSearchCV(

XGBClassifier(

use_label_encoder=False,

eval_metric='logloss',

random_state=42

),

param_grid=params,

scoring='recall',

cv=3,

verbose=1,

n_jobs=-1

).fit(X_train, y_train)

print("Best XGBClassifier:", search.best_params_)튜닝을 해준다. 하파명이 랜포랑 비슷한 것 같긴 한데 뭔가 넣을 게 더 많은 것 같기도 하고...ㅠㅠ

Best XGBClassifier: {'colsample_bytree': 0.8, 'gamma': 1, 'learning_rate': 0.1, 'max_depth': 3, 'min_child_weight': 5, 'n_estimators': 100, 'scale_pos_weight': 5, 'subsample': 0.8} 이런 수치가 나왔다.

# 모델 재구현

from xgboost import XGBClassifier

m_xgb = XGBClassifier(

**search.best_params_,

use_label_encoder=False,

eval_metric='logloss',

random_state=42

).fit(X_train, y_train)

y_train_pred = m_xgb.predict(X_train)

y_test_pred = m_xgb.predict(X_test)

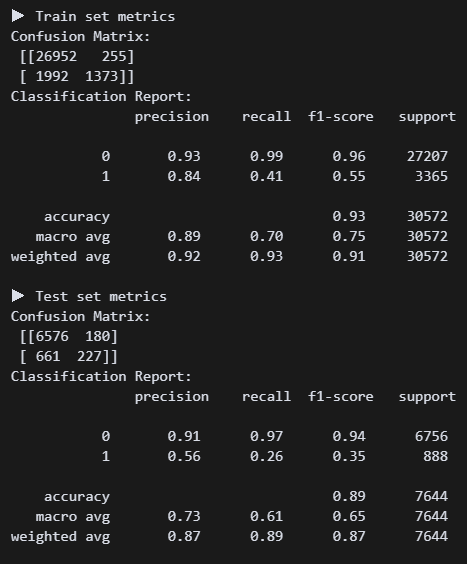

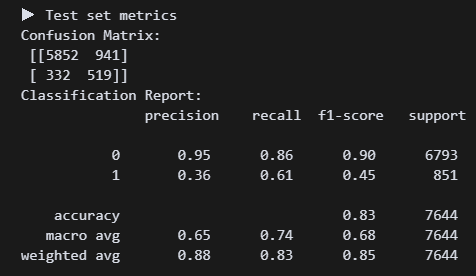

print_metrics() 다시 해보니까 리콜 수치가 0.54로 올랐다. 왠지 랜포가 더 쉽고 좋은 것 같다. (사실 내가 튜닝을 제대로 못해서 그럼)

다시 해보니까 리콜 수치가 0.54로 올랐다. 왠지 랜포가 더 쉽고 좋은 것 같다. (사실 내가 튜닝을 제대로 못해서 그럼)

(4) LightGBM

''' Boosting(LightGBM)'''

# 정답 컬럼

y = df_cat['y']

X = df_cat.drop(columns=['y'])

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, stratify=y, random_state=42)

from lightgbm import LGBMClassifier이 녀석을 위해 어제 df를 df_encoded와 df_cat으로 나눴었다. lightBGM은 카테고리형을 자동변환해서 잡는다는데 기대가 된다.

# 모델 구현

m_lgb = LGBMClassifier(

class_weight='balanced',

random_state=42

).fit(X_train, y_train)

y_train_pred = m_lgb.predict(X_train)

y_test_pred = m_lgb.predict(X_test)

print_metrics()일단 최대한 깡통으로 진행해보자.

뭔 경고가 엄청나게 뜬다.

뭔 경고가 엄청나게 뜬다. verbose=-1 한 줄 넣어주면 안 뜬다고 한다.

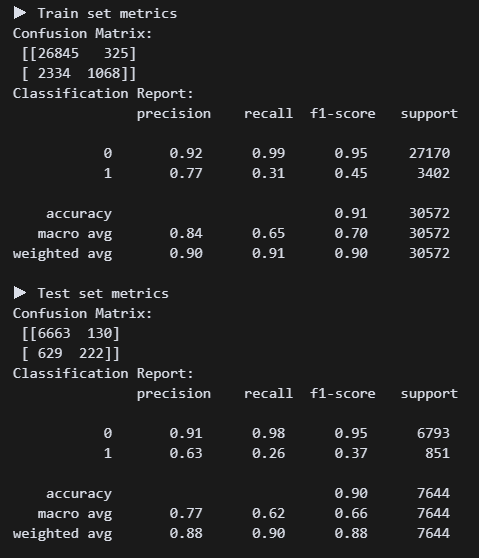

흠.. 리콜 수치가 처참하다. 튜닝튜닝튜닝!!!

흠.. 리콜 수치가 처참하다. 튜닝튜닝튜닝!!!

# 튜닝

from sklearn.model_selection import GridSearchCV

param_grid = {

'n_estimators': [100, 200],

'learning_rate': [0.05, 0.1],

'max_depth': [3, 5],

'num_leaves': [15, 31],

'min_child_samples': [20, 50],

'class_weight': ['balanced']

}

grid_lgb = GridSearchCV(

LGBMClassifier(random_state=42),

param_grid=param_grid,

scoring='recall',

cv=3,

verbose=1,

n_jobs=-1

).fit(X_train, y_train)

best_lgb = grid_lgb.best_estimator_

print("Best LGBMClassifier:", grid_lgb.best_params_)Best LGBMClassifier: {'class_weight': 'balanced', 'learning_rate': 0.05, 'max_depth': 3, 'min_child_samples': 20, 'n_estimators': 200, 'num_leaves': 15} 이렇게 나왔다. 바로 모델에 넣어주자!

m_lgb = LGBMClassifier(

n_estimators=200,

learning_rate=0.05,

max_depth=3,

min_child_samples=20,

num_leaves=15,

class_weight='balanced',

random_state=42

).fit(X_train, y_train)

y_train_pred = m_lgb.predict(X_train)

y_test_pred = m_lgb.predict(X_test) 헉 0.61!???

헉 0.61!???

# 임계값 조정

y_proba = m_lgb.predict_proba(X_test)[:, 1]

y_pred_custom = (y_proba >= 0.4).astype(int)

print("▶ Threshold 0.4 Evaluation")

print(classification_report(y_test, y_pred_custom))

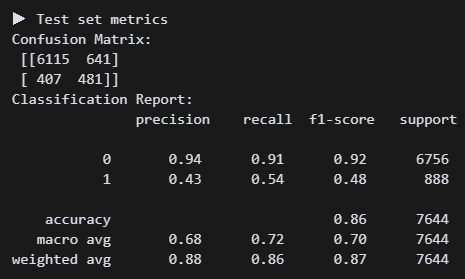

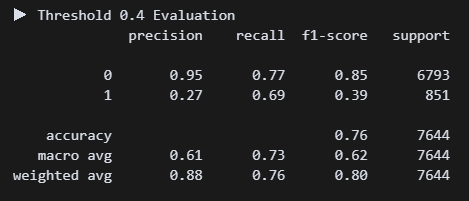

이건 임계값도 조정해 보자!

와 0.69면 지금까지 만든 모델 중에서 베스트다....

와 0.69면 지금까지 만든 모델 중에서 베스트다....

# 시각화

import matplotlib.pyplot as plt

feat_imp = pd.Series(m_lgb.feature_importances_, index=X.columns)

top_feat = feat_imp.sort_values(ascending=False).head(10)

plt.figure(figsize=(10, 5))

top_feat.sort_values().plot(kind='barh')

plt.title("LightGBM Top 10 Feature Importance")

plt.xlabel("Importance Score")

plt.tight_layout()

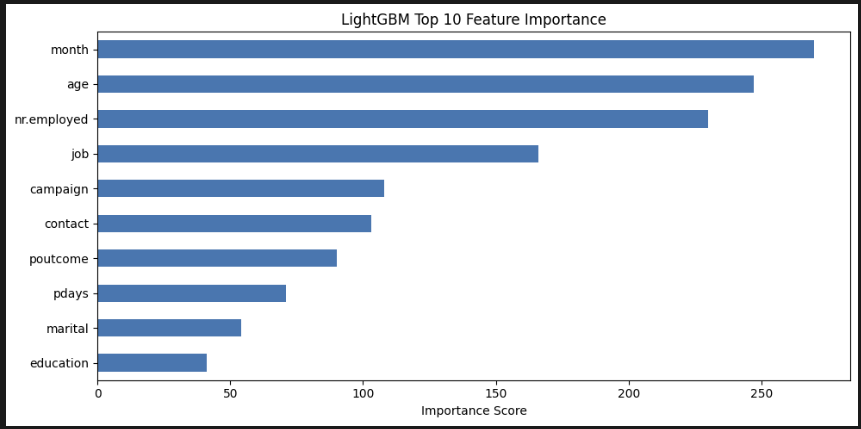

plt.show() LGBM은 특이하게도 월>나이>고용률>직업 순으로 중요하게 생각했다. 음 나도 pdays나 campaign보다는 이게 맞는 방향인 것 같다.

LGBM은 특이하게도 월>나이>고용률>직업 순으로 중요하게 생각했다. 음 나도 pdays나 campaign보다는 이게 맞는 방향인 것 같다.

(5) Catboost

라이브러리 설치가 안 된다 ㅠㅠ 카테고리 전문가처럼 보이는 이 녀석을 꼭 사용해 보고 싶었는데...

(6) Stacking

이 기법은 아직 이해를 제대로 못했다.. 나중에 다시 돌아오마..

4. 마치며

(1) 중요한 특성 순위

(LightGBM 모델 예측 결과 기반)

| 중요도 순위 | 변수명 |

|---|---|

1. month | 마지막 연락 월 |

2. age | 나이 |

3. nr.employed | 고용자 수(경제 지표) |

4. job | 고객의 직업군 |

5. campaign | 이번 캠페인 연락 횟수 |

6. contact | 연락 방식 |

7. poutcome | 이전 캠페인 결과 |

8. pdays | 이전 연락 후 경과일 |

9. marital | 혼인 여부 |

10. education | 교육 수준 |

(2) 마케팅 전략

A. 캠페인 타이밍 전략

month중요도 1위 → 특정 월에 가입률이 집중됨- 월별 성과 분석을 통해 성수기를 파악하고 성과 높은 월에 집중적인 마케팅 집행

- 3, 9, 10, 12월월 집중 캠페인 → 성과 2배”

B. 연령 기반 타겟팅

age중요도 2위 → 나이에 따라 가입 행동 다름- 20대 초반 60대 이후 연령 집중적으로 캠페인 진행

C. 경제 지표 기반 시기 예측

nr.employed중요도 3위- 고용률이 높을수록 고객의 여유 자금 가능성 ↑

- 외부 지표와 연동하여 타이밍 판단

- 고용자 수 증가 시점에 예금 프로모션 강화

D. 직업군별 맞춤 전략

job중요도 4위- 가입률 높은 직업군 파악하여 직업군별 전용 메시지/상품 제안

- "전문직 고객을 위한 프리미엄 예금" 등

E. 연락 방식과 빈도 최적화

contact,campaign,pdays는 “언제, 어떻게, 몇 번 연락했는가”에 관한 변수- 너무 자주 연락하면 가입률 떨어짐 (캠페인 효율성 저하)