Recap

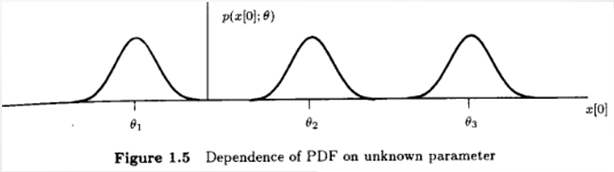

Revisit : Likelihood Function

- The

Likelihood Function(same description of PDF) - But as a function of parameter w/ the data vector fixed

|  |

|---|

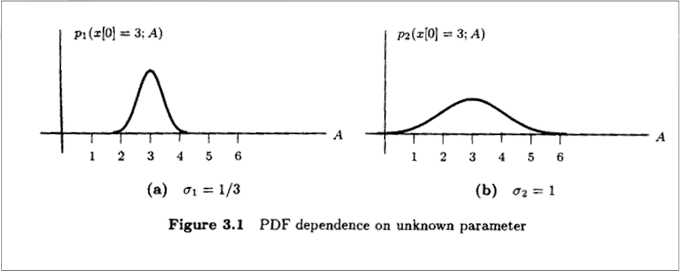

Likelihood Function Characteristics

- Intuitively :

sharpnessof theLikelihood Functionsets accuracy Sharpnessis measured usingcurvature:- Curvature ↑ ⇒ PDF concentration ↑ ⇒ Accuracy ↑

- Expected sharpness of

likelihood function

Vector Form of the CRLB

- Assuming satisfies the

regularity condition - The

covariance matrixof anyunbiased estimatorsatisfieswhere means the matrix ispositive semidefinite - Furthermore, an

unbiased estimatormay be found that attains the bound

if and only if - In that case, is the

MVUEwithvariance

MVUE for the Linear Model - Theorem

- If the observed data can be modeled as ,

- The

MVUEis - And the

covariance matrixof is - For the

linear model, theMVUEisefficientin that attains theCRLB - Also, the statiscal performance of is completely specified, because is a

linear transformationof aGaussian vectorand hence

Finding the MVUE so far

- When the observations and the data are related in a

linear way, - and the noise was

Gaussian, then theMVUEwas easy to find:withcovariance matrix, - Using the

CRLB, if you got lucky, then you could writewhere would be yourMVUE, anefficient estimator(meet theCRLB) - Even if

no efficient estimatorexists, anMVUEmay exist - In this section, we try to find a systematic way of determining the

MVUEif it exists

Finding the MVUE

- We wish to estimate the parameter(s) from the observations

- Step 1

- Determine (if possible) a

sufficient statisticfor the parameter to be estimated - This may be done using the

Neyman-Fisher factorization theorem

- Determine (if possible) a

- Step 2

- Determine whether the

sufficient statisticis alsocompleteThis is generally hard to do

- If it is

not complete, we can say nothing more about theMVUE - If it is, continue to

Step 3

- Determine whether the

- Step 3

- Find the

MVUEfrom is one of two ways using the

Rao-Blackwell-Lehmann-Scheffe(RBLS) theoremRao-Blackwell-Lehmann_Scheffe(RBLS) theorem

- Find a function of the

sufficient statisticthat yields anunbiasedestimator , theMVUE - By definition of

completenessof the statistic, this will yield theMVUE - Find any

unbiasedestimator for , and then determine

- This is usually very tedious/difficult to do

- The expectation is taken over the distribution

- Find a function of the

- Find the

- Step 1

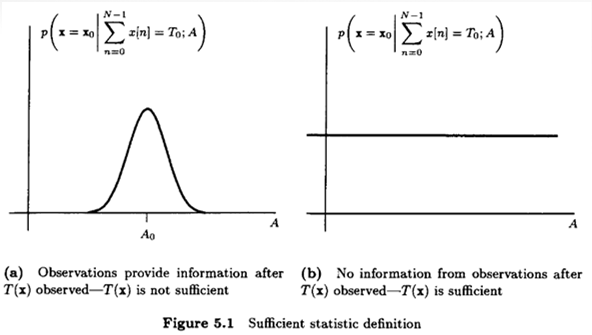

Sufficient Statistics

- Example : Estimating a DC Level in WGN

- :

MVUEwithvariance - :

unbiasedestimator withvariance

disarded the data points which carryinformationabout

- :

- Is there a set of data that is

sufficient?- :

sufficient statistic

(Original data set is alwayssufficient) - :

sufficient statistic - :

minimalsufficient statistis (least # of elements)

- :

- For estimation of , once we know , we

no longer needthe individualdatavaluesSince

all informationhas been summarized in thesufficient statistic - A statistic is the result of applying a function to a set of data - our observations

- A

single statisticis asingle functionof the observations, - And it is called

sufficient statisticsif the PDF isindependentof

- Example : Estimating a DC Level in WGN

- Conditional PDF should

not dependon

- Verification of a

sufficient statisticThen,Independentof the parameter

→ issufficient statisticfor the estimation of

- Evaluation of the

conditional PDFis difficult Guessinga potentialsufficient statisticsis even more difficult- General framework to find

sufficient statistic:Neyman-Fisher facorization

Neyman-Fisher Factorization

- If we can factor the PDF aswhere is a function depending on only through and is a function

dependingonly on - Then is a

sufficient statisticfor - Conversely, if is a

sufficient statisticfor , then the PDF can be factored as in the above equation - Proof : Appendix 5A

Example 1

- Example : Estimating a DC Level in WGN

- Note that any one-to-one function of is a

sufficient statistic

Example 2

- Example : Power of WGN

is theunknown parameter

Naturally Extended Neyman-Fisher Factorization

- The statistics are

joint sufficient statistics

if the conditional pdf does not depend on - They are

joint sufficient statisticsif and only if the pdf may be factored as - The original data are always

sufficient statistics

Phase Examples

- The exponent may be expanded as

- No single

sufficient statisticexists, butjointly sufficient statisticsexist

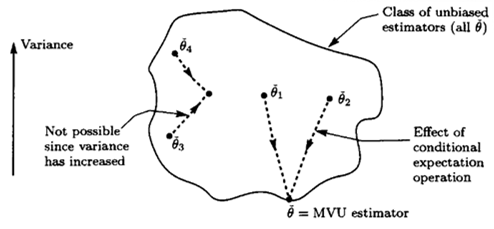

Sufficient Statistics and MVUEs

-

If we determined a

sufficient statisticfor -

Then we can use this to improve any

unbiased estimatorof -

As is proven in the

Rao-Blackwell-Lehmann-Scheffe(RBLS) theorem -

If we're lucky and the statistic is also

complete, we can use it to find theMVUE- There are many definitions for the

completenessof a statistic

One that is easy for us to use in the context of estimation is the following :It is called

completeif only 1 function of it yields anunbiased estimatorof

- This is generally difficult to check but is easy conceptually

- Another way of checking if a statistic is

complete:

- A statistic is

completeit contains above for all is only

satisfied by for all

- There are many definitions for the

Example : DC Level in WGN

- Suppose we don't know that the sample mean is

MVUE, but know thatis asufficient statistic - Two ways to find the

MVUE:- Find any

unbiased estimatorof , say , and determine

The expectation is taken with respect to - Find some function so that is an

unbiasedestimator of

- Find any

First Approach to find

- For

jointly Gaussian random variablesand(Appendix 10A)

Second Approach

- For

unbiased

Rao-Blackwell-Lehmann-Scheffe(RBLS) Theorem

- If is an

unbiased estimatorof and is asufficient statisticfor ,

Then- A valid estimator for (not dependent on )

Unbiased- Of lesser or equal variance thant that of , for all

- Additionally, if the

sufficient statisticiscomplete, then is theMVUE - A statistic is

completeif there is only one function of the statistic that isunbiased - doesn't depend on by the definition of

sufficient statistic

1is proven - Note that since

- Thus, :

3is proven

- If is

complete, there is only one function of that is anunbiasedestimator- is unique independent of

- for all

- must be an

MVUE

Completenessdepends on the PDF of- This condition is satisfied for the exponential family of PDFs

RBLS Example

Incomplete sufficient statistic- is

sufficient statisticand anunbiased estimatorIs a

MVUE?- Suppose that there exists another function w/ the

unbiasedproperty

and see if - Let , then for all

- Since for all

- satisfies the condition

⇒ based on thesufficient statisticand isunbiased→No

- Suppose that there exists another function w/ the

- Completeness condition is that only the zero function satisfies

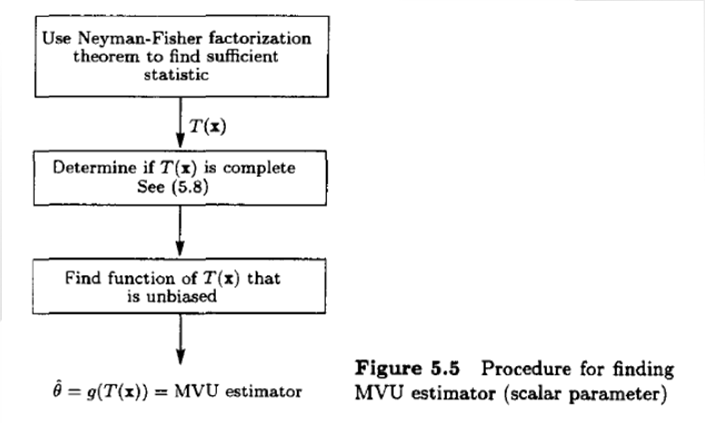

Procedure for finding

MVUE(Scalar)- Use

Neyman-Fisher Factorizationto findsufficient statistic - Determine if is

complete;

The condition forcompletenessis that only the zero function

satisfies for all - Find a function of that is

unbiased

Then is theMVUE

Or alternatively, evaluate where is anyunbiased estimator

- Use

Example : Mean of Uniform Noise

- Consider estimating the mean of the i.i.d. uniform noise

- Find an

efficient estimator- The

regularity conditiondoes not hold :CRLBcannot be applied - Natural guess : sample mean estimator

- Is the sample mean estimator

MVUE?

- The

- Follow Figure 5.5 unit step function

- :

sufficient statisticfor , and alsocomplete - Next, we need to find a function of that is

unbiased - To make this

unbiasedThe sample mean estimator was not theMVUE - Smaller than the variance of sample mean estimator for

- Not easy to apply when there is no single

sufficient statistic

Extensions to Vector Parameters

- If we can factor the PDF as

- is a function

depending ononly through , an statistic - And is function

depending on - Then is a

sufficient statisticfor - Conversely, if is a

sufficient statisticfor , then the PDF can be factored as above - Sufficiency : is

sufficientfor the estimation of if

RBLS

- If is an

unbiasedestimator of and is ansufficientstatistic for

Then is- A valid estimator for ( not dependent on )

Unbiased- Of lesser or equal variance than that of (each element of has less or equal variance)

- Additionally, if the

sufficient statisticiscomplete

then is theMVUECompleteness: if for , an arbitrary function of- for all , then for all

AI, Security