Last time, my model was overfitted because I did not handle the noises within the data.

This time, I was inspired by the article: Denoising Stock Price Time Series with Singular Spectrum Analysis for Enhanced Deep Learning Forecasting by Carol Anne Hargreaves and Zixian Fan.

Singular Spectrum Analysis is a technique that adjusts each data points according to its significance in the dataset. It is a very effective method for denoising and feature extracting.

This article also introduced CNN-LSTM hybrid model, where CNN layers is used for feature extraction.

Singular Spectrum Analysis (SSA)

I first created a method for calculating SSA value for a certain range (lookback).

def apply_ssa_trend(series, window = 15, lookback = 60):

n_total = len(series)

result = np.zeros(n_total)

result[:lookback] = series[:lookback]

for t in range(lookback, n_total):

sub_series = series[t - lookback + 1 : t + 1]

N = len(sub_series)

L = window

K = N - L + 1

X = np.column_stack([sub_series[i:i+L] for i in range(K)])

U, Sigma, VT = np.linalg.svd(X, full_matrices=False)

X1 = Sigma[0] * np.outer(U[:, 0], VT[0, :])

n = N - 1

vals = [X1[i, n-i] for i in range(max(0, n-K+1), min(n+1, L))]

result[t] = np.mean(vals)

return resultThen I adjusted my get_dataset() method that applies SSA. My previous get_dataset() method applied most of its data preprocessing steps (ex. scaling, column extraction, etc) within two methods, so checking the the dataset for each step was kind of complicated. I separated those steps so that I can analyze the dataset before applying certain steps.

def get_dataset_columns(ticker, period="1y", window=60):

df = yf.Tickers(ticker).history(period=period)

vix_data = yf.Tickers("^VIX").history(period=period, progress=False)

df.columns = df.columns.droplevel(1)

vix_data.columns = vix_data.columns.droplevel(1)

df = df.ffill().dropna()

vix_data = vix_data.reindex(df.index).ffill()

df = df.drop(['Stock Splits', 'Dividends'], axis=1)

open_trend = apply_ssa_trend(df['Open'].values, window=int((window/4)))

vix_trend = apply_ssa_trend(vix_data['Open'].values, window=int((window/4)))

min_len = min(len(df), len(open_trend), len(vix_trend))

df = df.iloc[:min_len]

df['Open_Trend'] = open_trend[:min_len]

df['Vix_Trend'] = vix_trend[:min_len]

df['Trend_Diff'] = df['Open'] - df['Open_Trend']

df['Target'] = ((df['Close'] - df['Open']) * 100 / df['Open'])

# df['Target'] = np.log(df['Close'] / df['Open']) * 100

# df['Target'] = df['Close']

df = df.drop(df.index[0])

df = df.drop(['High', 'Low', 'Volume', 'Close'], axis=1)

feature_cols = ["Open_Trend", "Trend_Diff", "Vix_Trend"]

target_col = ["Target"]

return df, feature_cols, target_col

def scale_dataset(df, ticker, feature_cols, target_col, test_size=0.2, scale_target=False):

train_size = int(len(df) * (1 - test_size))

df_train = df.iloc[:train_size]

if ticker not in feature_scalers:

f_scaler = StandardScaler()

f_scaler.fit(df_train[feature_cols])

feature_scalers[ticker] = f_scaler

if scale_target:

t_scaler = StandardScaler()

t_scaler.fit(df_train[target_col])

target_scalers[ticker] = t_scaler

df[feature_cols] = feature_scalers[ticker].transform(df[feature_cols])

if scale_target:

df[target_col] = target_scalers[ticker].transform(df[target_col])

data_x = df[feature_cols].values

data_y = df[target_col].values

return data_x, data_y

def get_full_dataset(tickers, period="1y", window_size=60, test_size=0.2):

X_total, y_total = [], []

for ticker in tickers:

df, feature_cols, target_col = get_dataset_columns(ticker, period=period, window=window_size)

data_x, data_y = scale_dataset(df, ticker, feature_cols, target_col, test_size, scale_target=False)

for i in range(len(df) - window_size):

X_total.append(data_x[i : i + window_size])

y_total.append(data_y[i + window_size])

X_data = np.array(X_total)

y_data = np.array(y_total)

nan_mask = np.isnan(X_data).any(axis=(1, 2))

X_data = X_data[~nan_mask]

y_data = y_data[~nan_mask]

print(f"NaN Deleted: {np.sum(nan_mask)}")

test_first_index = int(len(X_data) * (1 - test_size))

X_train, X_test = X_data[:test_first_index], X_data[test_first_index:]

y_train, y_test = y_data[:test_first_index], y_data[test_first_index:]

print("""

X_train Shape : {}

X_test Shape : {}

y_train Shape : {}

y_test Shape : {}

""".format(X_train.shape, X_test.shape, y_train.shape, y_test.shape))

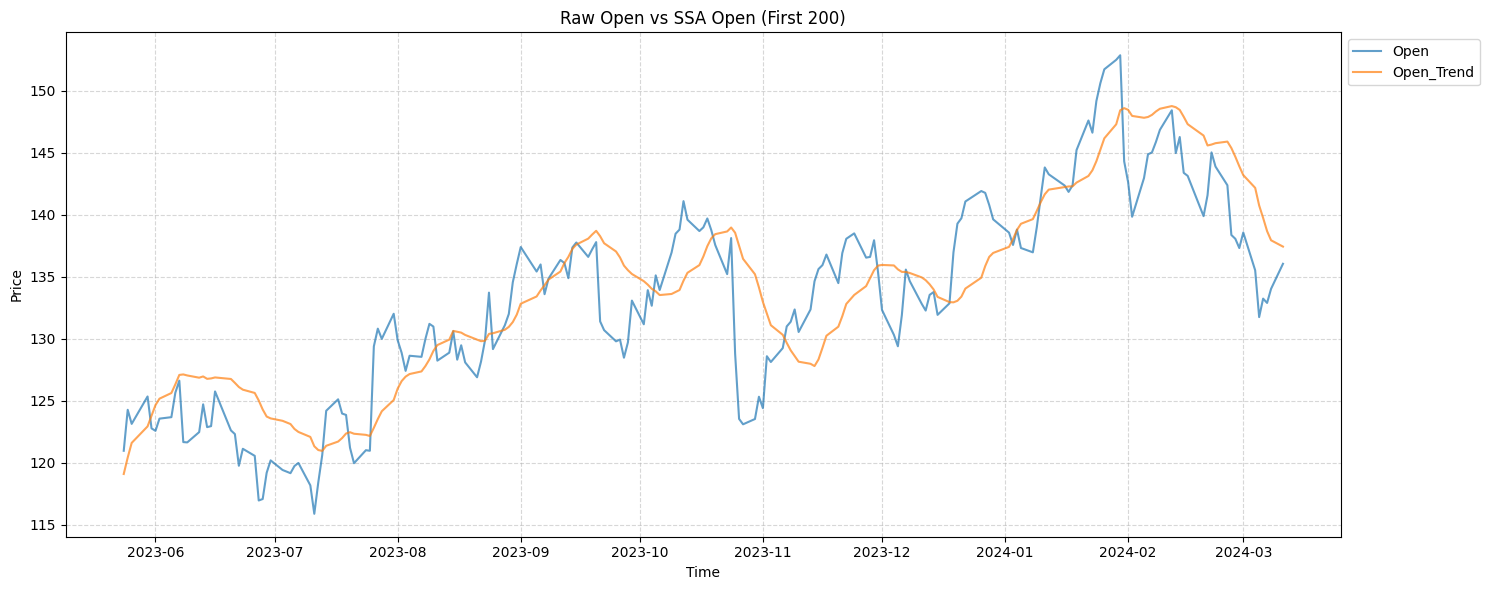

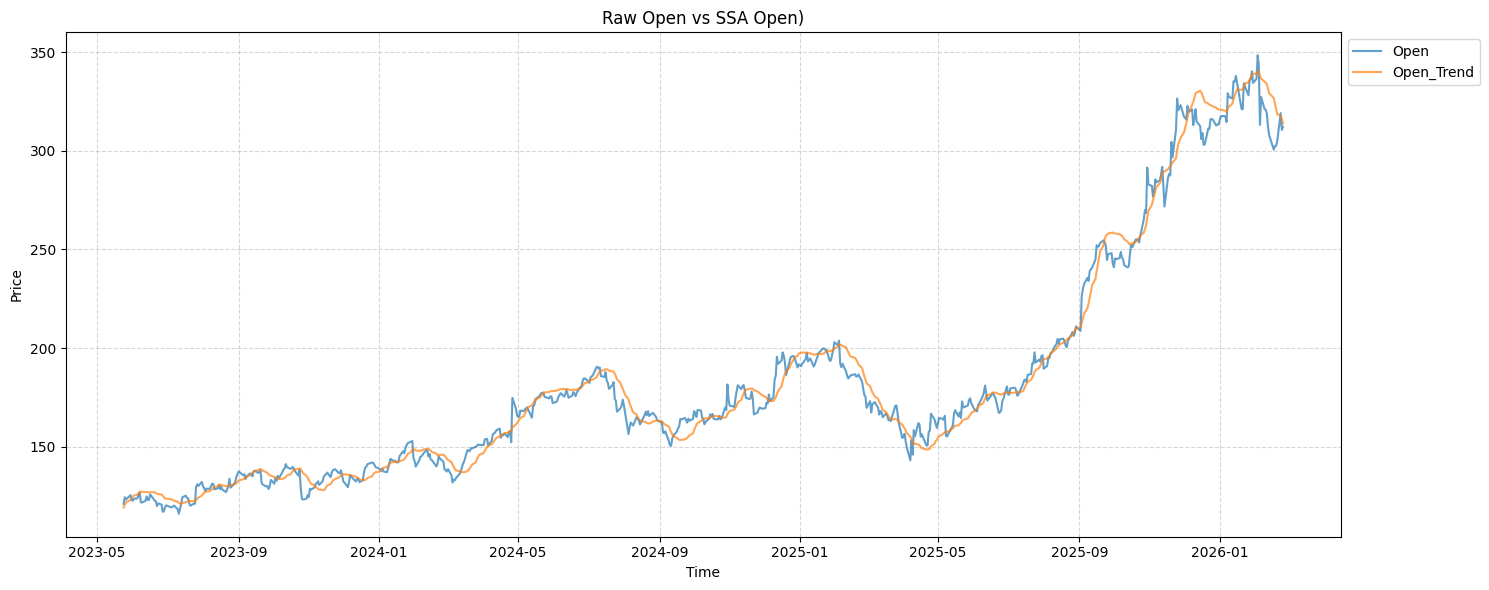

return X_train, X_test, y_train, y_testThe resulting dataset would now have a “Open” column and “Open Trend” that would look like this:

It looks like it is lagging because each values are calculated based on the average movement of the past 60 days. To address this problem, I added another column "Trend_Diff" that represents the noise within the trend.

CNN-LSTM Hybrid Model

This is the CNN-LSTM model I chose.

def get_CNN_LSTM_hybrid(window_size=60, feature_num=7):

dropout_rate = 0.2

input_layer = Input(shape=(window_size, feature_num), name="Input")

x = Conv1D(filters=64, kernel_size=3, strides=1, padding='same', activation='relu', name="Conv1D_1")(input_layer)

x = LayerNormalization(name="LayerNormalization_1")(x)

x = Conv1D(filters=64, kernel_size=3, strides=1, padding='same', activation='relu', name="Conv1D_2")(x)

x = LayerNormalization(name="LayerNormalization_2")(x)

x = MaxPooling1D(pool_size=2, name="Max_Pooling")(x)

x = LSTM(64, return_sequences=True, name="LSTM_1")(x)

x = Dropout(dropout_rate, name="Dropout_1")(x)

x = BatchNormalization(name="BatchNormalization_1")(x)

x = LSTM(32, return_sequences=False, name="LSTM_2")(x)

x = Dropout(dropout_rate, name="Dropout_2")(x)

x = BatchNormalization(name="BatchNormalization_2")(x)

x = Dense(16, activation="relu", name="FullyConnected_1")(x)

output_layer = Dense(1, activation="linear", name="Output")(x)

model = Model(inputs=input_layer, outputs=output_layer, name='SSA_CNN_LSTM_Hybrid')

optimizer = tf.keras.optimizers.Adam(learning_rate=0.001)

model.compile(optimizer=optimizer,

loss='mse',

metrics=['mae', tf.keras.metrics.RootMeanSquaredError()])

return model

CNN_LSTM_model = get_CNN_LSTM_hybrid(window_size, feature_num)

CNN_LSTM_model.summary()This is the previous LSTM model I will be comparing to:

def get_LSTM_model(window_size=60, feature_num=7):

dropout_rate = 0.2

input_layer = Input(shape = (window_size, feature_num), name="Input")

batch_norm_layer = BatchNormalization(name="BatchNormalization_1")(input_layer)

LSTM_layer = LSTM(64, return_sequences=True, name = "LSTM_1")(batch_norm_layer)

hidden_layer = Dropout(dropout_rate, name = f"Dropout_1_{dropout_rate}")(LSTM_layer)

hidden_layer = BatchNormalization(name="BatchNormalization_2")(hidden_layer)

hidden_layer = LSTM(32, name = "LSTM_2")(hidden_layer)

hidden_layer = Dropout(dropout_rate, name = f"Dropout_2_{dropout_rate}")(hidden_layer)

hidden_layer = Dense(16, activation = "relu", name="Dense")(hidden_layer)

output_layer = Dense(1, activation = "linear", name="Output")(hidden_layer)

model = Model(inputs = input_layer, outputs = output_layer, name='LSTM_BatchNorm_Dropout0.2_3y_window30')

optimizer = tf.keras.optimizers.Adam(learning_rate=0.0001)

# loss_fn = tf.keras.losses.Huber()

model.compile(optimizer = optimizer, loss = 'mse', metrics=['mae', tf.keras.metrics.RootMeanSquaredError()])

return model

LSTM_model = get_LSTM_model(window_size, feature_num)

LSTM_model.summary()Results:

I trained the model with the same companies as last time.

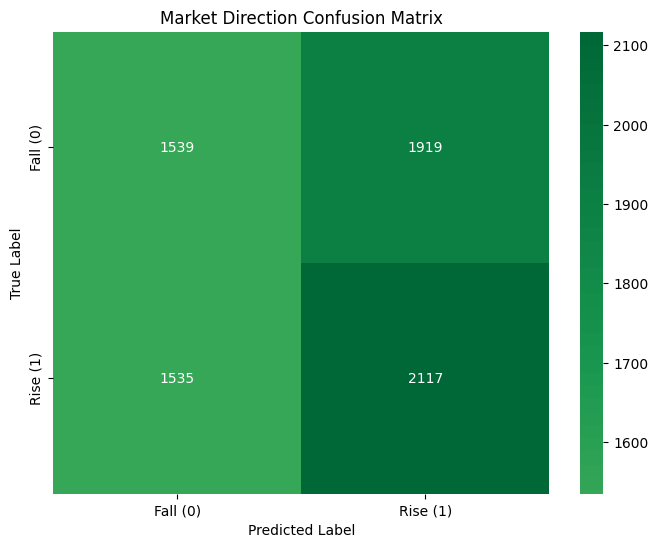

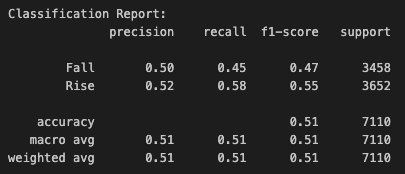

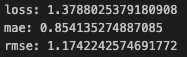

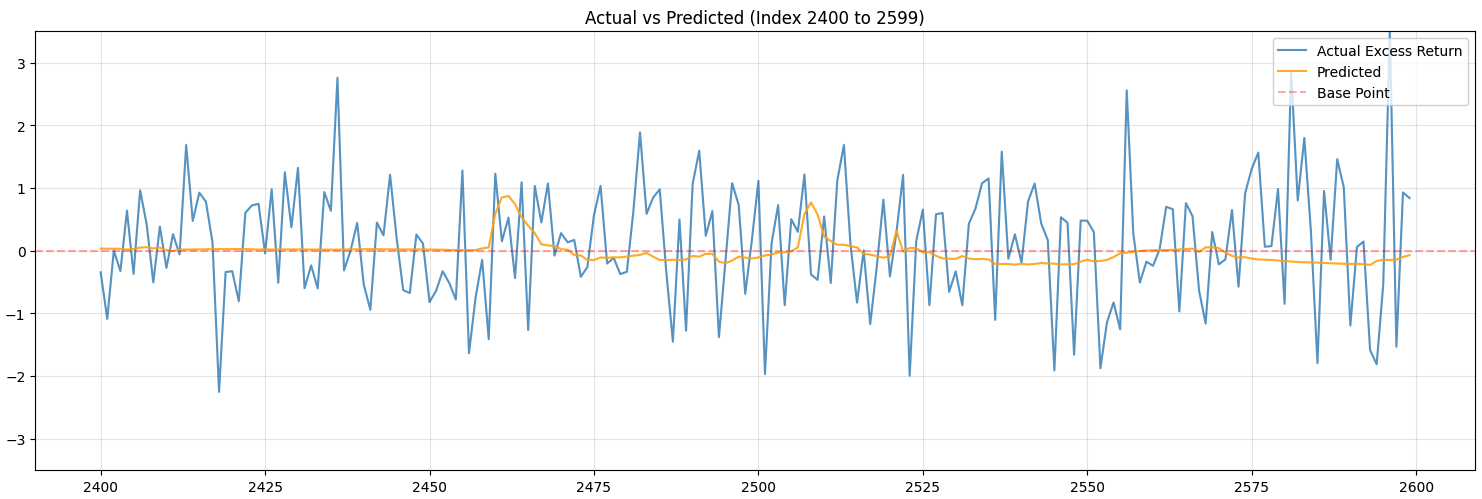

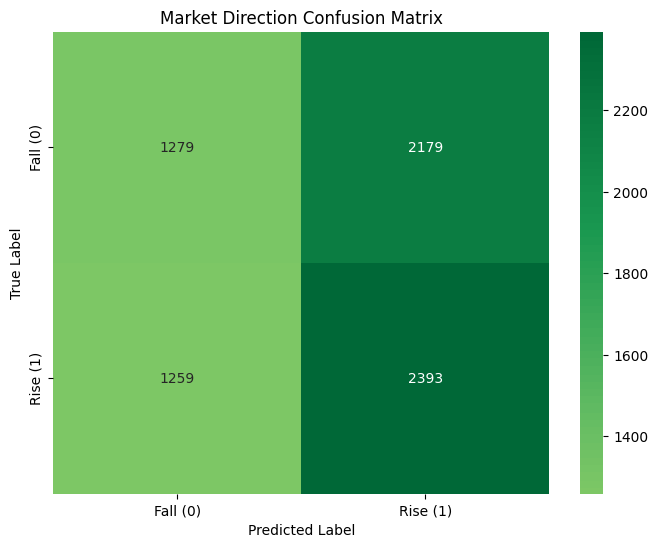

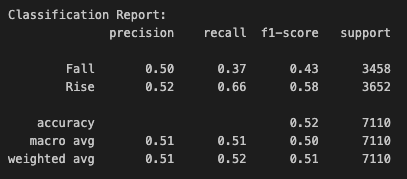

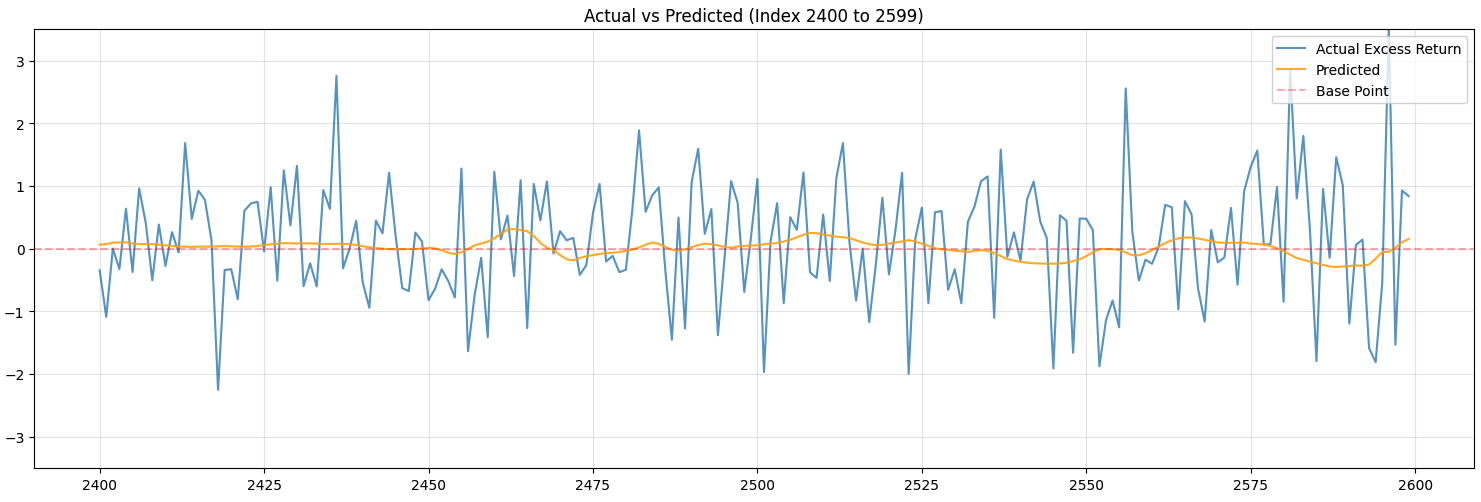

These are the results for CNN-LSTM model:

These only represent the classification of whether the price will rise or not.

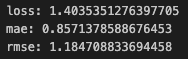

These are the metrics regarding the value:

Although the model is terrible at predicting, I see this as a huge improvement.

The previous LSTM model only predicted the value to be rising and the orange line was just a straight line. It is now predicting more diversely.

These are the results for previous LSTM model:

The LSTM model’s predictions have also shown improvements, but are still kind of overfitted. This still means that SSA is actually helping address overfitting problem.

The results show that applying SSA method and implementing CNN-LSTM model helped addressing overfitting problem.

Next time, I will be trying to improve the accuracy. I think I will be trying to add diffusion model in-between, but more research is required (if I find something that seems to be more effective, I might implement that).

Reference:

Hargreaves, C. A., & Fan, Z. (2026). Denoising Stock Price Time Series with Singular Spectrum Analysis for Enhanced Deep Learning Forecasting. Analytics, 5(1), 9. https://doi.org/10.3390/analytics5010009