1. Market Power

- So far, we have assumed that no market participant has the ability to

influence the marke tpricethrough its individual actions - A market where all participants act as

price takersis said to haveperfect competition- Achieving or approximating

perfect competitionis a verydesirable goalfrom a global perspective because it ensures that themarginal costof production isequalto themarginal valueof the goods to the consumers - In

perfectly competitive market, themarket priceis a parameter over which firms have no control - Each firm should

increase its productionup to the point where itsmarginal costis equal to themarket price

- Achieving or approximating

- When competition is

not perfect, each firm must consider how thequantityit produces might affect themarket price

2. Monopoly

-

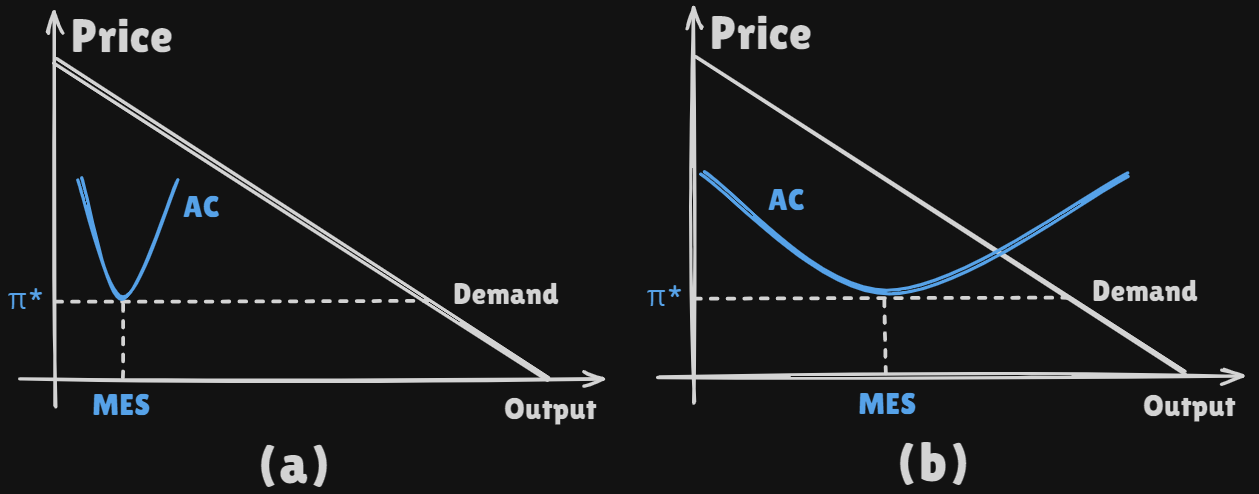

The

minimum efficient size(MES) of a firm in a particular industry provides a rough indication of the number of competitors that one is likly to find in the market for the product of this industry -

The shape of this curve is determined by the

technology used to producethe goods

- On (a), the

MESis muchsmallerthan thedemandfor the goods at thisminimum average cost, the market should be able to support alasrge number of competitors - On (b), the

MESis comparable to thedemand, the market cannot support two profitable firms andmonopoly situationis likely to develop

- On (a), the

-

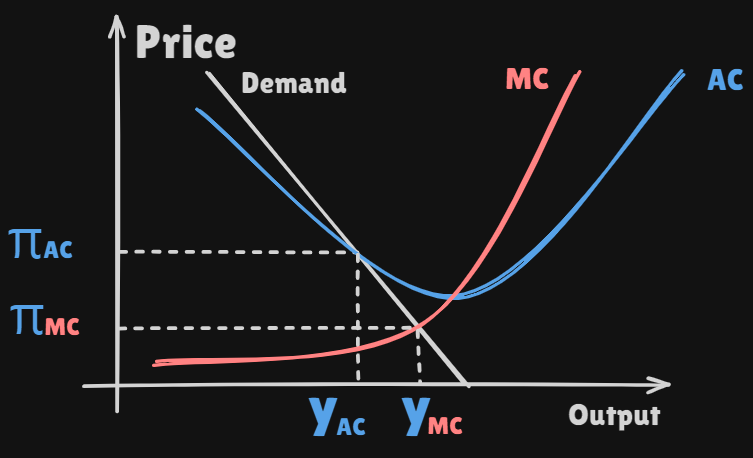

A

monopolistwill reduce itsoutputand raise itspriceabove itsmarginal costof productions to maximize its profit -

From a

global perspective, this isnot satisfactorybecause consumers purchase less of the goods than if they were sold on acompetitive basis

- The

intersectionof thedemandandmarginal cost curvegives a price that islowerthan theaverage costof production- To avoid driving the monopolist out of busincess, the

regulatormust set thepriceat leat at the value given by theintersectionof thedemand curveand theaverage cost curve - Such a situation is called a

natural monopoly

- To avoid driving the monopolist out of busincess, the

AI, Security