1. 데이터 개요

- 데이터셋: Credit Card Fraud Detection

- 배경 설명

- 신용카드사는 비정상적인 고객의 카드 거래를 인지하여 피해를 최소화핲 필요가 있다.

- 신용카드 사기를 탐지할 수 있는 모델을 생성하여 건전한 금융서비스에 기여하고자 한다.

2. 데이터 불러오기

- 데이터 로드

import pandas as pd

fpath = "./data/creditcard.csv"

df = pd.read_csv(fpath)- 데이터 정보 확인

# 약 28만개 행 X 31개 컬럼으로 구성, 결측치는 없음

df.info()

## 출력 결과

# <class 'pandas.core.frame.DataFrame'>

# RangeIndex: 284807 entries, 0 to 284806

# Data columns (total 31 columns):

# # Column Non-Null Count Dtype

# --- ------ -------------- -----

# 0 Time 284807 non-null float64

# 1 V1 284807 non-null float64

# 2 V2 284807 non-null float64

# 3 V3 284807 non-null float64

# (중략)

# 26 V26 284807 non-null float64

# 27 V27 284807 non-null float64

# 28 V28 284807 non-null float64

# 29 Amount 284807 non-null float64

# 30 Class 284807 non-null int64

# dtypes: float64(30), int64(1)

# memory usage: 67.4 MB- 첫 5행 확인

# V1 ~ V28 컬럼은 개인정보 보호 차 수치형 변수로 비식별화되어 있음

df.head()

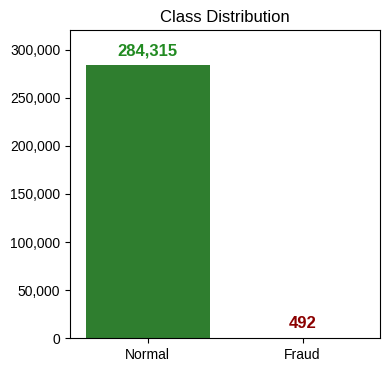

- 종속변수 확인

# 사기(1; Fraud)에 해당하는 데이터가 0.2% 정도 밖에 되지 않음

# 극심한 불균형 상태에 해당되어 향후 분석작업 유의 필요

df["Class"].value_counts(normalize=True).round(3)

## 출력 결과

# Class

# 0 0.998

# 1 0.002

# Name: proportion, dtype: float64

# 시각화

import matplotlib.pyplot as plt

import seaborn as sns

from matplotlib.ticker import FuncFormatter

import warnings

warnings.filterwarnings("ignore")

plt.rcParams["font.family"] = "Liberation Sans"

count_info = df["Class"].value_counts()

class_mapper = {"0": "Normal", "1": "Fraud"}

fig, ax = plt.subplots(figsize=(4,4))

sns.barplot(count_info, ax=ax, palette={"0": "forestgreen", "1": "darkred"})

for p in ax.patches:

ax.annotate(f"{int(p.get_height()):,d}",

xy=((p.get_x()+p.get_width()/2), p.get_height()+10_000),

ha="center",

color="forestgreen" if p.get_height() > 150_000 else "darkred",

weight="bold",

size=12)

ax.set_title("Class Distribution")

ax.set_xticklabels([class_mapper.get(label.get_text()) for label in ax.get_xticklabels()])

ax.set_xlabel(None)

ax.set_ylabel(None)

ax.set_ylim(0, 320_000)

ax.yaxis.set_major_formatter(FuncFormatter(lambda val, pos: f"{int(val):,d}"))

plt.show()

3. 데이터 들여다보기

- 독립변수와 종속변수 분리

X = df.drop(["Time", "Class"], axis=1) # Time 변수도 불필요하여 제거

y = df["Class"]

print(X.shape, y.shape)

## 출력 결과

# (284807, 29) (284807,)- 데이터 요약정보 확인

# V1~V28 변수간에는 최소-최대값 간 편차가 심한 편으로 확인

# Amount 변수의 중위수-최대값의 차이가 상당히 커 이상치가 존재하는 것으로 보임

X.describe().round(2)

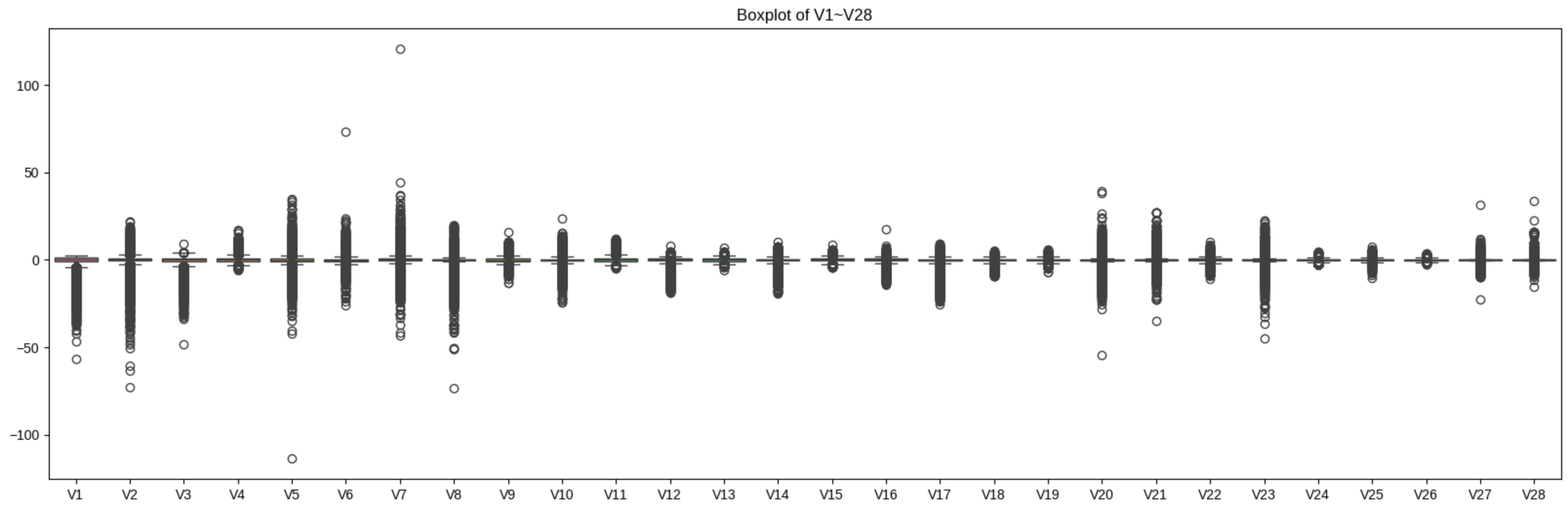

- V1~V28 컬럼의 박스플롯 시각화

# 일부 이상치 확인되었으나, 향후 트리 기반 모델링 수행 예정으로 감안 가능한 수준으로 판단

fig, ax = plt.subplots(figsize=(20, 6))

sns.boxplot(X.loc[:,"V1":"V28"], ax=ax)

plt.show()

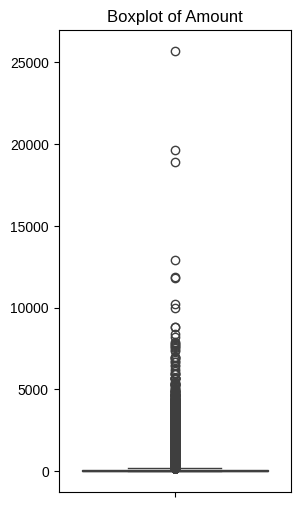

- Amount 컬럼의 박스플롯 시각화

# 분포가 상당히 왜곡되어 있음을 알 수 있음

fig, ax = plt.subplots(figsize=(3, 6))

sns.boxplot(X["Amount"], ax=ax)

ax.set_title("Boxplot of Amount")

ax.set_xlabel(None)

ax.set_ylabel(None)

plt.show()

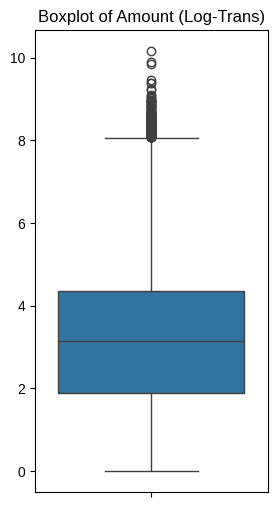

- Amount 컬럼 대상 로그 변환 수행 후 재 시각화

import numpy as np

X["Amount_Log"] = np.log1p(X["Amount"])

# 분포가 개선되었음을 확인

fig, ax = plt.subplots(figsize=(3, 6))

sns.boxplot(X["Amount_Log"], ax=ax)

ax.set_title("Boxplot of Amount (Log-Trans)")

ax.set_xlabel(None)

ax.set_ylabel(None)

plt.show()

- 기존 Amount 컬럼은 삭제

X.drop("Amount", axis=1, inplace=True)4. 데이터 분리하기

- Train 데이터셋과 Test 데이터셋 분리

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=.3, random_state=42, stratify=y)- Train, Test 데이터셋의 종속변수 비율 재확인

print("TRAIN\n", y_train.value_counts(normalize=True).round(3))

print("\nTEST\n", y_test.value_counts(normalize=True).round(3))

## 출력 결과

# TRAIN

# Class

# 0 0.998

# 1 0.002

# Name: proportion, dtype: float64

#

# TEST

# Class

# 0 0.998

# 1 0.002

# Name: proportion, dtype: float646. 모델 생성하기

- 분류기 평가용 함수 정의

# 모델 평가용 함수

from sklearn.metrics import accuracy_score, precision_score, recall_score, f1_score, roc_auc_score, confusion_matrix

from time import time

# 지표 반환

def get_eval(y_test, pred):

acc = accuracy_score(y_test, pred)

prec = precision_score(y_test, pred)

rec = recall_score(y_test, pred)

f1 = f1_score(y_test, pred)

auc = roc_auc_score(y_test, pred)

return acc, prec, rec, f1, auc

# 지표 출력

def print_eval(y_test, pred):

acc, prec, rec, f1, auc = get_eval(y_test, pred)

conf = confusion_matrix(y_test, pred)

print("\n=== Confusion Mtx. ===")

print(conf)

print("\n=== Metrics ===")

print(f"Accuracy: {acc:.3f}")

print(f"Precision: {prec:.3f}")

print(f"Recall: {rec:.3f}")

print(f"F1-score: {f1:.3f}")

print(f"AUC: {auc:.3f}")

# 모델 적합 + 지표 출력 + 지표 반환 자동화

def auto_eval(estimator, X_train, y_train, X_test, y_test):

s_time = time()

estimator.fit(X_train, y_train)

e_time = time()

print(f"=== Fit Time ===\n{e_time-s_time:.2f}sec")

pred = estimator.predict(X_test)

print_eval(y_test, pred)

nm = estimator.__class__.__name__

acc, prec, rec, f1, auc = get_eval(y_test, pred)

res = pd.DataFrame([[acc, prec, rec, f1, auc]], columns=["Acc.", "Prec.", "Rec.", "F1", "AUC"], index=[nm])

return res- 의사결정나무 모델 생성

from sklearn.tree import DecisionTreeClassifier

dt = DecisionTreeClassifier(random_state=42)

dt.fit(X_train, y_train)

pred = dt.predict(X_test)

print_eval(y_test, pred)

## 출력 결과

# === Fit Time ===

# 15.36sec

#

# === Confusion Mtx. ===

# [[85281 14]

# [ 39 109]]

#

# === Metrics ===

# Accuracy: 0.999

# Precision: 0.886

# Recall: 0.736

# F1-score: 0.804

# AUC: 0.868- 랜덤포레스트 모델 생성

from sklearn.ensemble import RandomForestClassifier

# n_estimators 조정을 통한 학습 시간 단축 (default=100)

rf = RandomForestClassifier(random_state=42, n_estimators=10, max_depth=10, n_jobs=-1)

rf_res = auto_eval(rf, X_train, y_train, X_test, y_test)

## 출력 결과

# === Fit Time ===

# 16.99sec

#

# === Confusion Mtx. ===

# [[85289 6]

# [ 34 114]]

#

# === Metrics ===

# Accuracy: 1.000

# Precision: 0.950

# Recall: 0.770

# F1-score: 0.851

# AUC: 0.885- LightGBM 모델 생성

from lightgbm import LGBMClassifier

lgbm = LGBMClassifier(random_state=42, verbose=0)

lgbm_res = auto_eval(lgbm, X_train, y_train, X_test, y_test)

## 출력 결과

# === Confusion Mtx. ===

# [[85119 176]

# [ 66 82]]

# === Metrics ===

# Accuracy: 0.997

# Precision: 0.318

# Recall: 0.554

# F1-score: 0.404

# AUC: 0.776- 세 모델의 결과 취합

# 세 모델 중에서는 랜덤 포레스트의 성능이 전반적으로 우수함

all_res = pd.concat([dt_res, rf_res, lgbm_res,], axis=0)

all_res.round(3)

7. 오버샘플링 해보기

- SMOTE 적용 후 세 모델의 결과 비교: 연산량 대비 성능 개선의 효과가 있다고 보기는 어려움

# SMOTE와 같은 오버샘플링 기법은 데이터 중복, 겹침 문제를 유발할 수 있어 실무 적용 시에는 신중해야 함

from imblearn.over_sampling import SMOTE

smt = SMOTE(random_state=42)

X_train_smt, y_train_smt = smt.fit_resample(X_train, y_train)

dt_res_smt = auto_eval(dt, X_train_smt, y_train_smt, X_test, y_test)

rf_res_smt = auto_eval(rf, X_train_smt, y_train_smt, X_test, y_test)

lgbm_res_smt = auto_eval(lgbm, X_train_smt, y_train_smt, X_test, y_test)

## 출력 결과: 생략

all_res_smt = pd.concat([dt_res_smt, rf_res_smt, lgbm_res_smt,], axis=0)

all_res_smt.round(3)

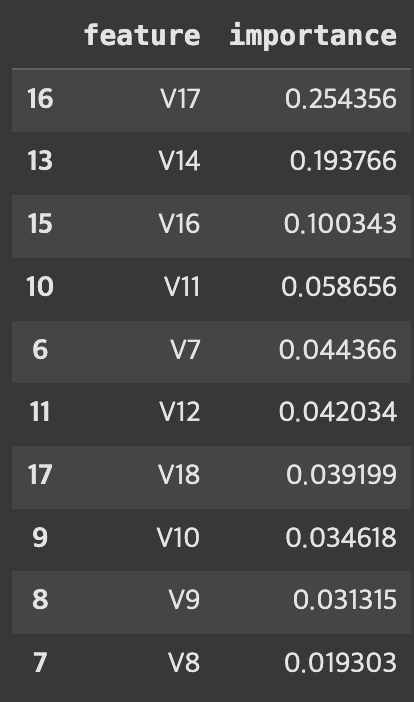

8. 변수별 중요도 확인

- 가장 나은 성능을 보인 RF 모델 기준 변수 중요도 추출

# 가장 나은 성능을 보인 RF 기준 변수 중요도 추출

rf.fit(X_train, y_train)

rf_fi = pd.DataFrame({"feature": X_train.columns, "importance": rf.feature_importances_})

rf_fi.sort_values(by="importance", ascending=False).head(10)

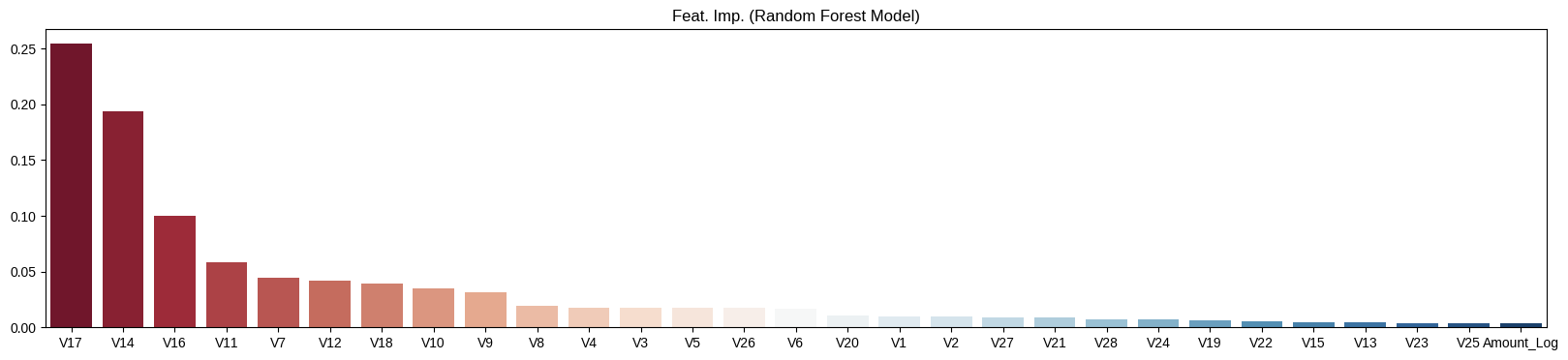

- 변수 중요도 시각화

rf_fi.sort_values(by="importance", ascending=False, inplace=True)

fig, ax = plt.subplots(figsize=(20,4))

sns.barplot(x=rf_fi["feature"],

y=rf_fi["importance"],

hue=rf_fi["feature"],

ax=ax,

palette="RdBu")

ax.set_title("Feat. Imp. (Random Forest Model)")

ax.set_ylabel(None)

ax.set_xlabel(None)

plt.show()

9. 결론

- 트리 기반 모델 중에서는 Random Forest 모델이 지표 전반적으로 가장 강건한 성능을 보임

- 특히, V17, V14, V16 세 컬럼이 의사결정에 가장 큰 영향을 끼쳤음

- 오버샘플링 기법 중 하나인 SMOTE 기법은 큰 효과가 없었음

- 하이퍼파라미터 튜닝을 통해 성능개선을 시도해보거나, 다른 분류모델을 사용해보거나, 변수 중요도가 낮은 변수들을 제외하여 모델 경량화 등을 시도해 볼 수 있음

*이 글은 제로베이스 데이터 취업 스쿨의 강의 자료 일부를 발췌하여 작성되었습니다.

데이터 분석, 데이터 사이언스 학습 저장소