R-Squared() Score

Introduction

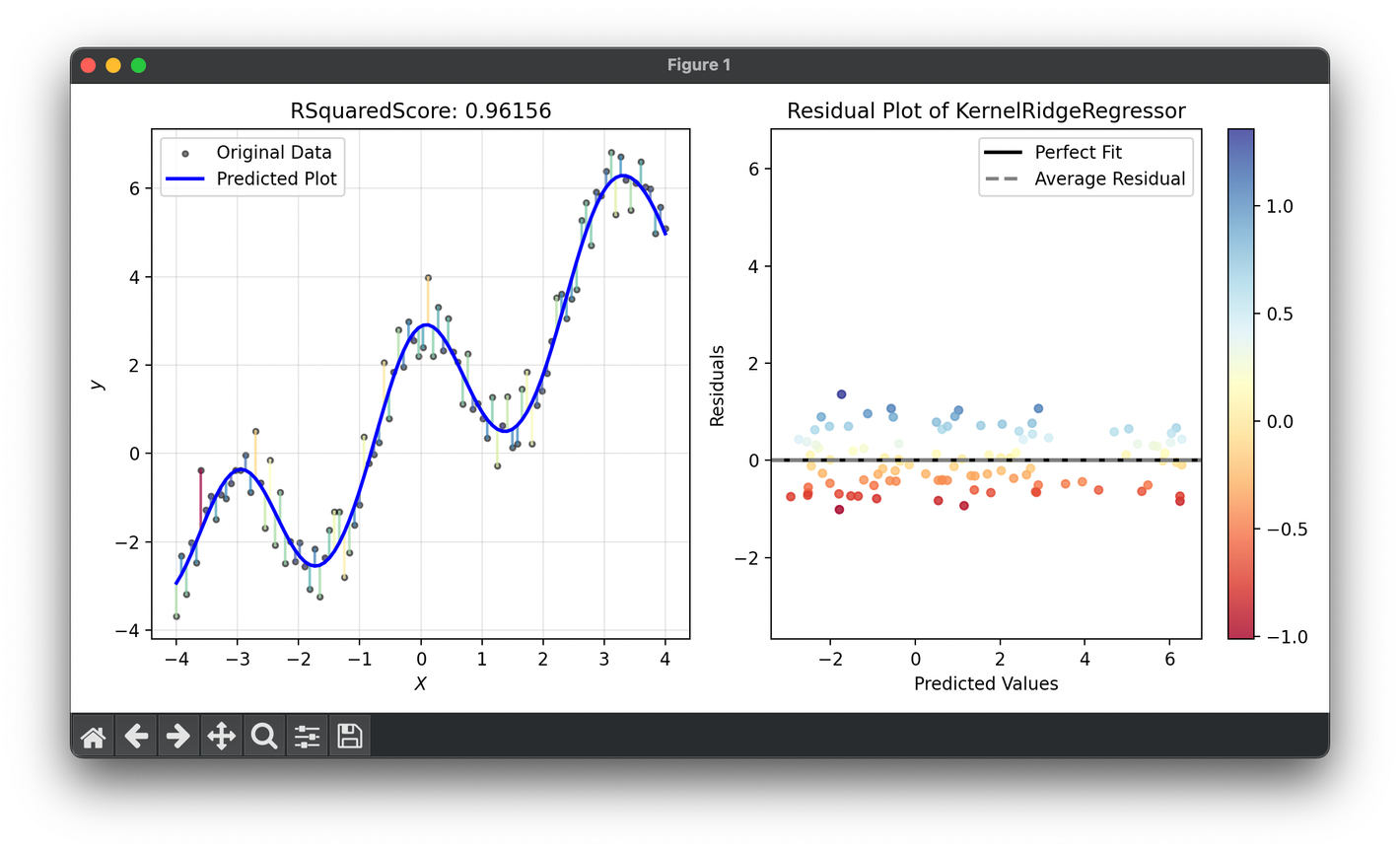

, also known as the coefficient of determination, is a statistical measure used to assess the goodness of fit of a regression model. It quantifies how well the independent variables explain the variability of the dependent variable, offering insights into the percentage of the data's variance accounted for by the model. is widely utilized in predictive analytics and modeling to evaluate the predictive power and accuracy of regression models.

Background and Theory

The value ranges from 0 to 1, where 0 indicates that the model explains none of the variability of the response data around its mean, and 1 indicates that the model explains all the variability. It is calculated based on the proportion of the total variation of outcomes explained by the model. The formula for is given by:

where:

- (sum of squares of residuals): ,

- (total sum of squares): ,

- is the actual value,

- is the predicted value,

- is the mean of actual values, and

- is the number of observations.

Applications

- Predictive Modeling: Assessing the performance of regression models in various fields, such as economics, finance, environmental science, and social sciences.

- Model Comparison: Comparing the explanatory power of different models on the same dataset.

- Feature Selection: Identifying the most relevant predictors by examining the change in when variables are added or removed from the model.

Strengths and Limitations

Strengths

- Interpretability: is a straightforward measure that provides insight into the proportion of the variance explained by the model.

- Comparability: It allows for the comparison of the explanatory power of models on the same dataset.

Limitations

- Non-indicative of Predictive Accuracy: A high does not necessarily mean the model has high predictive accuracy. It only indicates the proportion of variance explained.

- Sensitive to Overfitting: Adding more predictors to a model can artificially inflate , even if those variables do not improve the model’s predictive capability.

- Not Suitable for All Models: is not appropriate for evaluating models where the assumptions of linear regression are violated or for models not based on linear assumptions.

Advanced Topics

- Adjusted : To account for the potential overfitting with the inclusion of multiple predictors, the adjusted modifies the calculation to reflect the number of predictors in the model. It provides a more accurate measure for comparing models with a different number of variables.where is the number of predictors and is the sample size.

- Partial : Evaluates the contribution of one or more predictors to the model while controlling for the presence of other variables.

References

- James, G., Witten, D., Hastie, T., & Tibshirani, R. (2013). An Introduction to Statistical Learning. Springer.

- Draper, N. R., & Smith, H. (1998). Applied Regression Analysis. Wiley.