Introduction

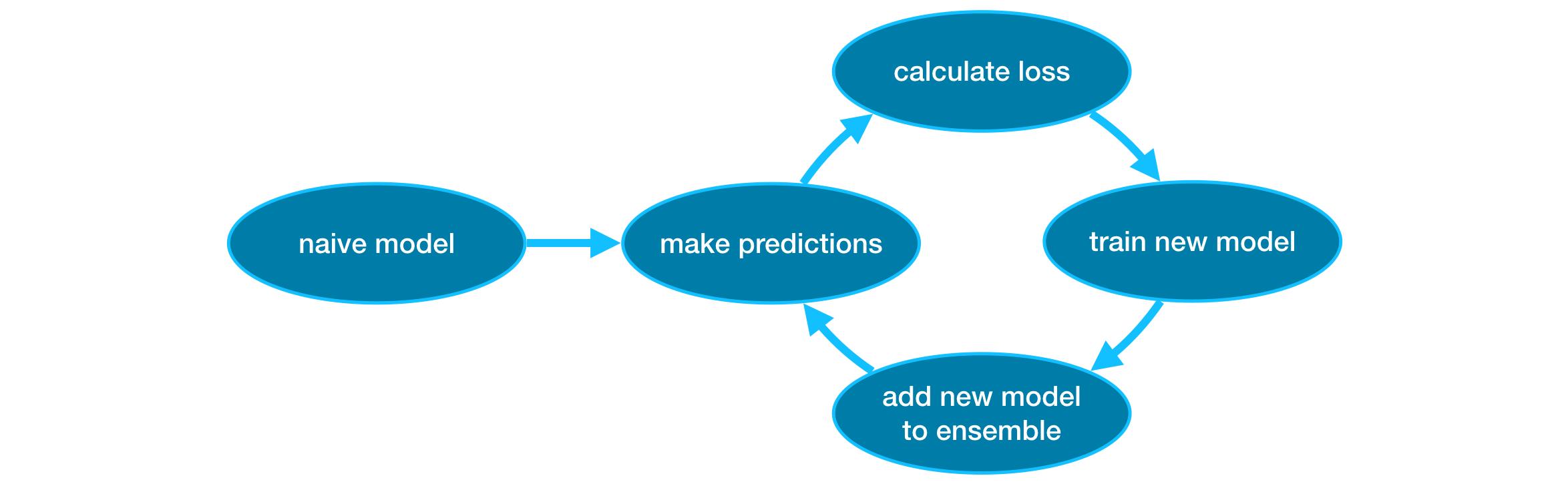

For much of this course, you have made predictions with the random forest method, which achieves better performance than a single decision tree simply by averaging the predictions of many decision trees.

We refer to the random forest method as an "ensemble method". By definition, ensemble methods combine the predictions of several models (e.g., several trees, in the case of random forests).

Next, we'll learn about another ensemble method called gradient boosting.

Example

We begin by loading the training and validation data in X_train, X_valid, y_train, and y_valid.

from xgboost import XGBRegressor

my_model = XGBRegressor()

my_model.fit(X_train, y_train)from sklearn.metrics import mean_absolute_error

predictions = my_model.predict(X_valid)

print("Mean Absolute Error: " + str(mean_absolute_error(predictions, y_valid)))Mean Absolute Error: 238794.73582819404

Parameter Tuning

XGBoost has a few parameters that can dramatically affect accuracy and training speed. The first parameters you should understand are:

my_model = XGBRegressor(n_estimators=500)

my_model.fit(X_train, y_train)my_model = XGBRegressor(n_estimators=500)

my_model.fit(X_train, y_train,

early_stopping_rounds=5,

eval_set=[(X_valid, y_valid)],

verbose=False)my_model = XGBRegressor(n_estimators=1000, learning_rate=0.05)

my_model.fit(X_train, y_train,

early_stopping_rounds=5,

eval_set=[(X_valid, y_valid)],

verbose=False)my_model = XGBRegressor(n_estimators=1000, learning_rate=0.05, n_jobs=4)

my_model.fit(X_train, y_train,

early_stopping_rounds=5,

eval_set=[(X_valid, y_valid)],

verbose=False)

DataEngineer Lee.