Multiple Hypothesis Testing

- This session focuses on

multiple hypothesis testing - A single null hypothesis might look like

: the expected blood pressures of mice in the control and treatment groups are the same

- We will now consider testing null hypotheses,

where e.g.: the expected values of the biomarker among mice in the control and treatment groups are equal

- In this setting, we need to be careful to avoid incorrectly rejecting too many null hypotheses,

i.e. having too many false positives

A Quick Review of Hypothesis Testing

- Hypothesis tests allow us to answer simple

yes-or-noquestions, such as- Is the true coefficient in a linear regression equal to zero?

- Does the expected blood pressure among mice in the treatment group equal the expected blood pressure among mice in the control group?

- Hypothesis testing proceeds as follows :

- Define the null and alternative hypotheses

- Construct the test statistic

- Compute the -value

- Decide whether to reject the null hypothesis

1. Define the Null and Alternative Hypotheses

- We divide the world into

nullandalternativehypotheses - The

null hypothesis, is the default state of belief about the world. For instance :- The true coefficient equals

zero - There is no difference in the expected blood pressure

- The true coefficient equals

- The

alternative hypothesis, represents something different and unexpected. For instnace :- The true coefficient is

non-zero - There is a difference in the expected blood pressure

- The true coefficient is

2. Construct the Test Statistic

- The test statistis summarizes the extent to which our data are consistent with

- Let respectively denote the average blood pressure for the mice in the treatment and control groups

- To test : , we use a two-sample -statistic

3. Compute the p-value

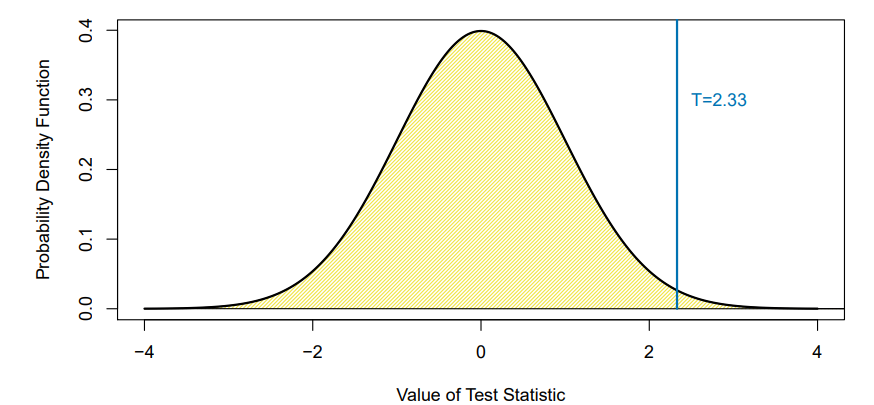

- The -value is the probability of observing a test statistic at least as extreme as the observed statistic,

under the assumption thatis true - A small -value provides evidence

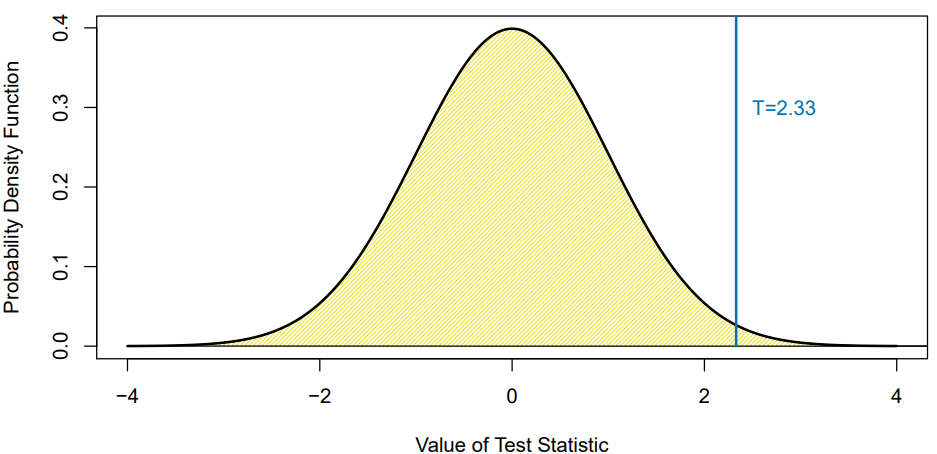

against - Suppose we compute for our test of

- Under for a two-sample -statistic

- The p-value is because, if is true, we would only see this large of the time

4. Decide Whether to Reject Null Hypothesis, Part 1

- A small -value indicates that such a large value of the test statistic is unlikely to occur under

- So, a small -value provides evidence against

- If the -value is sufficiently small, then we will want to

reject - But how small is small enough? To answer this, we need to understand the

Type 1 Error

4. Decide Whether to Reject Null Hypothesis, Part 2

- The

Type 1 Error rateis the probability of making aType 1 Error - We want to ensure a small

Type 1 Error rate - If we reject when the p-value is less then , then the

Type 1 Error ratewill be at most - So, we reject when the p-value falls below some : often we choose to equal or

Multiple Testing

- Now suppose that we wish to test

null hypotheses, - Can we simply reject all

null hypothesesfor which the corresponding -value falls below - If we reject all null hypotheses for which the -value falls below , then how many

Type 1 Errorwill be make?

A Thought Experiment

- Suppose that we flip a fair coin ten times, and we wish to test

- We'll probably get approximately the same number of heads and tails

- The -value probably won't be small. We do not reject

- But what if we flip fair coins ten times each?

- We'd except one coin (on average) to come up all tails

- The -values for the

null hypothesisthat this particular coin is fair is less than ! - So we would conclude it is not fair, i.e. we

reject null hypothesis, even though it's a fair coin

- If we test a lot of hypotheses, we are almost certain to get one very small -value by chance

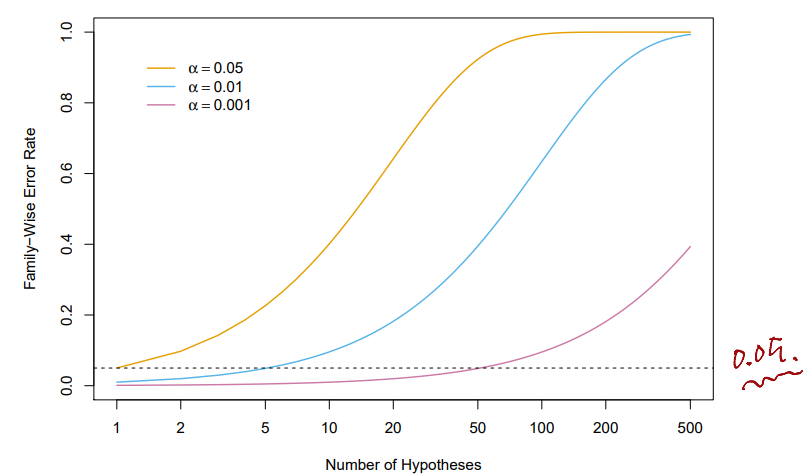

The Challenge of Multiple Testing

- Suppose we test , all of which are true, and reject any

null hypothesiswith a -value below - Then we except to falsely reject approximately

null hypotheses - If , then we expect to falsely reject

null hypothesesby chance!That's a lot of Type 1 Errors, i.e. false positives

The Family-Wise Error Rate

- The

family-wise error rate(FWER) is the probability of makingat least oneType 1 error when conducting hypothesis tests

Challenges in Controlloing the FWER

- If the tests are

independentand all are true then

The Bonferroni Correction

- Where is the event that we

falsely rejectthe thnull hypothesis - If we only reject hypotheses when the -value is less than , then

- This is the

Bonferroni Correction: to controlFWERat level , reject anynull hypothesiswith -value below

Holm's Method for Controlling the FWER

- Compute -values, for the

null hypotheses - Order the -values so that

- Define

- Reject all

null hypotesesfor which- Holm's method controls the

FWERat level

- Holm's method controls the

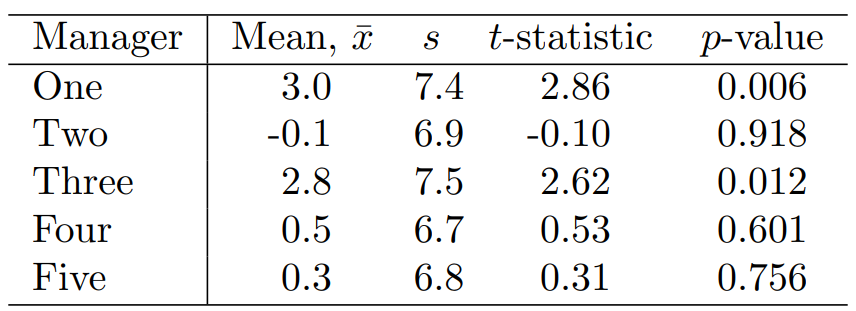

Holm's Method on the Fund Manager Data

- The ordered -values are

- The

Holm procedurerejects the first twonull hypotheses, because Holmrejects for thefirstandthirdmanagers, butBonferronionly rejects for thefirstmanager

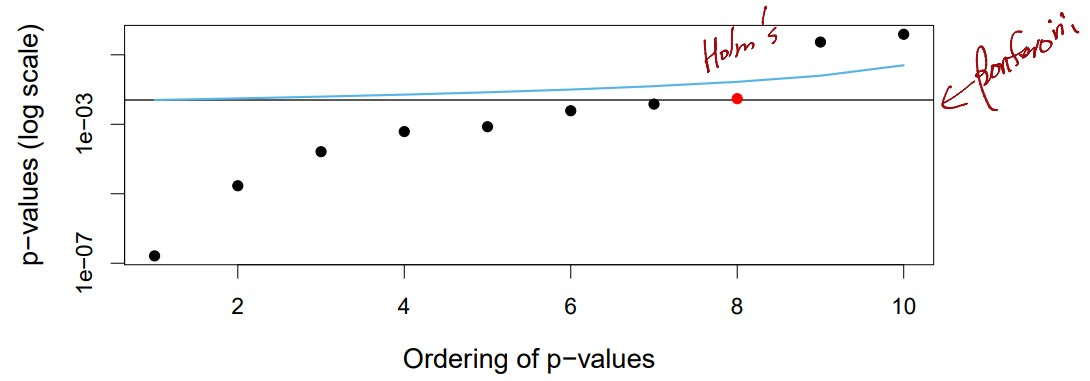

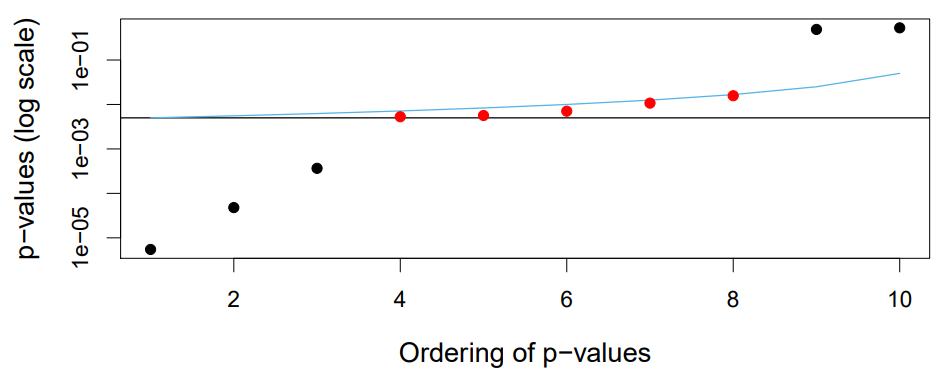

Comparison with m=10 p-values

- Aim to control

FWERat - -values below the balck horizontal line are rejected by

Bonferroni - -values below the blue line are rejected by

Holm HolmandBonferronimake the same conclusion on the black points, but onlyHolmrejects for the red point

A More Extreme Example

- Now five hypotheses are rejected by

Holmbut not byBonferroni... - even though both control

FWERat

Holm or Bonferroni?

Bonferroniis simple : reject anynull hypothesiswith a -value belowHolmis slightly more complicated, but it will lead to more rejections while controllingFWERSo,

Holmis a better choice

The False Discovery Rate

- Back to this table :

- The

FWERrate focuses on controlling , i.e., the probability of falsely rejectinganynull hypothesis - This is a tough ask when is large. It will cause us to be super conservative(i.e. to very rarely reject)

- Instead, we can control the

false discovery rate

Intuition Behind the False Discovery Rate

- A scientist conducts a hypothesis test on each of drug candidates

- She wants to identify a smaller set of promising candidates to investigate further

- She wants reassurance that this smaller set is really

promising, i.e. not too many falsely rejected 's FWERcontrolsFDRcontrols the fraction of candidates in the smaller set that are really false rejections.

Benjamini-Hochberg Procedure to Control FDR

- Specify , the level at which to control the

FDR - Compute -values for the

null hypotheses - Order the -values so that

- Define

- Reject all null hypotheses for which

Then,FDR

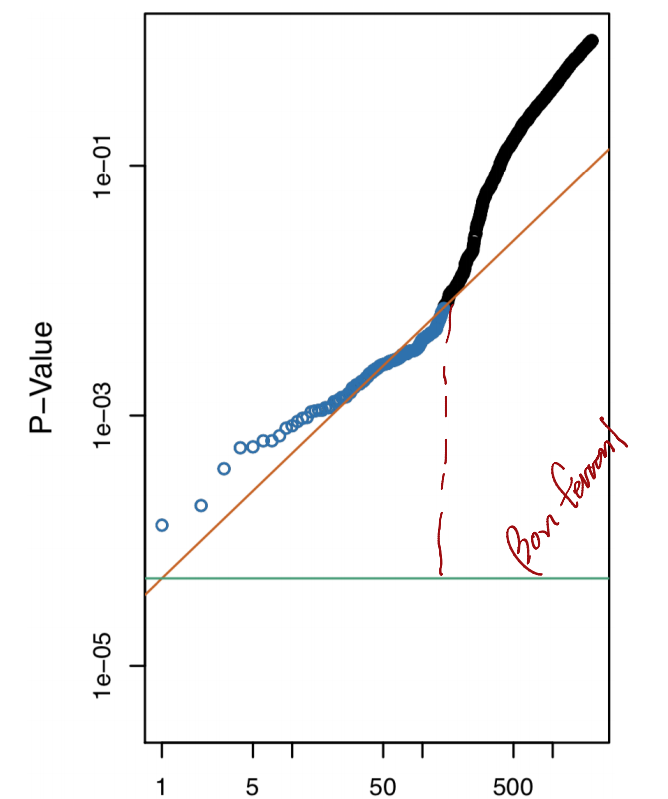

A Comparison of FDR vs FWER

- Here, -values for

null hypothesesare displayed - To control

FWERat level withBonferroni: reject hypotheses below green line - To control

FDRat level withBenjamini-Hochberg: reject hypothese shown in blue

- Consider p-values from the Fund data :

- To control

FDRat level usingBenjamini-Hochberg:- Notice that

- So, we reject and

- To control

FWERat level usingBonferroni:- We reject any

null hypothesisfor which the -value is less than - So, we reject only

- We reject any

Re-Sampling Approaches

- So far, we have assumed that we want to test some

null hypothesiswith some test statistic , and that we know the distribution of under - This allows us to compute the -value

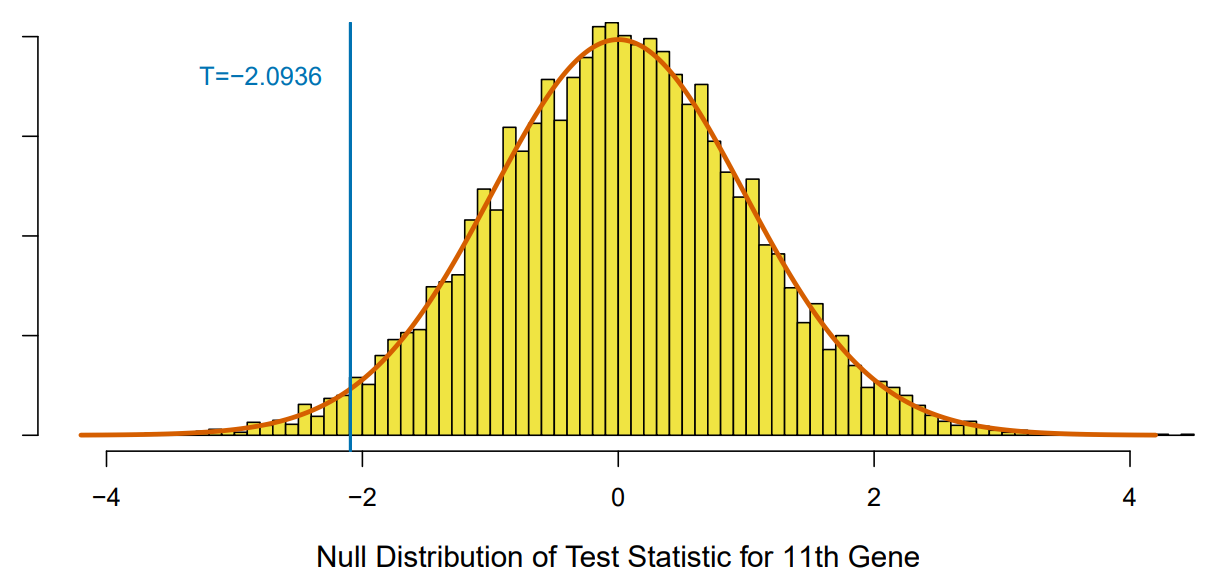

- What if this theoretical null distribution is unknown?

A Re-Sampling Approach for a Two-Sample t-Test

- Suppose we want to test versus , using independent observations from and independent observations from

- The two-sample -statistic takes the form

- If and are large, then approximately follows a distribution under

- If and are small, then we don't know the theorectical null distribution of

- Let's take a

permutationorre-samplingapproach...

- Compute the two-sample -statistic on the original data and

- For (where is a large number, like ) :

2.1.Randomly shufflethe observations

2.2. Call the first shuffled observations and call the remaining observations

2.3. Compute a two-sample -statistic on the shuffled data, and call it - The -value is given by

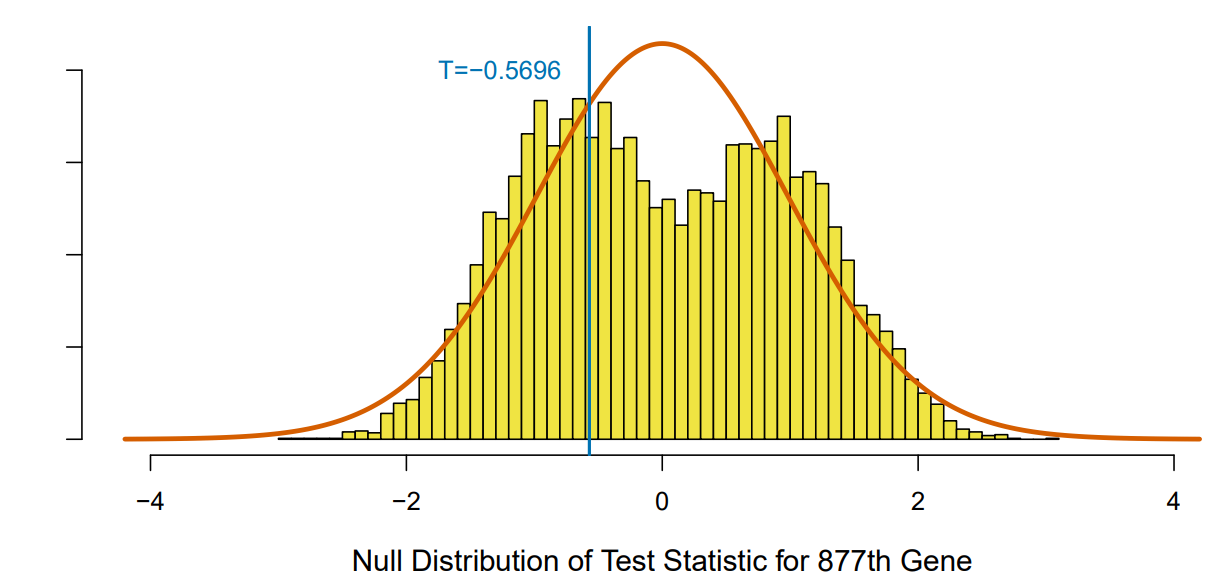

- Theoretical -value is . Re-sampling -value is

- Theoretical -value is . Re-sampling -value is

More on Re-Sampling Approaches

Re-samplingapproaches are useful if the theoreticalnull distributionis unavailable, or requires stringent assumptions- An extension of the re-sampling approach to compute a -value can be used to control

FDR - This example involved a two-sample -test, but similar approaches can be developed for other test statistics

AI, Security