Classification

Qualitativevariables take values in anunordered set, such as- Given a

featurevector and aqualitativeresponse taking values in the setThe

Classificationtask is to build a function that takes as input thefeaturevector and predicts its value for - Often we are more interested in estimating the

probabilitiesthat belongs to each category in .

Can we use Linear Regression?

-

Suppose for the

Defaultclassification task that we code -

Can we simply perform a

linear regressionof on and classify asYesif ?- In this case of a

binary outcome,linear regressiondoes a good job as aclassifier, and if equivalent tolinear discriminant analysiswhich we discuss later - Since in the population , we might think that

regressionis perfect for this task - However,

linear regressionmight produce probabilitiesless than zeroorbigger than oneLogistic regressionis more appropriate

- In this case of a

-

Now suppose that

-

Linear regressionis not appropriate hereMulticlass Logistic RegressionorDiscriminant Analysisare more appropriate

Logistic Regression

- Let's write for short and consider using to predict .

Logistic regressionuses the form - is a mathematical constant [Euler's number]

- will have values between 0 and 1

- A bit of rearrangement gives :

log oddsorlogit

Maximum Likelihood

- This

likelihoodgives the probability of the observed zeros and ones in the data - We pick and to

maximizethelikelihoodof the observed data

Making Predictions

- What is estimated probability of for someone with a of $1000?

Logistic Regression with several variables

Logistic Regression with more than two classes

Multiclass logistic regressionis also referred to asmultinomial regression

Discriminant Analysis

- Here the approach is to model the distribution of in each of the classes separately, and then use

Bayes theoremto flip things around and obtain - When we use

NormalorGaussiandistributions for each class, this leads tolinearorquadratic discriminant analysis

Bayes theorem for classification

-

Bayes theorem -

One writes this slightly differently for

discriminant analysis:- is the

densityfor in class - is the

marginalorpriorprobability for class

- is the

-

When the

priorsare different, we take them into account as well, and compare . -

On the right, we favor the blue class - the decision boundary has shifted to the left

Why discriminant analysis?

- When the classes are

well-separated, the parameter estimates for thelogistic regression modelare surprisinglyunstable. But,Linear discriminant analysisdoes not suffer from this problem - If is small and the distribution of the predictors is approximately

normalin each of the classes, thelinear discriminant modelis again morestablethan thelogistic regression model Linear discriminant analysisis popular when we have more than two response classes, because it also provideslow-dimensionalviews of the data

Linear Discriminant Analysis when p = 1(Uncorrelated)

- The

Gaussian densityhas the form - Here is the

mean, and thevariance(in class ) - We will assume that all the are the same

- Plugging this into

Bayes formula, we got a rather complex expression for

Discriminant functions

- To classify at the value , we need to see which of the is largest

- Taking logs, and discarding terms that do not depend on , we see that this is equivalent to assigning to the class with the largest

discriminant score: - Note that is a

linearfunction of - If there are classes and , then one can see that the

decision boundaryis at - where is the usual formula for the estimated

variancein the th class

Linear Discriminant Anaysis when p > 1(Correlated)

- (Red :

linearin , other :constant) - Despite its complex form:

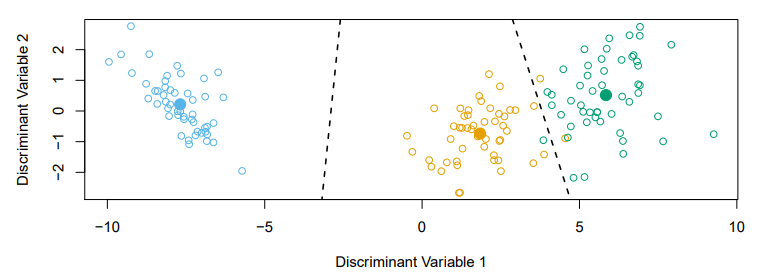

Fisher's Discriminant Plot

- When there are classes,

linear discriminant analysiscan be viewed exactly in a dimensional plotBecause it essentially classifies to the

closest centroidand they span aK-1dimensional plane - Even when , we can find the

best2-dimensional plance for visualizing the discriminant rule

From delta function to probabilities

- One we have estimates , we can turn these into estimates for class probabilities:

- So classifying to the largest amounts to classifying to the class for which is

largest - When , we classify to class if , else to class 1

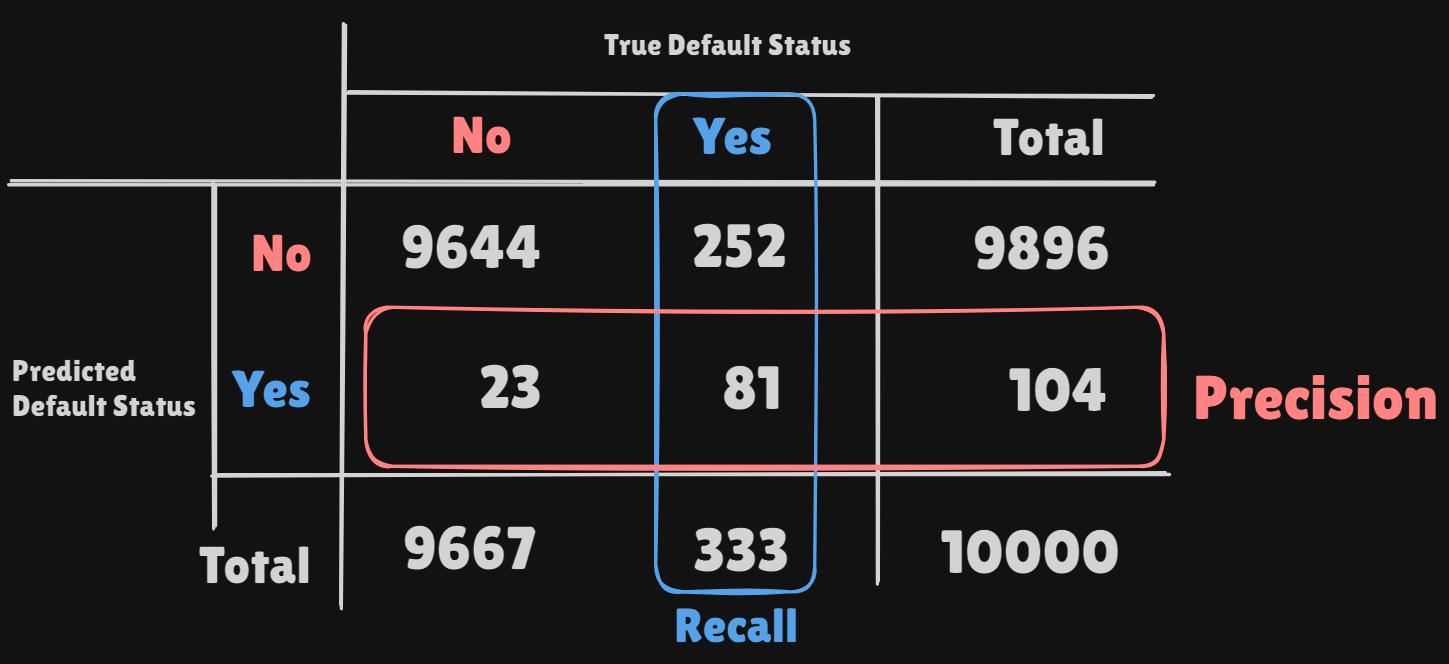

Confusion Matrix

misclassification rate:precision:recall:False positive rate: The fraction ofnegativeexamples that are classified aspositive- in exampleFalse negative rate: The fraction ofpositiveexamples that are classified asnegative- in example- We produced this table by classifying to class if

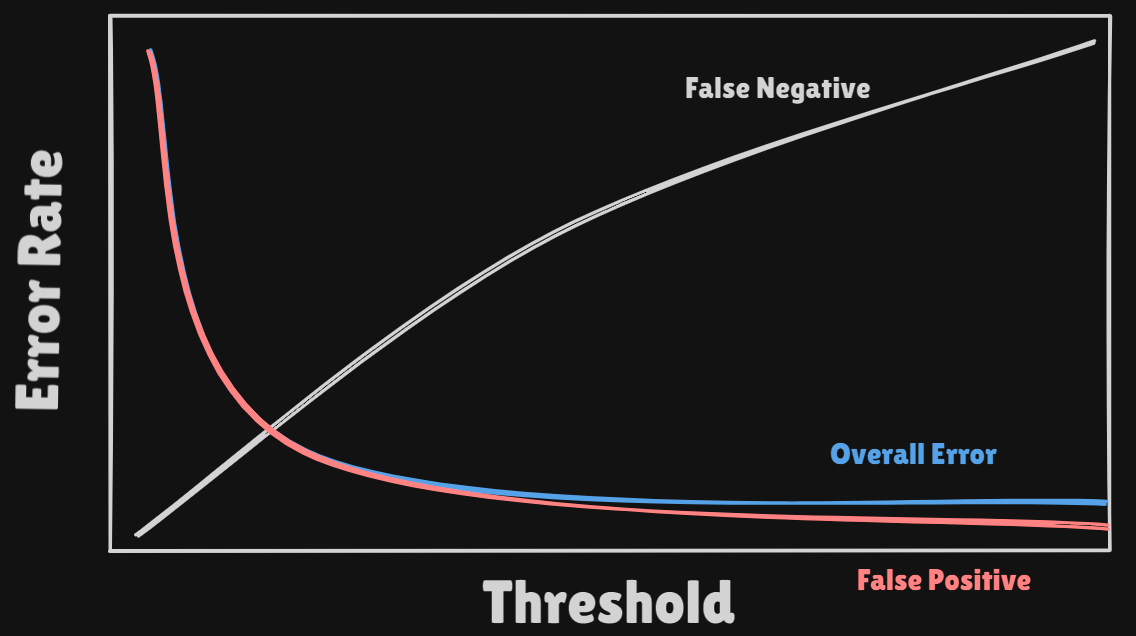

- Lower Threshold : Higher

False Positiveand LowerFalse Negative - Higher Threshold : Lower

False Positiveand HigherFalse Negative

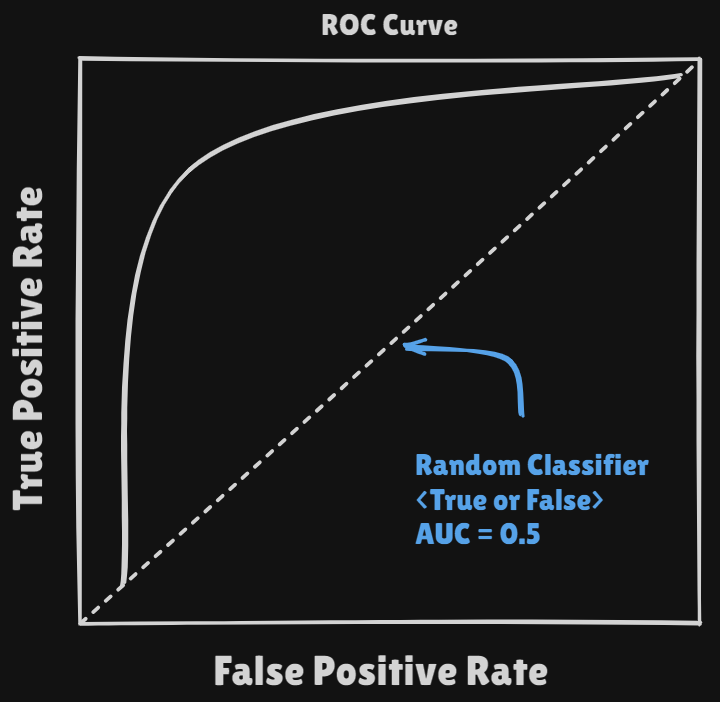

With controlling thethresholdwe can getROC Curve - If the

classifierhas good performance theAUCvalue goes near 1

- Lower Threshold : Higher

Other forms of Discriminant Analysis

- With

Gaussiansbut different in each class, we getquadratic discriminant analysis - With

Gaussiansand same in each class, we getlinear discriminant analysis - With (conditional independence model) in each class we get

naive Bayes. ForGaussianthis means the arediagonal- : Covariance Matrix

- : Covariance Matrix

Naive Bayes

- Assume features are

independentin each class - Useful when is large, and so multivariate methods like

QDAand evenLDAbreak down Gaussian naive Bayesassumes each is diagonal:- For

mixedfeature vectors(qualitative and quantitative)If is

qualitative, replace with probability mass function (histogram) over discrete categories

Logistic Regression versus LDA

- For a two-class problem, one can show that for

LDA - So it has same form as

logistic regression - The difference is in how the parameters are estimated

Logistic Regressionuses theconditional likelihoodbased on (discriminative learning)LDAuses thefull likelihoodbased on (generative learning)

Logistic Regressioncan also fitquadratic boundarieslikeQDA, by explicitly includingquadratic termsin the model

Multinomial Logistic Regression

- The simplest representation uses different linear functions for each class, combined with the

softmaxfunction to form probabilities - There is a rebundancy here; we really only need functions

- We fit by maximizing the

multinomial log likelihood(cross-entropy) - a generalization of the binomial

Generative Models and Naive Bayes

-

Logistic regressionmodels directly, via the logistic function -

Similarly the

multinomial logistic regressionuses thesoftmax function -

These all model the

conditional distributionof given -

By contrast

generative modelsstart with theconditional distributionof given , and then useBayes formulato turn things around: -

is the density of given

-

is the

marginal probabilitythat is in class -

LinearandQuadraticdiscriminant analysis derive fromgenerative models, where areGaussian -

Often useful if some classes are

well seperated- a situation wherelogistic regressionisunstable -

Naive Bayesassumes that the densities in each classFactor

-

Equivalently this assumes that the features are

independentwithin each class -

Then using

Bayes formula: -

: Probability that the value could be found by each distribution

Why independence assumption for naive bayes?

- Difficult to specify and model

high-dimensional densities. Much easier to specifyone-dimensional densities - Can handle

mixedfeatures- If feature is

quantitative, can model asunivariate Gaussian. We estimate and from the data, and then plug intoGaussian density formulafor - Alternatively, can use a

histogramestimate of the density, and directly estimate by the proportion of observations in the bin into which falls - If feature is

qualitative, can simply model the proportion in each category

- If feature is

Naive Bayes and GAMs

- Hence, the

Naive Bayesmodel takes the form of ageneralized additive modelfrom later Chapter

Generalized Linear Models

Generalized linear modelsprovide a unified framework for dealing with many different response types(non-negative responses, skewed distributions, and more)

- In left plot we see that the

variancemostly increases with themean - Taking log() alleviates this, but has its own problems: e.g.

predictionsare on the wrong scale, and some counts are zero

Poisson Regression Model

Poisson Distributionis useful for modeling counts:- - there is a mean/variance dependence

- With covariates, we modelor equivalently

- Model automatically gurantees that the

predictionsarenon-negative

Three GLMs

- We have covered three

GLMs:Gaussian,BinomialandPoisson - They each have a characteristic

linkfunction. This it the transformation of themeanthat is represented by alinear modellinear:logistic:Poisson regression:

- They also each have characteristic

variancefunctions - The modls are fit by

maximum-likelihood