Lag-Llama: Towards Foundation Models for Probabilistic Time Series Forecasting

General purpose foundation model for univariate probabilistic time series forecasting

Use lags as covariates

Lag-Llama is pretrained on a large corpus of diverse time series data from several domains

1. Introduction

General purpose foundation model for univariate probabilistic time series forecasting

Statistical models

- Shortfall lies in their inherent assumption of linear relationships and stationarity

- May require extensive manual tuning and domain knowledge to select appropriate models and parameters

Foundation models

- Time-LLM, LLM4TS, GPT2 freeze LLM encoder backbones while simultaneously fine-tuning the input and distribution heads for forecasting

- Main goal of our work is to apply the foundation model approach to time series data

3. Probabilistic Time Series Forecasting

Univariate time series dataset

- Dtrain={x1:Tii}i=1D

- t∈{1,…,Ti}

- Ti : length of the time series i

- Predict the values at the future P

- Dtest={xTi+1:Ti+Pi}i=1D

Univariate probabilistic time series forecasting problem

= Modelling an unknown joint distribution of the P future values

- ϕ : paramters of a parametric distribution

- Rather than considering the whole history of each time series i,

we can instead sub-sample fixed context windows of size C

Predictions are conditioned on these learned parameters θ

4. Lag-Llama

- When training on heterogenous univariate time series corpora, the frequency of the time series in our corpus varies

- When adapting model to downstream datasets, may encounter new frequencies and combinations of seen frequencies

→ General method for tokenizing series from such a dataset, without directly relying on the frequency of any specific dataset

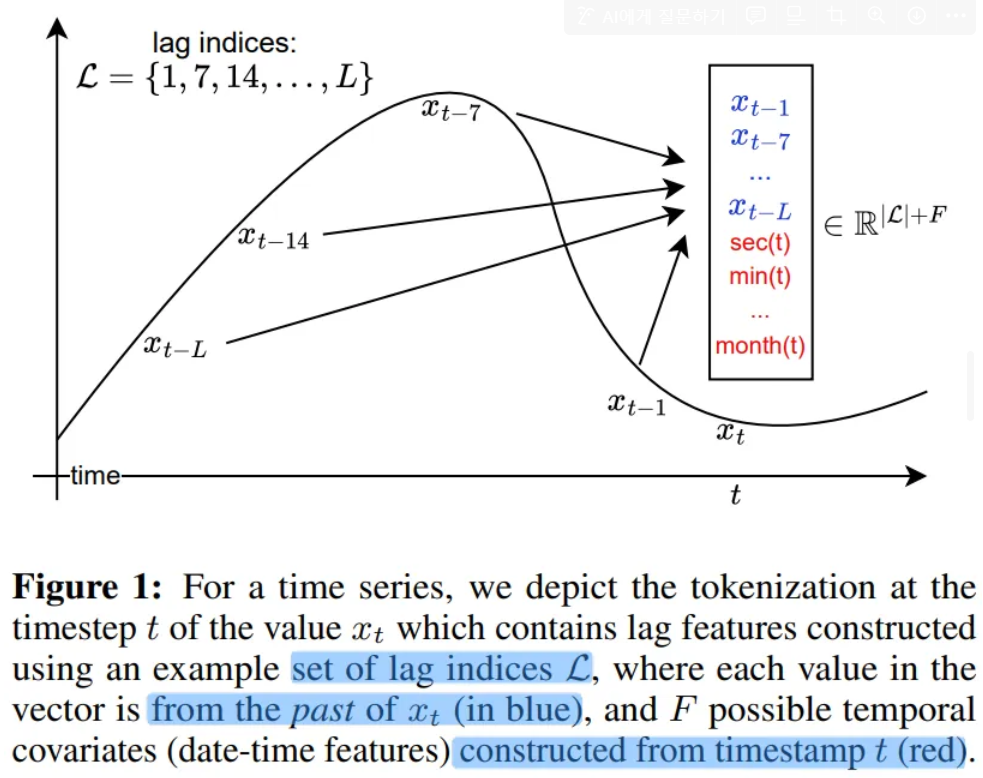

4.1. Tokenization : Lag Features

- Construct lagged features from the prior values of the time series

- Lag indices include quarterly, monthly, weekly, daily, hourly and second-level frequencies

To create lag features for some context-length window x1:C,

- Sample a larger window with L more historical points

- To these lagged features, add date-time features of all the frequencies

second of minute, hour of day etc. (Real time values of data) till the quarter of year from the time index t

- All except one date-time feature will remain constant from one time-step to the next and from the model can make sense of the frequency of the time series

- F : total of date time features

- → Each of tokens is of size £+F

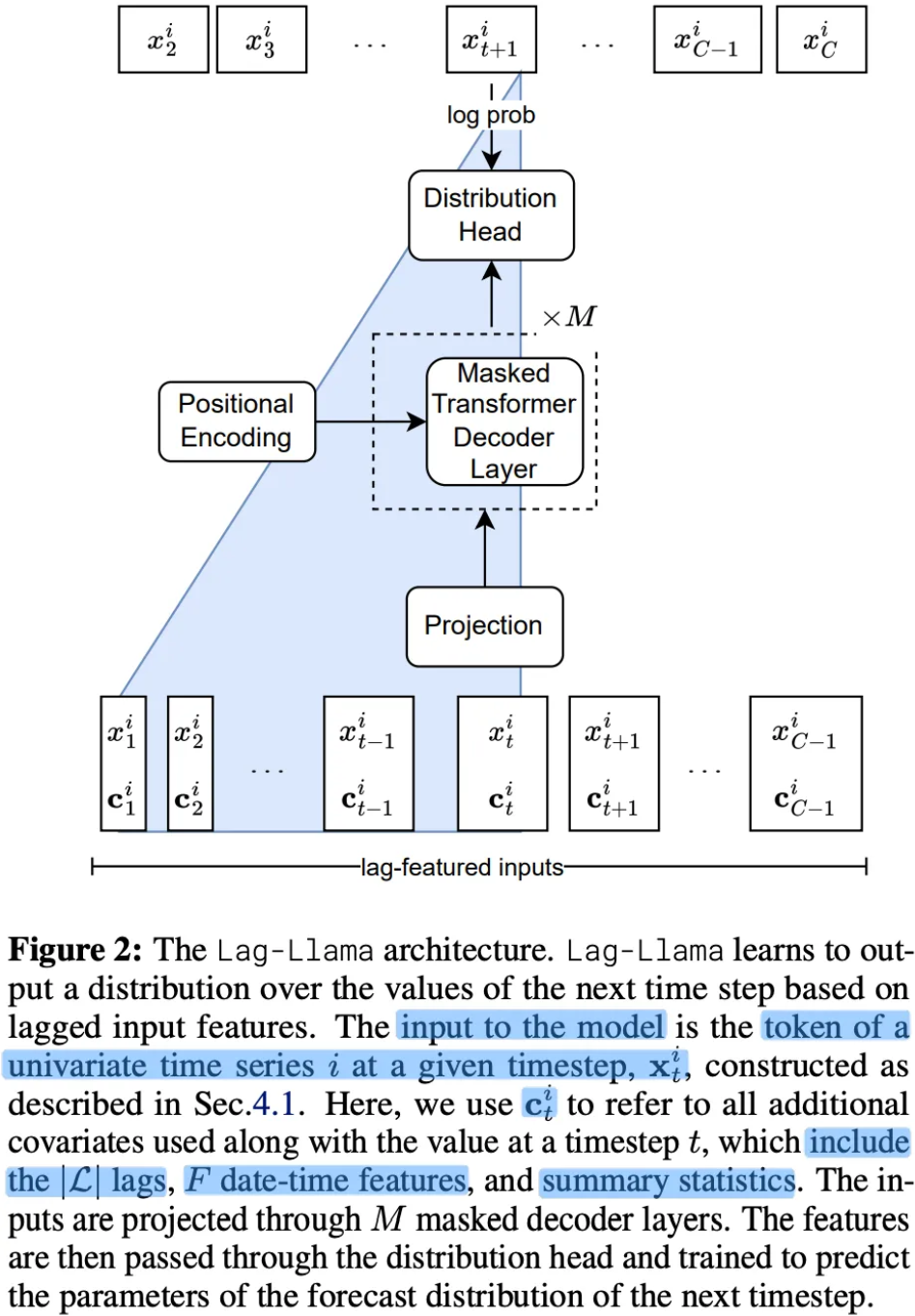

4.2. Lag-Llama Architecture

- A univariate sequence of length along with its covariates is tokenized by concatenating the covariates vectors to a sequence of C tokens

- Tokens are passed through a shared linear projection layer

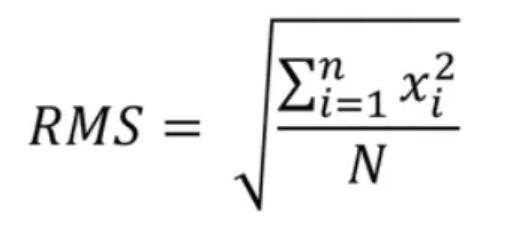

- RMSNorm and Rotary Positional Encoding at each attention layer’s query and key representations

RMSNorm

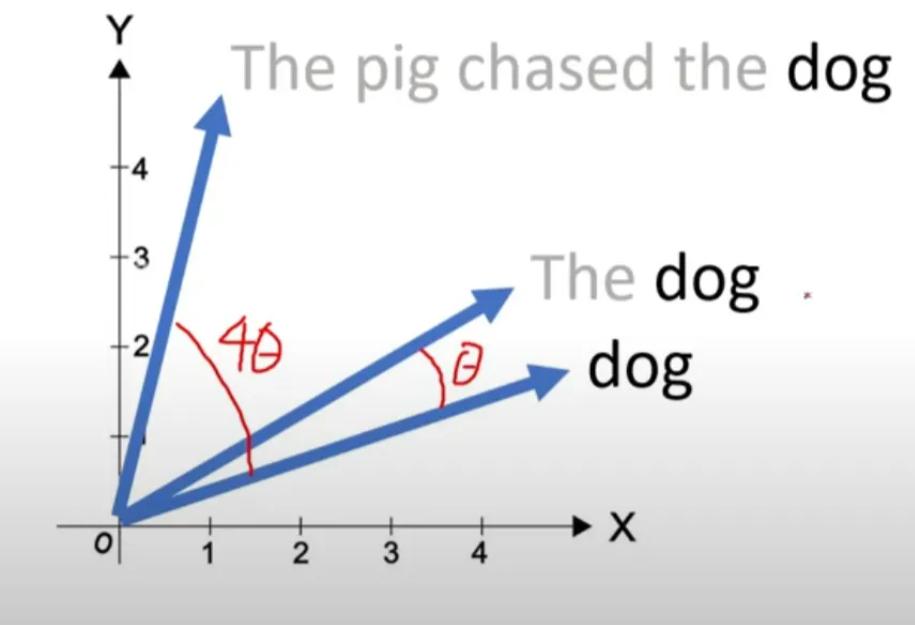

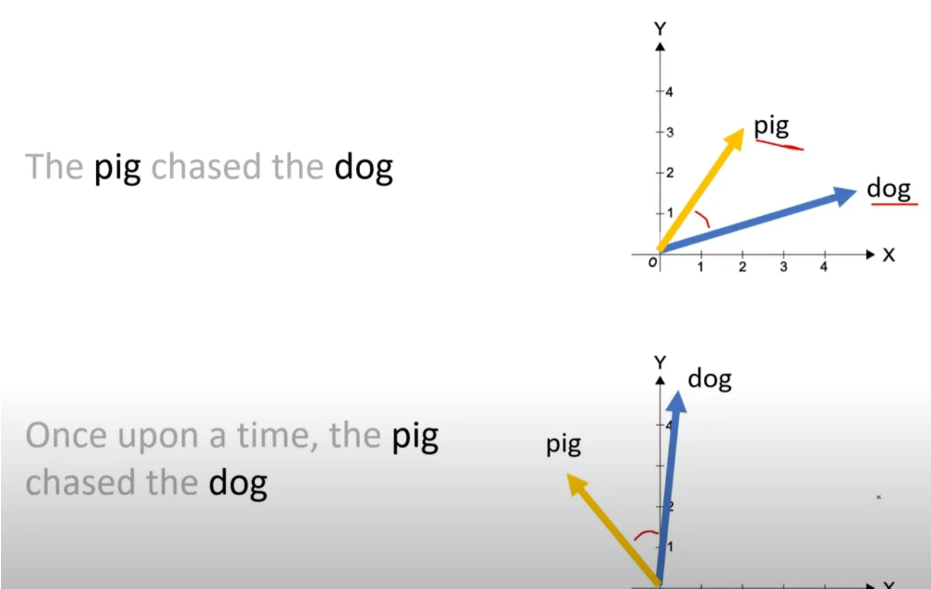

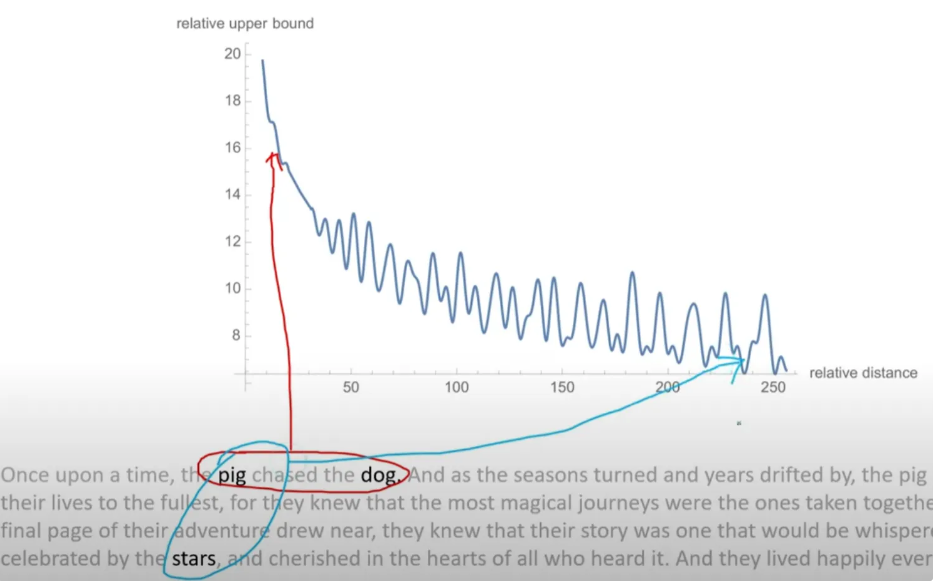

Rotary Positional Encoding

- As long as the distance between the two words stay same

- Multiply rotation matrix after Multiply query and key weight matrix

- Model predicts the parameters ϕ of the forecast distribution of the next timestep

- Parameters are output by a parametric distribution head

4.3. Choice of Distribution Head

- Last layer is the distribution head

which projects the model’s features to the parameters of a probability distribution

- Combine different distribution heads

- Adopt Student’s t-distribution and output the three parameters

Degrees of freedom, Mean, and Scale

- To ensure the parameters stay positive, appropriate non-linearity is used

4.4. Value Scaling

- Utilize the scaling heuristic

- For each univariate window, Calulate its mean and variance

- Scale x1:Ci → {(xti−μi)/σi}t=1C

- Also incorporate μi and σi as covariates for each token,

which we call summary statistics

- During training, values are transformed using the mean and variance,

while sampling, every timestep data is sampled is de-standardized

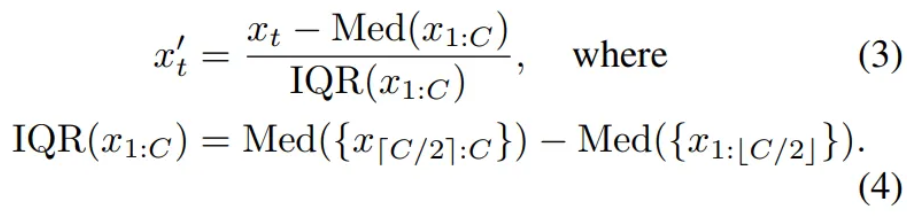

- In practice, instead of the standard scaler, Use Robust Standardization

Robust Standardization

4.5. Training Strategies

- Corpus are weighed by the amount of total number of series

- Augment with Freq-Mix and Freq-Mask

5. Experiment Setup

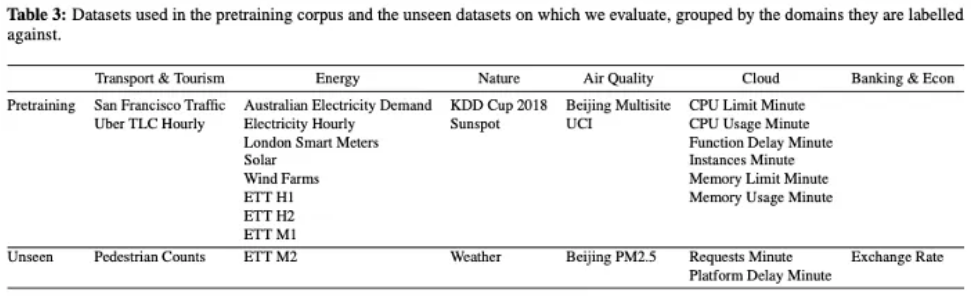

5.1. Datasets

- Corpus of 27 time series datasets from six different domains

- Leave out a few datasets from each domain for testing the few-shot

- 7965 univariate time series

5.3. Model Training Setup

- Each epoch consists of 100 randomly sampled windows

- Since model is decoder-only and since prediction length is not fixed

the model can work for any downstream prediction length

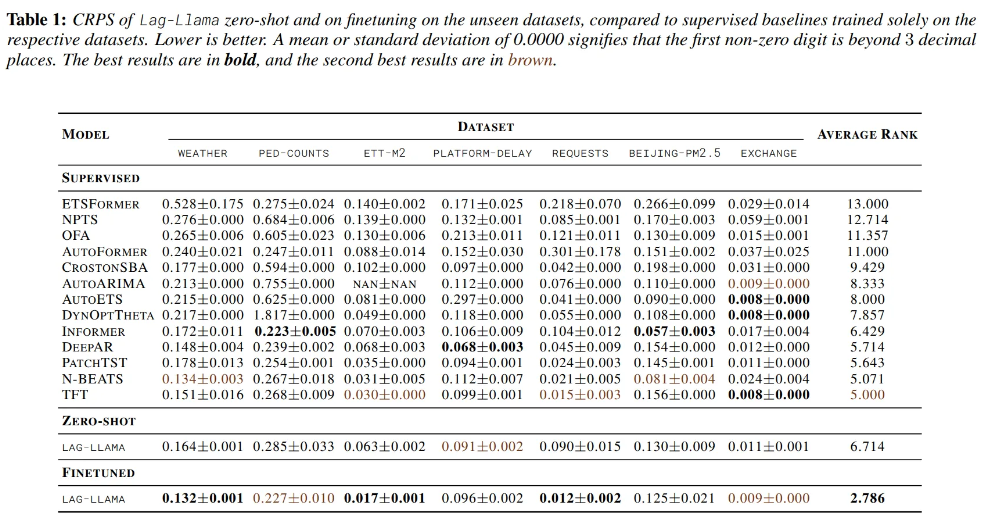

6. Results

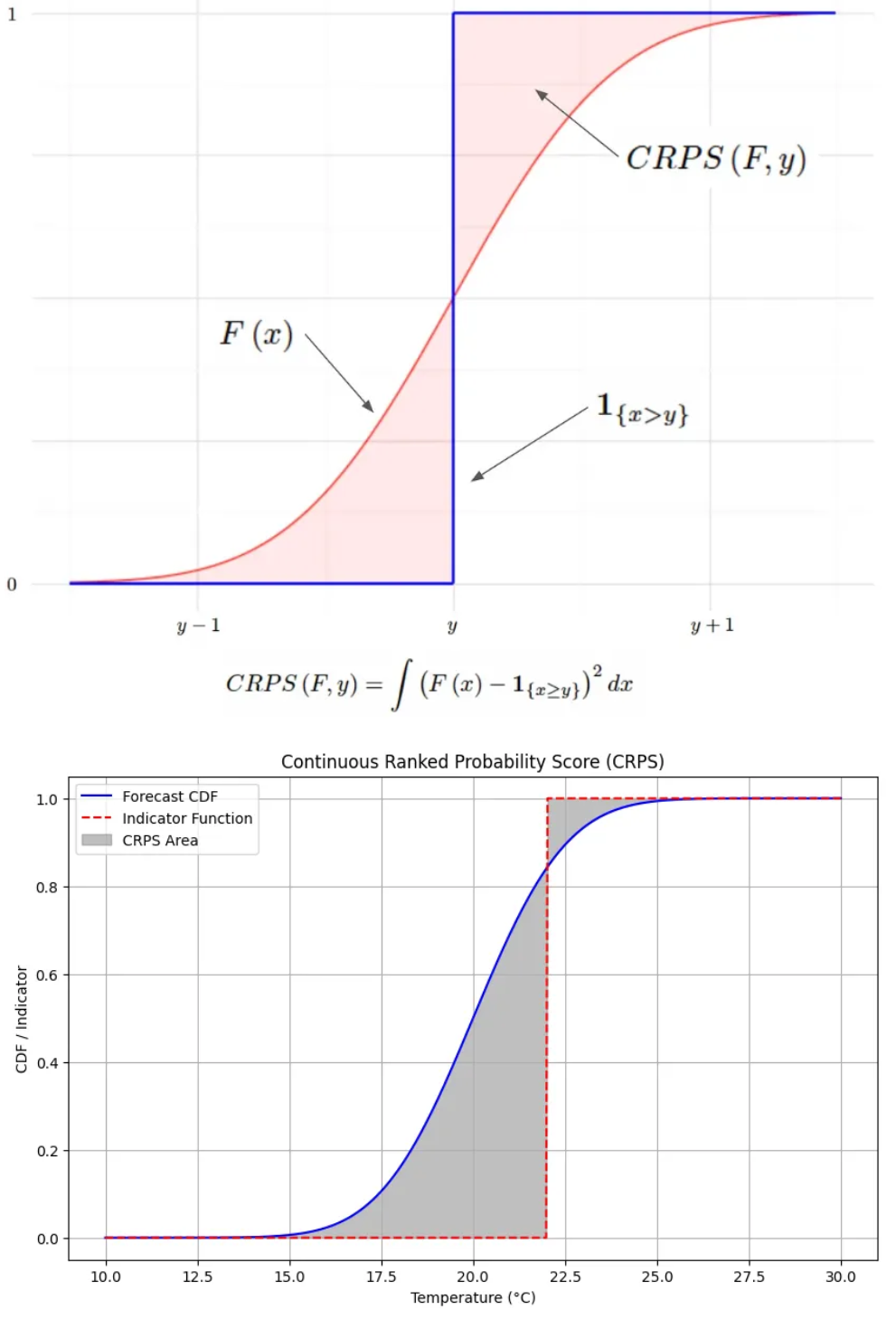

CRPS

- μ=20,σ=2

- Observed value = 22

6.1. Zero-shot

- Exchange-rate is an entirely new domain

- Inductive bias

- Vanilla decoder-only transformers outperform other transformer architectures

- As inductive bias gets larger, it performs well with smaller datasets

- Simple models with smaller inductive bias perform better when trained on large datasets.

- Compared to the OneFitsAll which adapts a pretrained LLM for forecasting, Lag-Llama achieves better performance

- Demonstrate the potential of foundation models trained from scratch compared to the adaptation of pretrained LLM

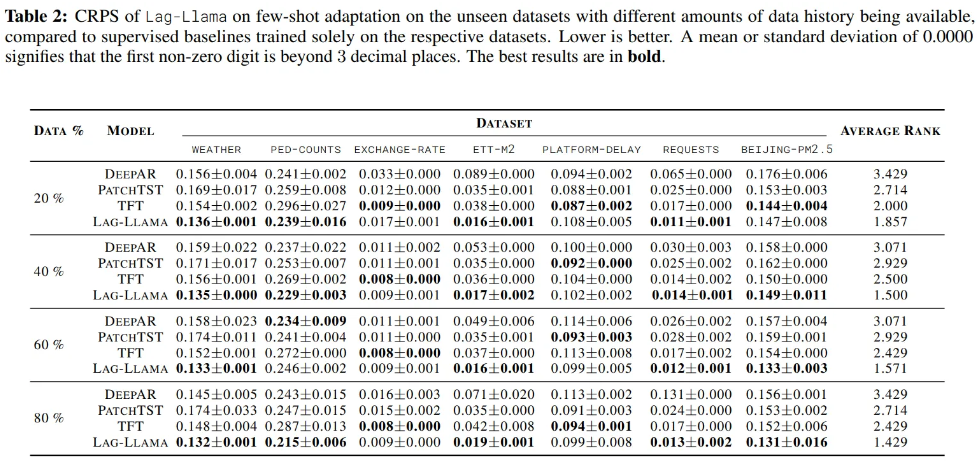

6.2. Few-shot

- Exchange-rate is entirely new domain and new unseen frequency

- most dissimilar as compared to the pretraining corpus

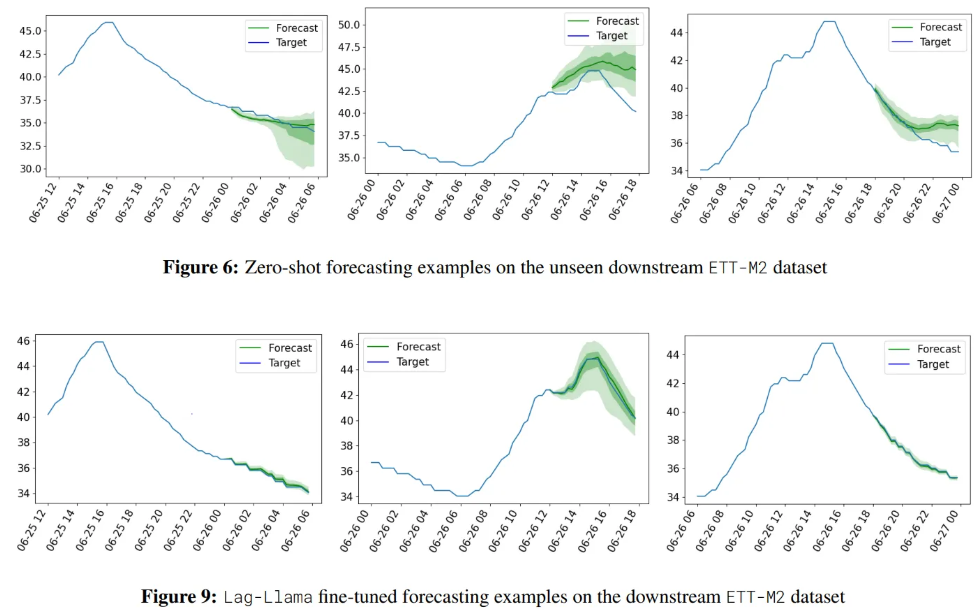

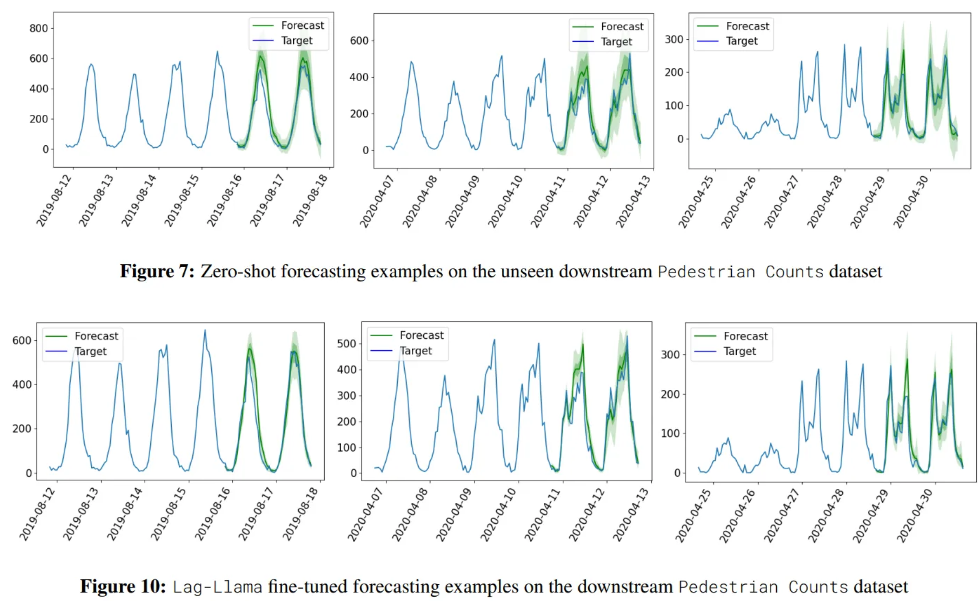

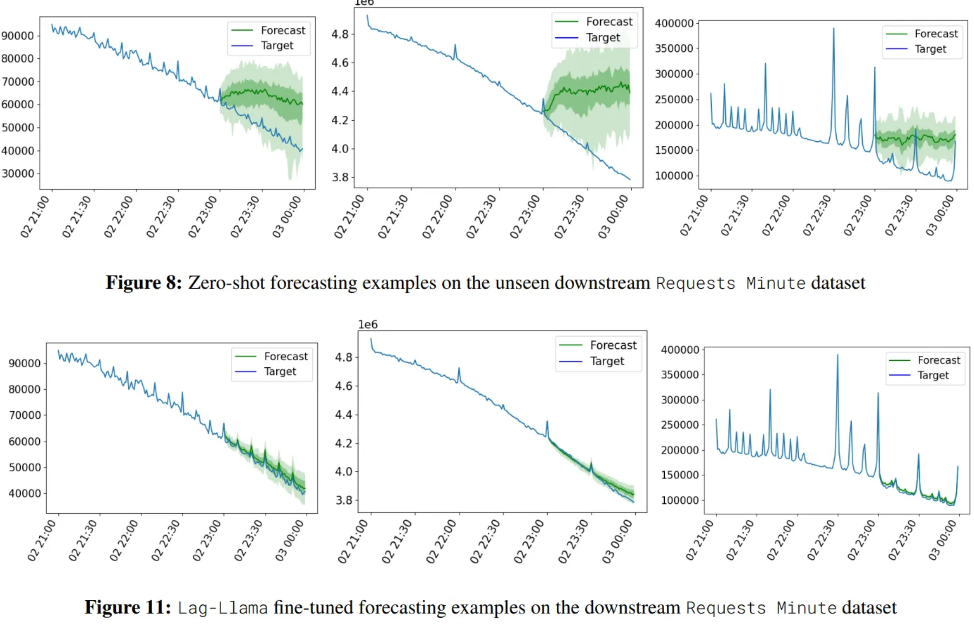

Visualization