3. 성별, 연령, 신용카드 이용 연수에 대한 EDA

3.1 성별에 따른 EDA

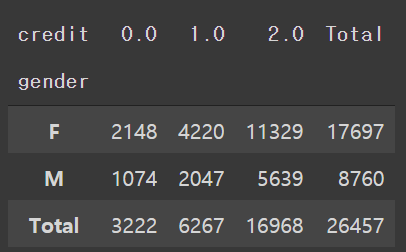

# 성별에 따른 신용등급 인원수

pd.crosstab(train['gender'], train['credit'], margins=True, margins_name='Total')

- 여성고객이 남성고객보다 많다.

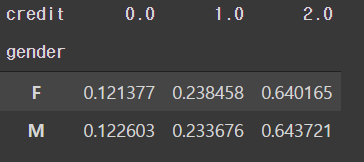

# 성별에 따른 신용등급 비율

pd.crosstab(train['gender'], train['credit'], normalize='index')

- 성별에 따른 신용등급은 큰 차이를 보이지 않는다.

3.2 연령에 따른 EDA

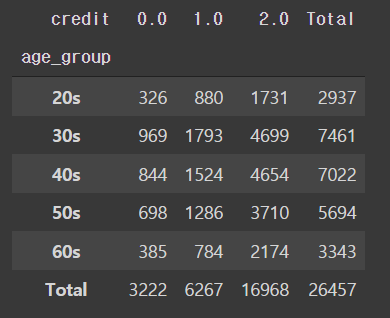

# 연령에 따른 신용등급 인원수

pd.crosstab(train['age_group'], train['credit'], margins=True, margins_name='Total')

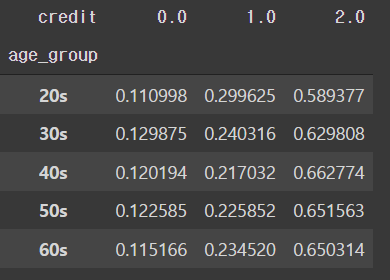

# 연령에 따른 신용등급 비율

pd.crosstab(train['age_group'], train['credit'], normalize='index')

- 연령에 따른 신용 비율이 뚜렷이 보여주는 차이가 없다

3.3 신용카드 이용 연수에 따른 EDA

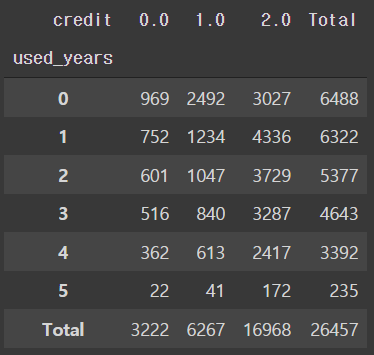

pd.crosstab(train['used_years'], train['credit'], margins=True, margins_name='Total')

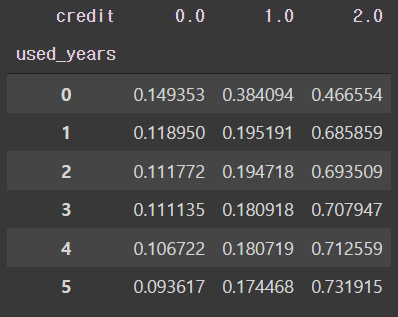

pd.crosstab(train['used_years'], train['credit'], normalize='index')

- 신용카드는 사용 연수가 증가 할 수록 신용등급률이 떨어지는 것으로 보인다.

- 신용카드 사용 첫번째 1년이 지날때 비율이 가장 많이 떨어지고 그 후엔 조금씩 지속적으로 떨어진다.

- 신용 2등급의 경우 처음 1년이 지나고 가장 많이 오른다.

3.4 성별과 연령, 사용 연수에 따른 종합적인 EDA

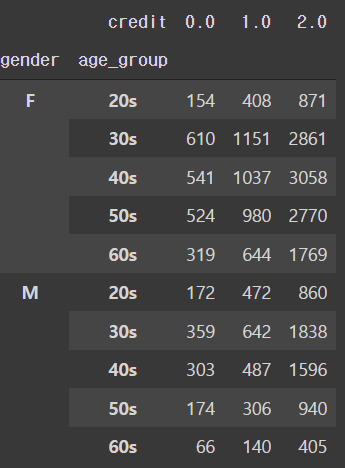

# 성별과 연령대에 따른 신용등급 인원수

pd.crosstab([train['gender'],train['age_group']], train['credit'])

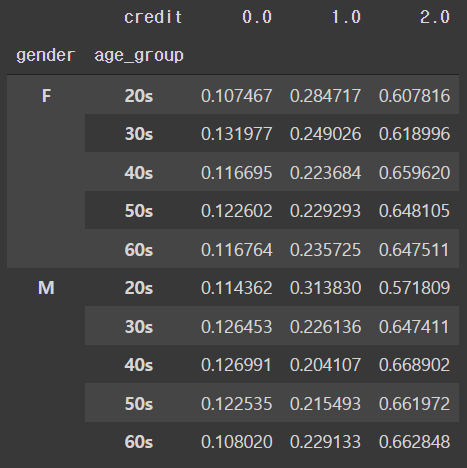

# 성별과 연령대에 따른 신용등급 비율

pd.crosstab([train['gender'],train['age_group']], train['credit'], normalize='index')

- 성별과 연령대에 따른 신용등급의 변화는 뚜렷이 보이는 것이 없다.

3.5 연령과 사용연수에 따른 EDA

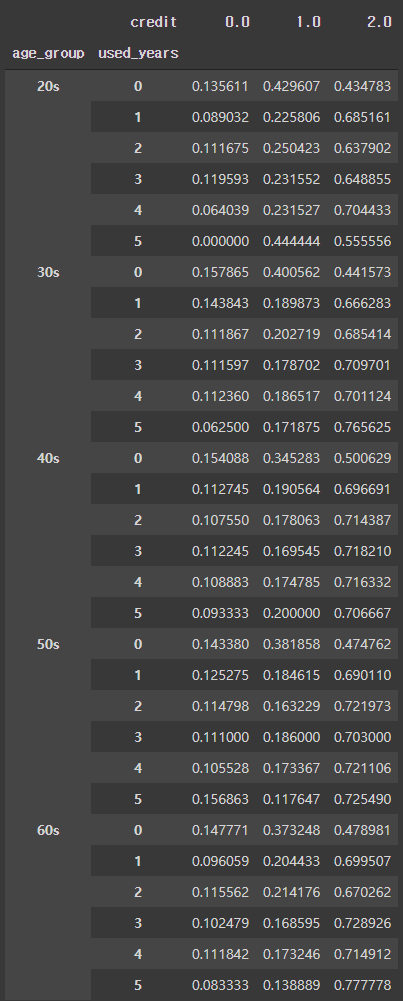

# 연령대와 사용연수에 따른 신용등급 비율

pd.crosstab([train['age_group'],train['used_years']], train['credit'], normalize='index')

- 연령대에 따라 신용카드 이용연수가 증가 할 수록 신용등급 변화가 다르게 나타난다.

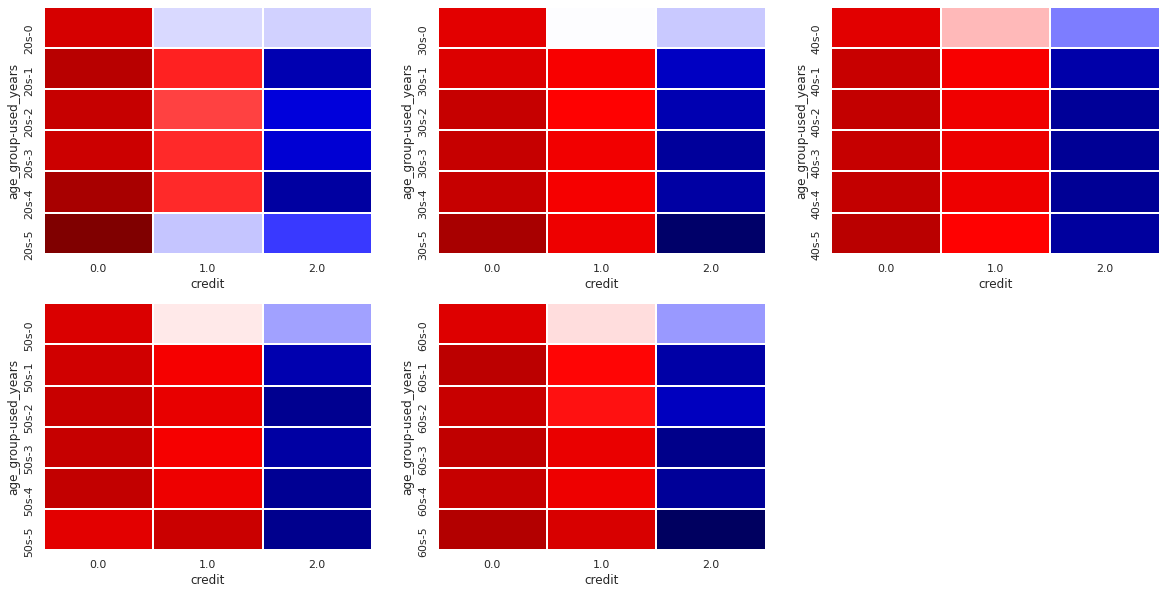

# heatmap에 따른 연령대와 사용연수에 따른 신용등급 비율

## 20s

twenty = train[train['age_group']=='20s']

twentyUsedYear = pd.crosstab([twenty['age_group'],twenty['used_years']], twenty['credit'], normalize='index')

## 30s

thirty = train[train['age_group']=='30s']

thirtyUsedYear = pd.crosstab([thirty['age_group'],thirty['used_years']], thirty['credit'], normalize='index')

## 40s

forty = train[train['age_group']=='40s']

fortyUsedYear = pd.crosstab([forty['age_group'],forty['used_years']], forty['credit'], normalize='index')

## 50s

fifty = train[train['age_group']=='50s']

fiftyUsedYear = pd.crosstab([fifty['age_group'],fifty['used_years']], fifty['credit'], normalize='index')

## 60s

sixty = train[train['age_group']=='60s']

sixtyUsedYear = pd.crosstab([sixty['age_group'],sixty['used_years']], sixty['credit'], normalize='index')# 사이즈 지정

plt.figure(figsize=(20,10))

plt.subplot(2,3,1)

sns.heatmap(twentyUsedYear, vmin=0, vmax=0.8,

linewidths=1, cmap="seismic_r", cbar=False)

plt.subplot(2,3,2)

sns.heatmap(thirtyUsedYear, vmin=0, vmax=0.8,

linewidths=1, cmap="seismic_r", cbar=False)

plt.subplot(2,3,3)

sns.heatmap(fortyUsedYear, vmin=0, vmax=0.8,

linewidths=1, cmap="seismic_r", cbar=False)

plt.subplot(2,3,4)

sns.heatmap(fiftyUsedYear, vmin=0, vmax=0.8,

linewidths=1, cmap="seismic_r", cbar=False)

plt.subplot(2,3,5)

sns.heatmap(sixtyUsedYear, vmin=0, vmax=0.8,

linewidths=1, cmap="seismic_r", cbar=False)

plt.show()

- 짙은 감색일 수록 비율이 높고 짙은 적색일 수록 비율이 낮다.

- 위에 테이블에서 보여준 숫자 상으론 차이가 보이긴 하나 명확하게 어떠한 차이가 있는지 보이지 않는다.

- 후에 modeling을 통한 수치 비교를 해야 할거 같다.

4. 실물 자산에 따른 EDA

4.1 부동산 소유에 따른 신용등급

# 부동산 소유에 따른신용등급 인원수

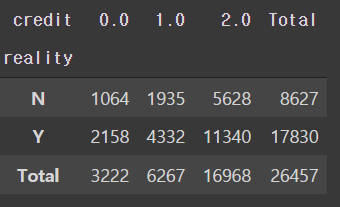

pd.crosstab(train['reality'], train['credit'], margins=True, margins_name='Total')

- 신용카드 사용자 중 대부분은 부동산을 소유하고 있다.

# 부동산 소유에 따른신용등급 비율

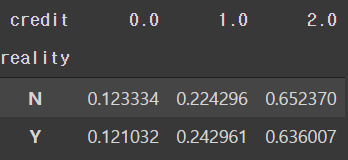

pd.crosstab(train['reality'], train['credit'], normalize='index')

- 비율상 두 level의 차이는 크게 다르지 않다.

4.2 부동산 종류에 따른 신용등급

# 부동산 종류에 따른신용등급 인원수

pd.crosstab(train['house_type'], train['credit'], margins=True, margins_name='Total')

- 대부분의 경우 아파트에 거주하고 있다.

# 부동산 종류에 따른신용등급 비율

pd.crosstab(train['house_type'], train['credit'], normalize='index')

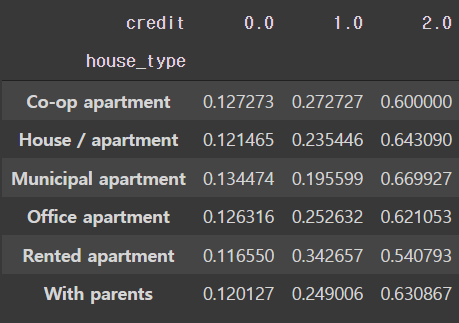

- 비율 상으로 크게 차이가 나는 level은 보이지 않는다.

- Municipal apaetment에 거주 하는 사람들의 경우 신용등급 0과 1의 비율차가 다른 level에 비해 많이 나진 않는다.

- 그러나 Municipal apaetment의 경우 신용등급 2의 비율이 가장 높다.

4.3 자동차 소유에 따른 신용등급

# 자동차 소유에 따른신용등급 인원수

pd.crosstab(train['car'], train['credit'], margins=True, margins_name='Total')

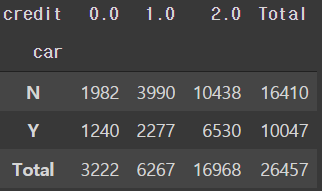

- 자동차를 소유하고 있지 않은 고객이 더 많다.

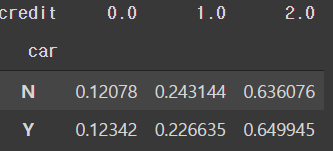

# 자동차 소유에 따른신용등급 비율

pd.crosstab(train['car'], train['credit'], normalize='index')

- 비율적으로 큰 차이가 보이진 않는다.

4.4 연령과 자동차 소유에 대한 신용등급

- 가정: 20대 승용차를 가지고 있을 경우 무리해서 구매 했을 가능성이 있다.

- 따라서 20대 경우 승용차를 소유 하고 있는 그룹과 아닌 그룹간의 차이를 보여줄 수 있다.

# 20대의 차량 소유에 따른 신용등급 비율

pd.crosstab(twenty['car'], twenty['credit'], normalize='index')

- 차량 소유에 따른 신용등급의 비율 차가 많이 나지 않는다

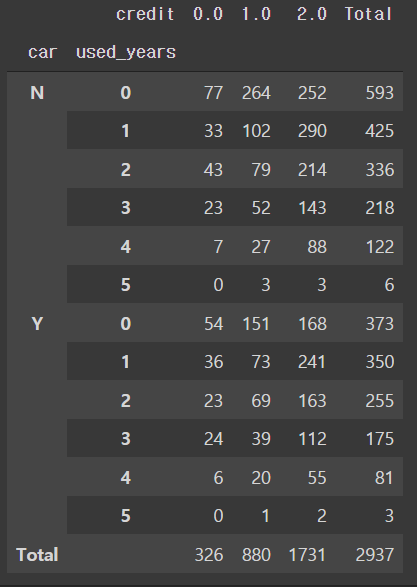

pd.crosstab([twenty['car'], twenty['used_years']], twenty['credit'], margins=True, margins_name='Total')

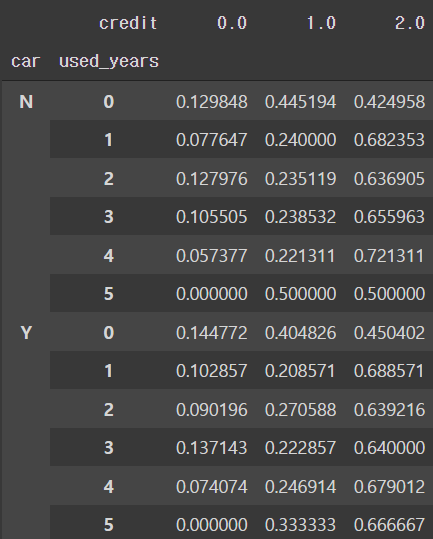

pd.crosstab([twenty['car'], twenty['used_years']], twenty['credit'], normalize='index')

- 싱용카드 사용 연수에 따른 결과 값이 사이즈를 고려 했을시 의미있다 보긴 힘들다.

- 따라서 지금 단계에선 20대가 자동차를 소유했다고해서 신용등급이 영향을 받는다고 결론을 내리긴 힘들어 보인다.

5. 가족 정보에 따른 신용정보

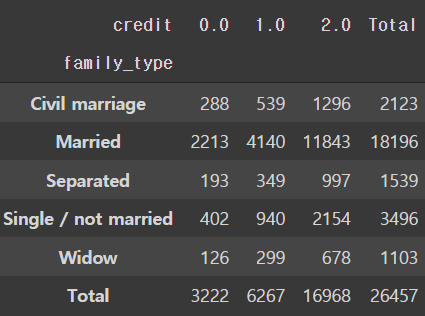

5.1 가족 유형(family_type)에 따른 신용등급

# 가족 유형에 따른 신용등급 인원수

pd.crosstab(train['family_type'], train['credit'], margins=True, margins_name='Total')

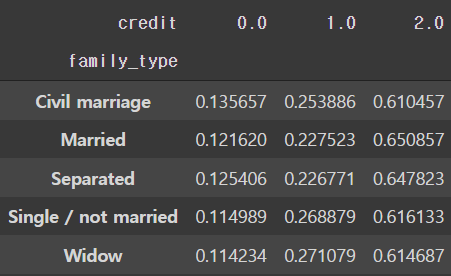

# 가족 유형에 따른 신용등급 비율

pd.crosstab(train['family_type'], train['credit'], normalize='index')

- civil marriage와 married의 경우 같은 값으로 봐도 괜찮을 수 있다.

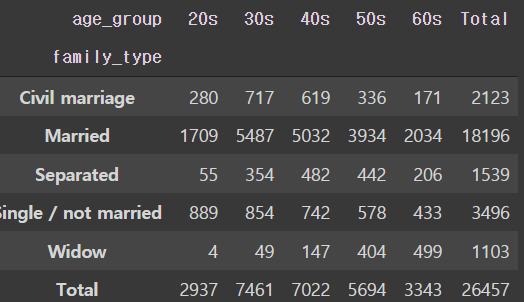

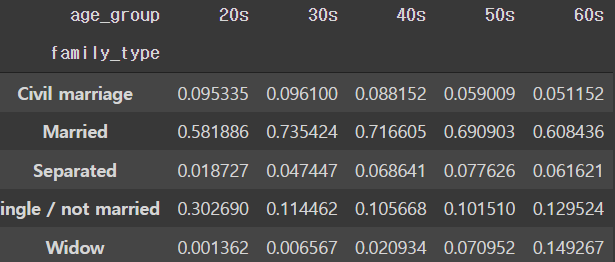

5.1.1 가족 유형과 연령에 따른 비율과 인원수

pd.crosstab(train['family_type'], train['age_group'], margins=True, margins_name='Total')

pd.crosstab(train['family_type'], train['age_group'], normalize='columns')

- 신용카드 회사의 주 고객층은 30대에서 50대 이다.

- 전 연령 층에서 결혼한 고객들의 비율이 가장 높다.

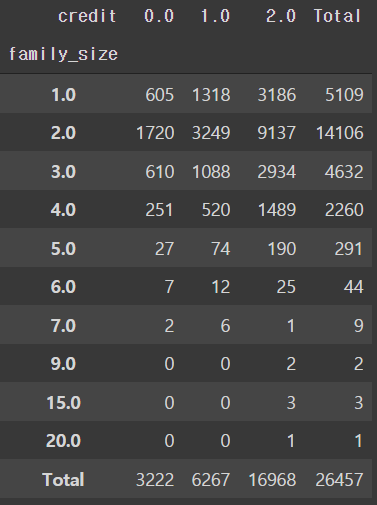

5.2 가족 인원수에 따른 신용등급

# 가족 인원수에 따른 신용등급

pd.crosstab(train['family_size'], train['credit'], margins='total', margins_name='Total')

- 대부분의 고객은 2인가족이다.

- 5인 이상의 고객의 경우 데이터의 사이즈가 작다.

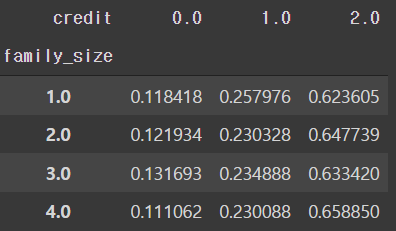

# 가족 인원 1~4명에 따른 신용등급 비율

pd.crosstab(train['family_size'][train['family_size'] < 5], train['credit'], normalize='index')

- 가족 인원수에 따른 신용등급의 유의미한 차이가 현재 보이지 않는다.

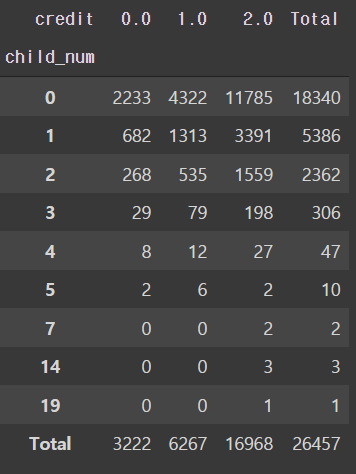

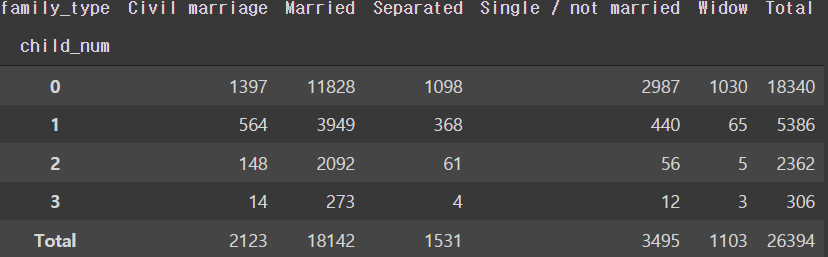

5.3 자녀에 따른 신용등급

# 자녀에 따른 신용등급

pd.crosstab(train['child_num'], train['credit'], margins='total', margins_name='Total')

- 자녀가 3명 이하인 경우에 따른 비율을 보는것이 효율적일 것으로 보인다.

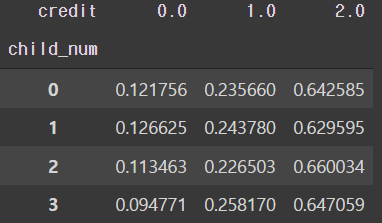

# 자녀에 따른 신용등급

pd.crosstab(train['child_num'][train['child_num']<4], train['credit'], normalize='index')

- 자녀가 3명인 경우 신용등급 0이 다른 그룹에 비해 낮다.

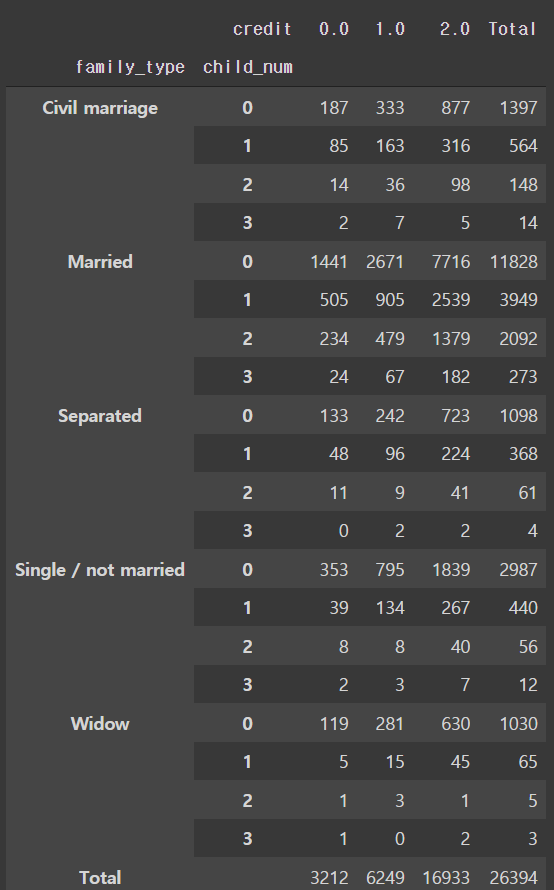

5.3.1 가족 유형과 자녀 명수에 따른 신용등급

# 자녀가 3명 이하인 경우에 따른 가족 유형 인원수

pd.crosstab(train['child_num'][train['child_num']<4], train['family_type'], margins='total', margins_name='Total')

# 자녀가 3명 이하인 경우에 따른 가족 유형 인원수

pd.crosstab([train['family_type'], train['child_num'][train['child_num']<4]],

train['credit'], margins='total', margins_name='Total')

- 각 셀의 인원수를 고려 했을시 자녀수가 2명 이하인 경우가 유의미한 정보를 보여주는 것으로 보인다.

- 가족 유형은 결혼한 인원에 대해서만 보는게 효율적일 것으로 보인다.

6. 직장과 수입에 따른 신용등급

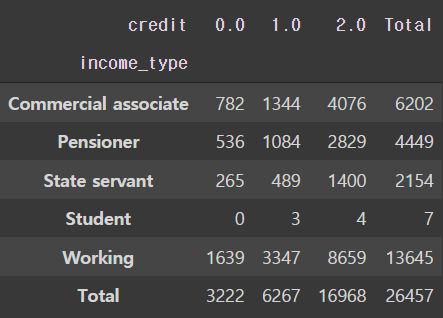

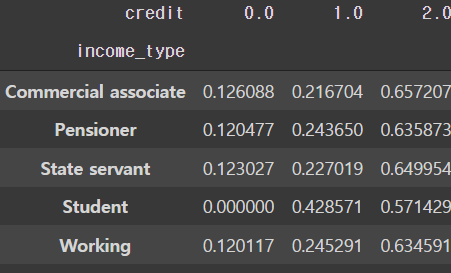

6.1 수입 방식에 따른 신용등급

# income_type에 따른 신용 등급 인원수

pd.crosstab(train['income_type'], train['credit'], margins='total', margins_name='Total')

# income_type에 따른 신용 등급 비율

pd.crosstab(train['income_type'], train['credit'], normalize='index')

- 학생의 경우 절대적인 인원수가 적어 의미 있는 정보를 찾아보기 힘들다.(후에 학생에 대한 값들은 드롭하는 것이 좋을 수 있다.)

- 다른 변수들의 경우 비슷한 트렌드를 보인다.

6.2 수입에 따른 신용등급

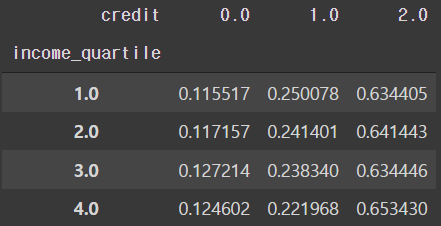

# 4분위에 대한 정보

pd.crosstab(train['income_quartile'], train['credit'], normalize='index')

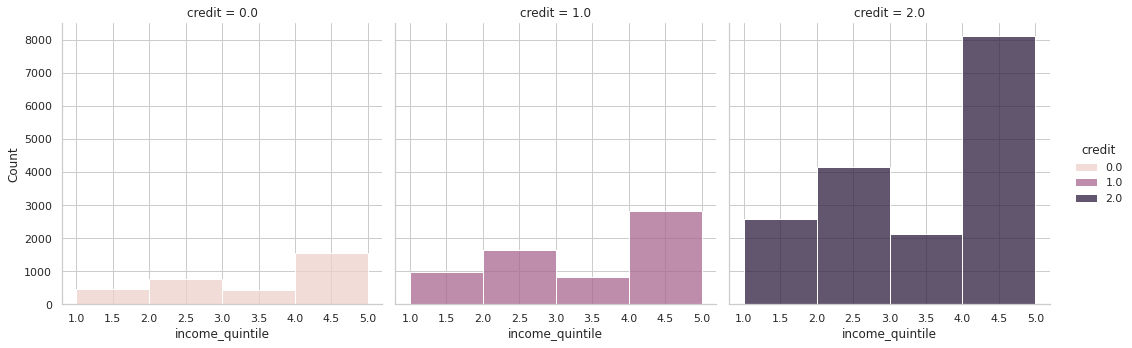

sns.displot(x='income_quintile', hue='credit', multiple='stack', col='credit', bins=4, data=train)

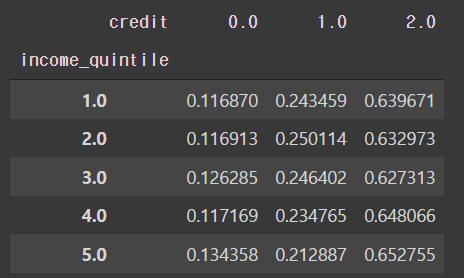

# 5분위에 대한 정보

pd.crosstab(train['income_quintile'], train['credit'], normalize='index')

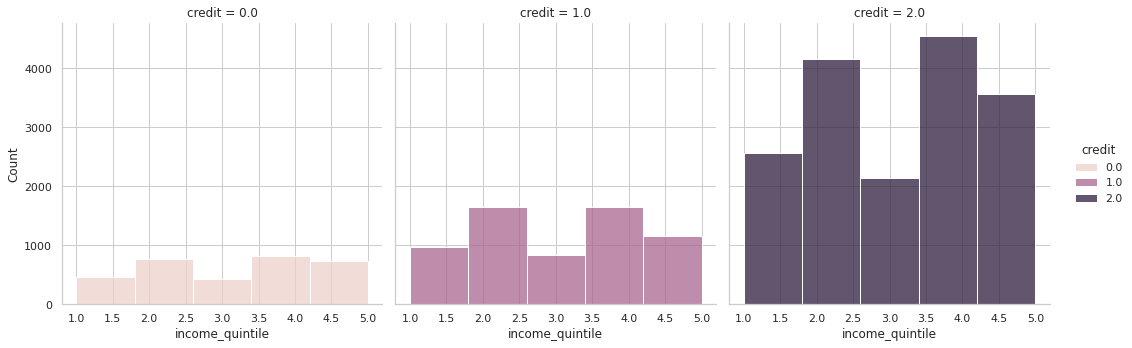

# 5분위에 따른 신용 등급

sns.displot(x='income_quintile', hue='credit', multiple='stack', col='credit', bins=5,data=train)

# 10분위에 대한 정보

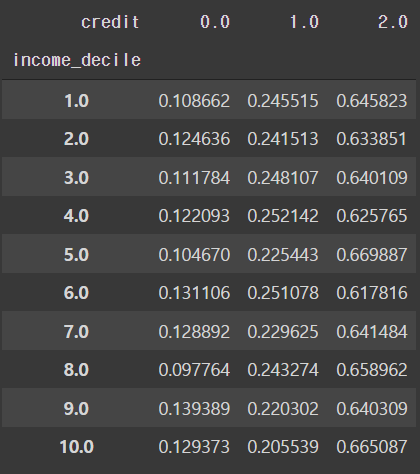

pd.crosstab(train['income_decile'], train['credit'], normalize='index')

# 10분위에 따른 신용 등급

sns.displot(x='income_decile', hue='credit', multiple='stack', col='credit', bins=10,data=train)

- 현재 4, 5, 10분위에 따라 나누어진 신용 등급표에 의하면 어느 특정 분위수의 그룹이 상대적으로 높게 평가되거나 하진 않는다.

- 수입에 따른 신용등급은 의미가 없을 수도 있다.

6.3 근무 연수에 따른 신용등급

# 근무 연수에 대한 정보

train['worked_year'].describe()

## -1은 무직자를 말한다.

count 26457.000000

mean 5.441736

std 6.581967

min -1.000000

25% 1.000000

50% 4.000000

75% 8.000000

max 43.000000

Name: worked_year, dtype: float64creditZero = train[train['credit']==0]

creditOne = train[train['credit']==1]

creditTwo = train[train['credit']==2]plt.figure(figsize=(25, 8))

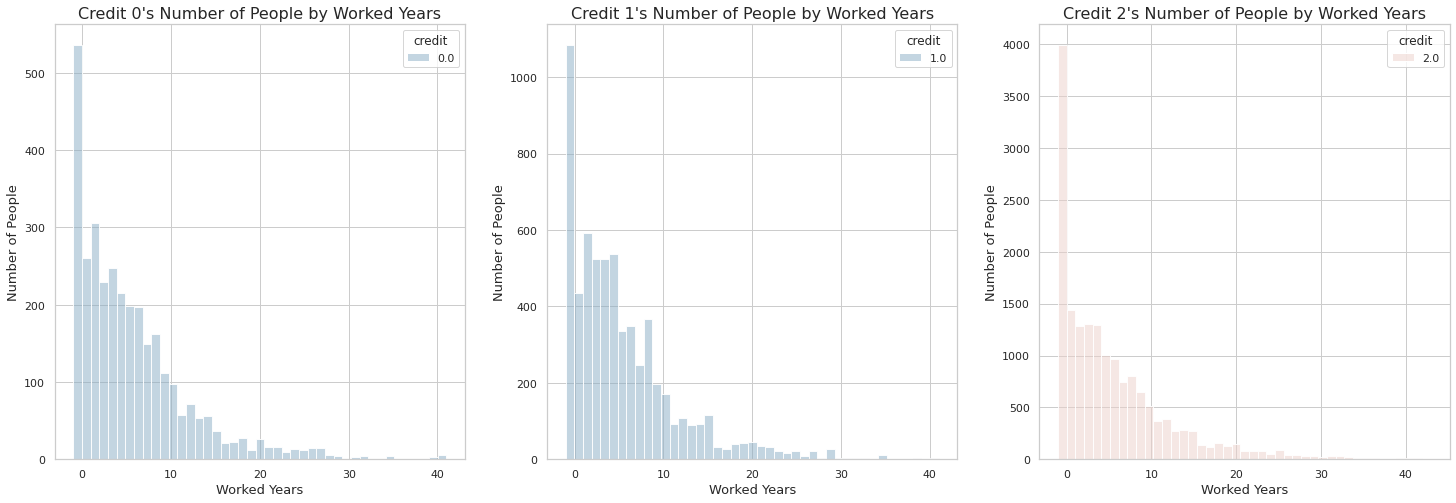

# 근무 연수에 따른 신용 등급 0의 인원수

plt.subplot(1, 3, 1)

creditZeroPlot = sns.histplot(x='worked_year', hue='credit', bins=43, data=creditZero)

creditZeroPlot.set_xlabel('Worked Years', fontsize=13)

creditZeroPlot.set_ylabel('Number of People', fontsize=13)

creditZeroPlot.set_title("Credit 0's Number of People by Worked Years", fontsize=16)

# 근무 연수에 따른 신용 등급 1의 인원수

plt.subplot(1, 3, 2)

creditOnePlot = sns.histplot(x='worked_year', hue='credit', bins=43, data=creditOne)

creditOnePlot.set_xlabel('Worked Years', fontsize=13)

creditOnePlot.set_ylabel('Number of People', fontsize=13)

creditOnePlot.set_title("Credit 1's Number of People by Worked Years", fontsize=16)

# 근무 연수에 따른 신용 등급 1의 인원수

plt.subplot(1, 3, 3)

creditTwoPlot = sns.histplot(x='worked_year', hue='credit', bins=43, data=creditTwo)

creditTwoPlot.set_xlabel('Worked Years', fontsize=13)

creditTwoPlot.set_ylabel('Number of People', fontsize=13)

creditTwoPlot.set_title("Credit 2's Number of People by Worked Years", fontsize=16)

plt.show()

- 전체적인 트랜드를 봤을 때 근무 연수가 올라간다 하여 신용등급이 올라가지는 않는 것으로 보인다.

- 위에서 본 연령별 신용카드 사용자를 보면 50대와 60대의 경우 다른 연령에 비해 사용자가 적다.

- 따라서 근무연수가 올라갈 수록 전체적인 신용등급에 따른 인원이 적은 것으로 보인다.

- 흥미로운점은 무직자가(-1) 신용등급 0에 가장 많다는 것이다.

따라서 근무 연수와 상관없이 신용등급이 결정될 수 있다는 가정이 생긴다.

6.4.1 성별과 근무연수에 따른 신용등급

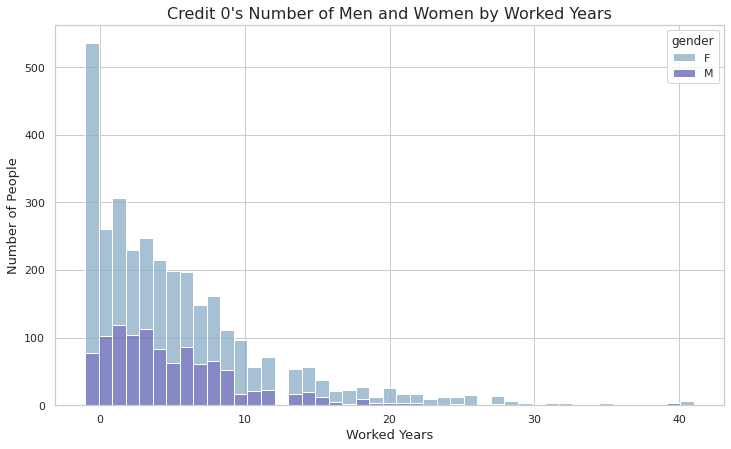

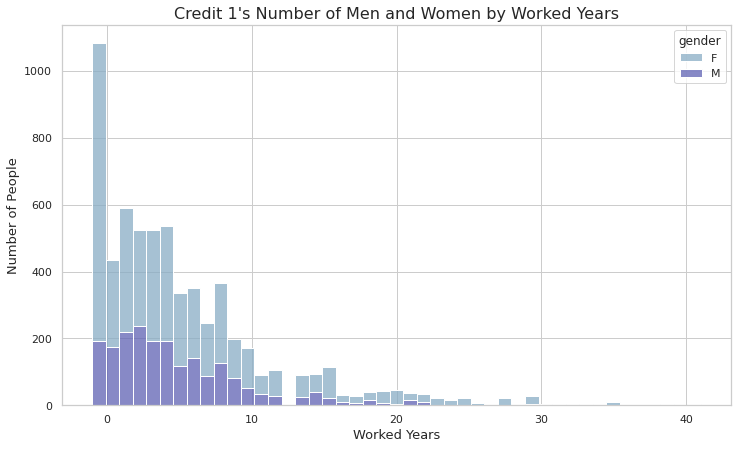

# 성별에 따른 신용등급 0의 인원수

plt.figure(figsize=(12,7))

genderCreditZero = sns.histplot(x='worked_year', hue='gender', multiple='stack', bins=45, data=creditZero)

genderCreditZero.set_xlabel('Worked Years', fontsize=13)

genderCreditZero.set_ylabel('Number of People', fontsize=13)

genderCreditZero.set_title("Credit 0's Number of Men and Women by Worked Years", fontsize=16)

plt.show()

- 신용등급 0 에 대해서 여성의 경우 근무를 하지 않는 그룹이 가장 많은 비중을 차지하고 있다.

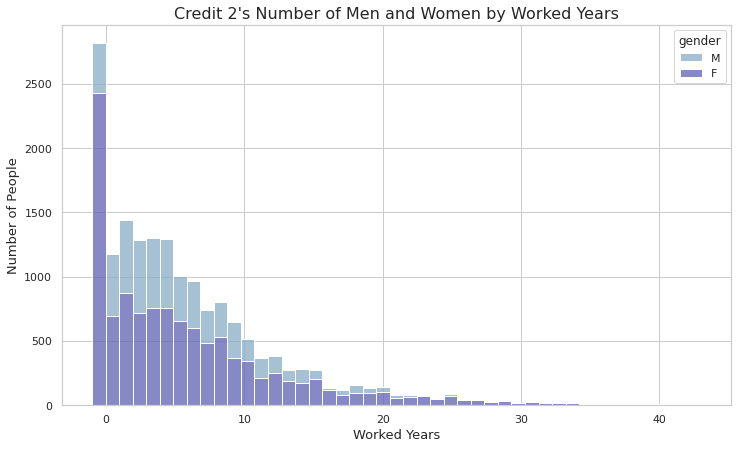

# 성별에 따른 신용등급 1의 인원수

plt.figure(figsize=(12,7))

genderCreditOne = sns.histplot(x='worked_year', hue='gender', multiple='stack', bins=45, data=creditOne)

genderCreditOne.set_xlabel('Worked Years', fontsize=13)

genderCreditOne.set_ylabel('Number of People', fontsize=13)

genderCreditOne.set_title("Credit 1's Number of Men and Women by Worked Years", fontsize=16)

plt.show()

- 신용 등급 1에 대해서도 근무를 하지 않는 여성들이 가장많은 비중을 차지하고 있다.

# 성별에 따른 신용등급 2의 인원수

plt.figure(figsize=(12,7))

genderCreditTwo = sns.histplot(x='worked_year', hue='gender', multiple='stack', bins=45, data=creditTwo)

genderCreditTwo.set_xlabel('Worked Years', fontsize=13)

genderCreditTwo.set_ylabel('Number of People', fontsize=13)

genderCreditTwo.set_title("Credit 2's Number of Men and Women by Worked Years", fontsize=16)

plt.show()

- 신용 등급 2에서는 대부분이 남자가 차지하고 있고 근무연수가 늘어날 수록 비중이 줄어드는 현상이 보인다.

6.4 직업 유형(occpy_type)에 따른 신용등급

- 현재 occyp_type에는 8,171개(31%정도)의 결측치가 존재한다.

- 일한 경력이 없을 경우 직업이 빈칸일 것으로 추측된다.

- 연금 수령자들 또한 직업이 빈칸일 것으로 추측된다.

- 결측치의 비중이 크고 변수에 level이 높아서 drop하는 것이 좋을 수도 있다.

train[train['worked_year']==-1].info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 4438 entries, 14 to 26443

Data columns (total 22 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 gender 4438 non-null object

1 car 4438 non-null object

2 reality 4438 non-null object

3 child_num 4438 non-null int64

4 income_total 4438 non-null float64

5 income_type 4438 non-null object

6 edu_type 4438 non-null object

7 family_type 4438 non-null object

8 house_type 4438 non-null object

9 DAYS_BIRTH 4438 non-null int64

10 DAYS_EMPLOYED 4438 non-null int64

11 occyp_type 0 non-null object

12 family_size 4438 non-null float64

13 begin_month 4438 non-null float64

14 credit 4438 non-null float64

15 income_quartile 4438 non-null float64

16 income_quintile 4438 non-null float64

17 income_decile 4438 non-null float64

18 age 4438 non-null int64

19 age_group 4438 non-null object

20 used_years 4438 non-null int64

21 worked_year 4438 non-null int64

dtypes: float64(7), int64(6), object(9)

memory usage: 797.5+ KB- 일한 경력이 없는 4438명의 경우 occyp_type이 Null값으로 되어 있다.

train[train['income_type']=='Pensioner'].info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 4449 entries, 14 to 26443

Data columns (total 22 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 gender 4449 non-null object

1 car 4449 non-null object

2 reality 4449 non-null object

3 child_num 4449 non-null int64

4 income_total 4449 non-null float64

5 income_type 4449 non-null object

6 edu_type 4449 non-null object

7 family_type 4449 non-null object

8 house_type 4449 non-null object

9 DAYS_BIRTH 4449 non-null int64

10 DAYS_EMPLOYED 4449 non-null int64

11 occyp_type 9 non-null object

12 family_size 4449 non-null float64

13 begin_month 4449 non-null float64

14 credit 4449 non-null float64

15 income_quartile 4449 non-null float64

16 income_quintile 4449 non-null float64

17 income_decile 4449 non-null float64

18 age 4449 non-null int64

19 age_group 4449 non-null object

20 used_years 4449 non-null int64

21 worked_year 4449 non-null int64

dtypes: float64(7), int64(6), object(9)

memory usage: 799.4+ KB- 9명을 제외한 나머지 4,440명의 경우 직업이 Null값이다.

train[(train['worked_year']==-1)&(train['income_type']=='Pensioner')].info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 4438 entries, 14 to 26443

Data columns (total 22 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 gender 4438 non-null object

1 car 4438 non-null object

2 reality 4438 non-null object

3 child_num 4438 non-null int64

4 income_total 4438 non-null float64

5 income_type 4438 non-null object

6 edu_type 4438 non-null object

7 family_type 4438 non-null object

8 house_type 4438 non-null object

9 DAYS_BIRTH 4438 non-null int64

10 DAYS_EMPLOYED 4438 non-null int64

11 occyp_type 0 non-null object

12 family_size 4438 non-null float64

13 begin_month 4438 non-null float64

14 credit 4438 non-null float64

15 income_quartile 4438 non-null float64

16 income_quintile 4438 non-null float64

17 income_decile 4438 non-null float64

18 age 4438 non-null int64

19 age_group 4438 non-null object

20 used_years 4438 non-null int64

21 worked_year 4438 non-null int64

dtypes: float64(7), int64(6), object(9)

memory usage: 797.5+ KB결측치 처리

- 근무 경험이 없고 연금 수령자인 사람들에 대해서 Unempolyed라는 level로 지정해주자.

- 나머지 값들에 대해선 iterative imputation으로 결측치 처리를 진행하자.

# 무직자와 연금수령자 중 무직자에 대해 Unempolyed 지정

train['occyp_type'][(train.worked_year==-1)&(train.income_type=='Pensioner')] = 'Unempolyed'

train['occyp_type'][train.worked_year==-1] = 'Unempolyed'train.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 26457 entries, 0 to 26456

Data columns (total 22 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 gender 26457 non-null object

1 car 26457 non-null object

2 reality 26457 non-null object

3 child_num 26457 non-null int64

4 income_total 26457 non-null float64

5 income_type 26457 non-null object

6 edu_type 26457 non-null object

7 family_type 26457 non-null object

8 house_type 26457 non-null object

9 DAYS_BIRTH 26457 non-null int64

10 DAYS_EMPLOYED 26457 non-null int64

11 occyp_type 22724 non-null object

12 family_size 26457 non-null float64

13 begin_month 26457 non-null float64

14 credit 26457 non-null float64

15 income_quartile 26457 non-null float64

16 income_quintile 26457 non-null float64

17 income_decile 26457 non-null float64

18 age 26457 non-null int64

19 age_group 26457 non-null object

20 used_years 26457 non-null int64

21 worked_year 26457 non-null int64

dtypes: float64(7), int64(6), object(9)

memory usage: 4.4+ MB- 우선 나머지 3733개의 값에 대해선 drop하고 값을 보자

train.dropna(axis=0, inplace=True)

train.info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 22724 entries, 1 to 26456

Data columns (total 22 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 gender 22724 non-null object

1 car 22724 non-null object

2 reality 22724 non-null object

3 child_num 22724 non-null int64

4 income_total 22724 non-null float64

5 income_type 22724 non-null object

6 edu_type 22724 non-null object

7 family_type 22724 non-null object

8 house_type 22724 non-null object

9 DAYS_BIRTH 22724 non-null int64

10 DAYS_EMPLOYED 22724 non-null int64

11 occyp_type 22724 non-null object

12 family_size 22724 non-null float64

13 begin_month 22724 non-null float64

14 credit 22724 non-null float64

15 income_quartile 22724 non-null float64

16 income_quintile 22724 non-null float64

17 income_decile 22724 non-null float64

18 age 22724 non-null int64

19 age_group 22724 non-null object

20 used_years 22724 non-null int64

21 worked_year 22724 non-null int64

dtypes: float64(7), int64(6), object(9)

memory usage: 4.0+ MB# credit값을 object로 치환

train['credit'] = train['credit'].astype('object')

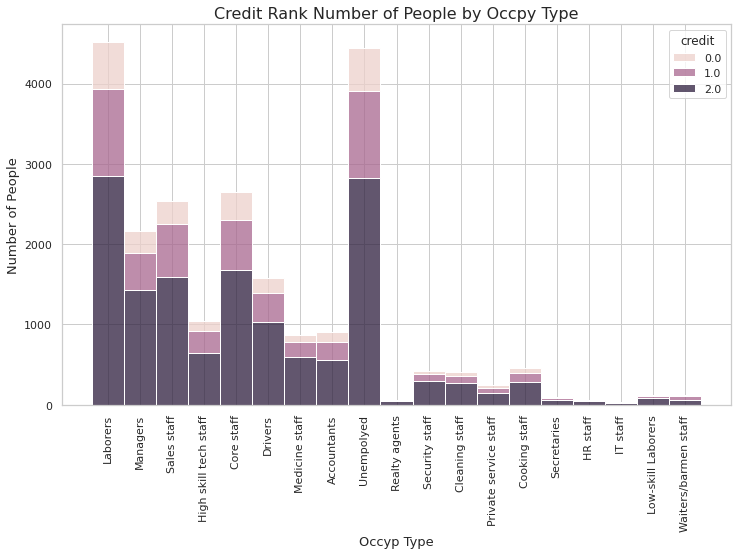

# occyp_type에 따른 신용등급

plt.figure(figsize=(12,7))

occypPlot = sns.histplot(x='occyp_type', hue='credit', multiple='stack', bins=19, data=train)

plt.xticks(rotation = 90)

occypPlot.set_xlabel('Occyp Type', fontsize=13)

occypPlot.set_ylabel('Number of People', fontsize=13)

occypPlot.set_title("Credit Rank Number of People by Occpy Type", fontsize=16)

plt.show()

- 현재 직업군에선 'Laboers', 'Managers', 'Sales staff', 'High skill tech staff', 'Core staff', 'Drivers', 'Medicine staff', 'Accountants', 'Unempolyed'가 해석에 있어 의미있는 직업군으로 보인다.

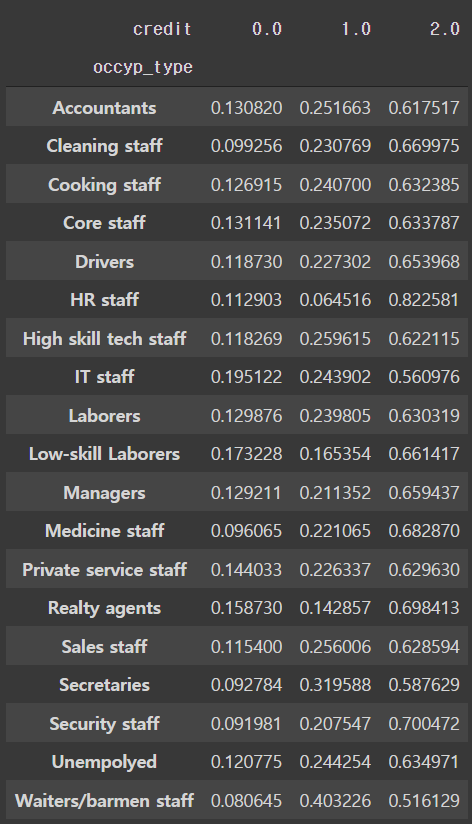

pd.crosstab(train['occyp_type'], train['credit'], normalize='index')

- 현재 체이블에서 보여지는 값으론 사이즈는 작지만 'IT staff'와 'Low-skill Laborers'가 높은 신용등급 0에서의 비율이 가장 높다.